For anyone looking to start learning how to invest, I would always recommend starting with products or services you use. Being a foodie myself, F&B naturally falls within my circle of competence!

Before we dive into today’s main topic, please allow me to sidetrack a little.

When selecting F&B companies as investment, always choose companies with products that could become part of their customer’s routine. Even better if it’s a little addictive.

Think Starbucks.

Coffee is something that could be consumed daily (or must be consumed daily for some) and customers seldom change their daily routine. Once you find something that suits your taste and the location is convenient, people generally don’t change due to homeostasis.

Slap on a membership program (including its own mobile payment) and premium branding, and its product becomes extremely sticky.

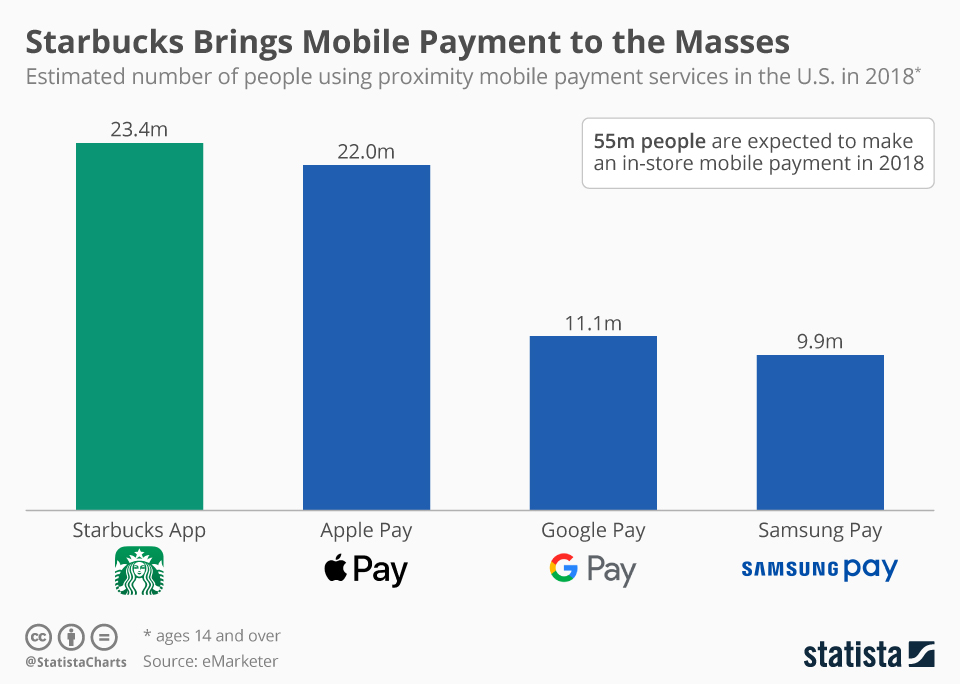

Just take a look at how Starbucks mobile payment towers over mainstream mobile payment.

As Mohnish Pabrai highlighted: Recurring Revenue Stream (RSS) is the most important thing for a business.

It is no wonder Starbucks has done remarkably well for its shareholders.

I would avoid restaurant businesses like the Cheesecake Factory, Applebee, etc. Consumers usually patronize them on special occasions and are less likely to visit the same restaurant to celebrate birthdays, anniversaries repeatedly.

When it is not part of their customers routine to visit these restaurants, they have to battle it out. These restaurants end up spending a large amount on marketing and promotions to bring in different customers every day.

Alright, now that this is out of the way, let’s jump right into the article!

Enter Domino’s

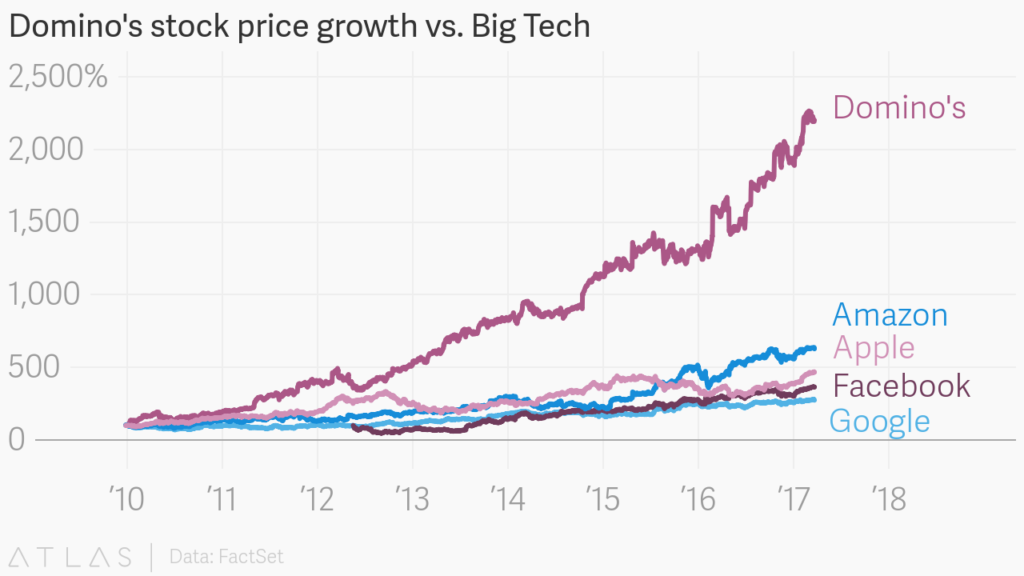

We always hear about tech stocks generating immense wealth for shareholders due to their scalability and capital light business model.

Who knew Domino’s could outperform them?

Three observations from the chart:

- The franchise model is able to scale rapidly.

- The franchise model is capital-light.

AmericansConsumers can eat pizza over and over again.

Domino makes money largely by collecting franchise fees and providing its franchisees with supplies (i.e. dough, etc).

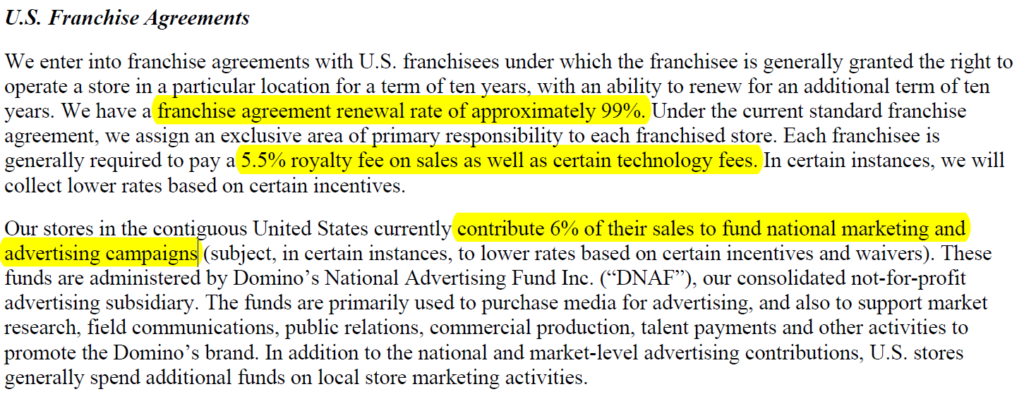

U.S. Franchise Agreements are contracts entered with individual franchisees for 10 years. Domino collects roughly 11.5% of its franchisee’s revenue. This is made up of 5.5% royalty fees and 6% for group marketing expenses.

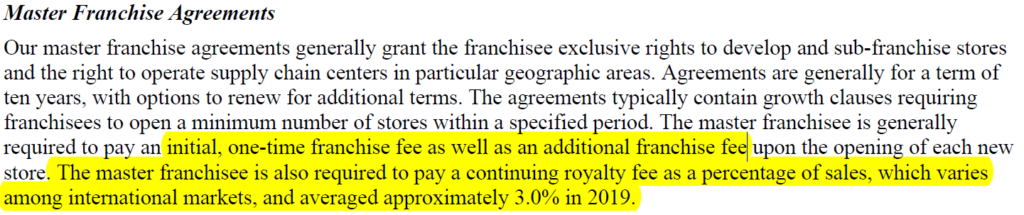

Master Franchise Agreements are bigger contracts that give the franchisee exclusive rights to operate in certain areas. Domino’s collect one-time upfront fees for a long-term agreement (>10 years) and an upfront fee whenever a new store is opened.

On a recurring basis, they collect 3% of revenue as royalty fee.

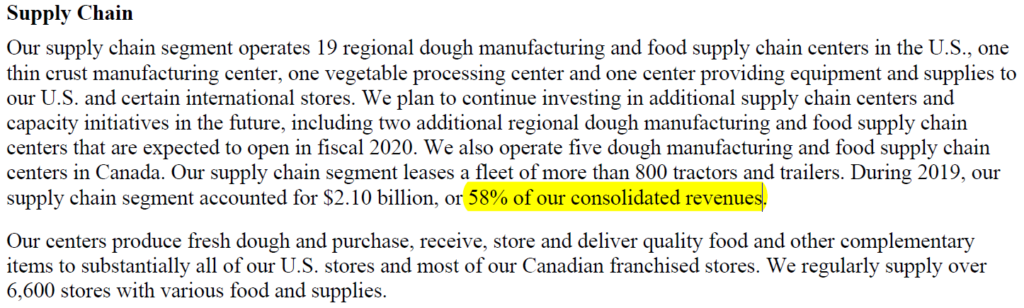

Last but not least, they make money through their supply chain (e.g. selling dough to its franchisees).

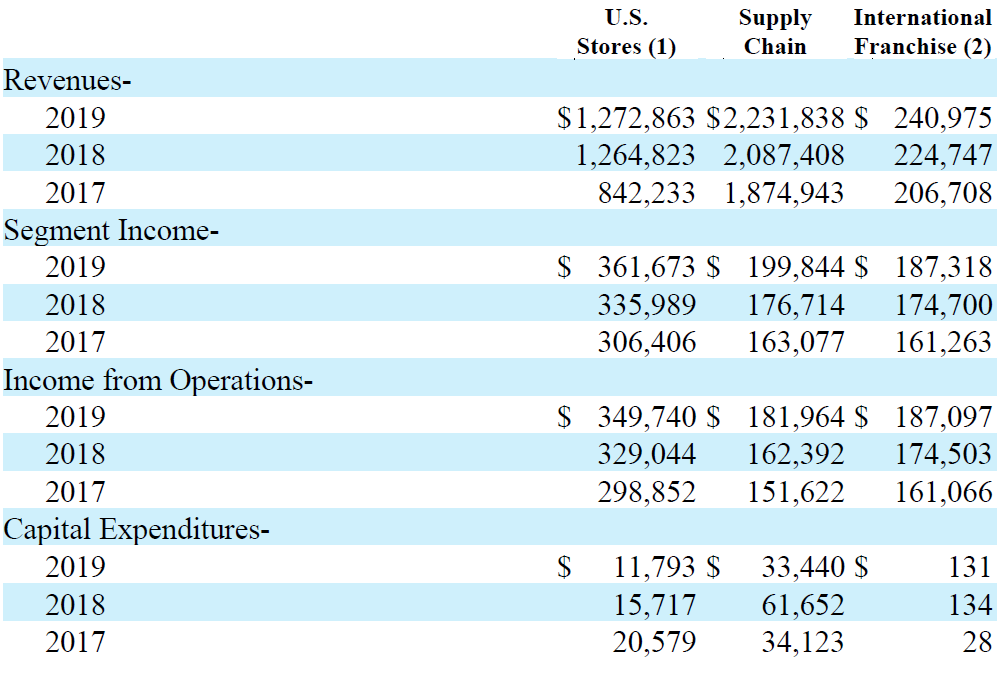

Higher Profitability

Due to the cost of sales (i.e. raw materials), the margins on the supply chain are much smaller when compared to collecting royalties (there’s no COS when collecting franchise fees).

Domino’s does have company-owned stores as well, although they contribute much lesser to the bottom line with a margin of 23.7%.

A margin of 23.7% means Domino’s makes approximately $1.42 from the $5.99 pizza below:

Here we can appreciate the difference in operating margin amongst U.S. stores, Supply Chain, and International Franchise.

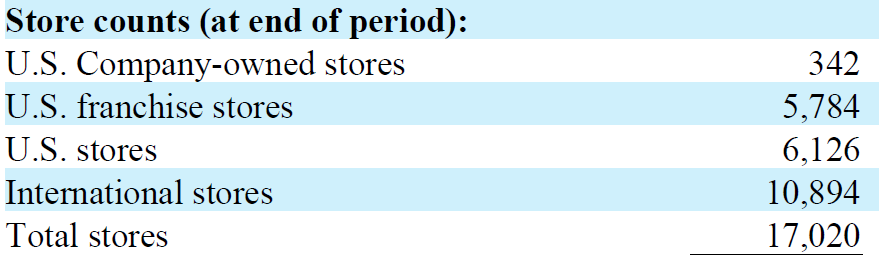

Note that their U.S. Stores is a mixture of franchise agreements.

Specifically, they have 342 company-owned stores and 5,784 franchise stores in the U.S.

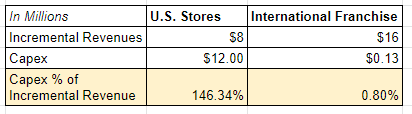

Capital-Light Model

Notice the difference in capital expenditures (capex) between a combined strategy of franchise and company-owned (U.S. Stores) and 100% franchise (International Franchise).

The capex required to generate an additional dollar of sales under the International Franchise (100% franchise) is way lesser than the U.S. Stores (a mixture of company-owned & franchise)!

In fact, the amount of capex required for franchises is almost non-existent.

This shows the power of capital-light businesses!

With the franchise model, Domino’s does not have to come up with the capital required to set up stores, buy new equipment, etc. The franchisees’ will be the ones who come up with that capital!

Compare this with the Chipotle business model where 100% of their stores are company-owned. They need to have capital locked in for working capital needs, buying of equipment, renovation, staff uniforms, and many more—before they could start making money.

Side note: This is not to say company-owned models are inferior. In investing, as with life, it is always wise not to take an extreme stance. I will write about company-owned models in my future articles. Subscribe to be notified!

Conclusion

There’re many benefits to investing in a franchise model—higher margins, low capital intensity, and scalability. We need to appreciate how much capital it frees up for a company, in terms of initial start-up costs and working capital requirements.

‘The three most harmful addictions are heroin, carbohydrates, and a monthly salary. ‘

Nassim Nicholas Taleb

Let’s not forget recurring revenue streams, the revenue from the royalties is extremely sticky and when it comes to pizza, consumers seldom change their preferences.

So much so that Domino’s stock has outperformed the top tech companies. As investors, we can afford to ignore pharma, SaaS, oil & gas sectors if they are not in our circle of competence. Sometimes the next big winner is just something simple, easily understood, and delicious…

| Thank you for taking the time to read my blog. If you’re enjoying the content so far, I’m sure you’ll find 3-Bullet Sunday helpful. As an extension to the regular posts, I send out weekly newsletters sharing timeless ideas on life and finance. I do not share this content elsewhere. Join 400+ subscribers and subscribe to our newsletter today to receive a free investment checklist! |

Join our growing tribe on Twitter.

Great article. Enjoyed it thoroughly. I had a quick question.

How did you arrive at the data (e.g., incremental revenues, capex) in the capital expenditure table?

Thanks Sumeet, all this can be found under the footnotes of the 10-K. They will usually break all the income and expenses into different segments.

Got it. Thanks. Excellent observation. One follow up question. Is there a need to distinguish between maintenance vs. growth capex?

You could, but for most of the companies I invest in they are churning out so much free cash flow there’s no need to do that. E.g. I invested in Facebook during the scandals in late 2018, it was generating so much free cash flow and the company was on fire sale.

Even for companies like Dominos the capex as a % of revenue is so insignificant, it makes no point to segregate between maint and growth capex.

One company that may require distinguishing between maint vs growth capex to spot its hidden potential would be Amazon. The company is continuously reinvesting so heavily into the business in its early years.

I have another article that touch on Amazon and how you could look certain adjustments to see its potential. You can find it here https://steadycompounding.com/investing/amazon-and-the-problem-with-reported-earnings/

Think you might be interested in MTY Food Group (TSE:MTY) basically combining this franchise model with an active M&A roll up.

Thanks Johan! I’ll definitely give it a look. Do share with me your thesis/research at steadycompounding@gmail.com if possible. Happy to discuss.