From the earlier post, we learned that not all growth is value-adding. Today, we are going to discuss an equally important concept – operating leverage. Not all sales growth has the same effect on profitability.

With these two articles, I wish to highlight to readers that sales growth, profit growth, and value creation are distinct. Growth in sales creates value only when a company earns a rate of return greater than its cost of capital. Furthermore, the percentage increase in profits may be vastly different than the increase in sales growth and vice versa as a result of operating leverage.

Operating leverage is a measurement of how an additional dollar of sales translates into operating profit. A 10% increase in sales may result in a 30% increase in net profits. Likewise, a 10% decline in sales may send a company’s share price earnings into oblivion, as we will see in GameStop’s case study later.

How Does Operating Leverage Work?

Operating leverage is the most common in businesses which require a large amount of fixed assets investments. Theme parks are an example of a business with high operating leverage. Approximately 75% of their costs are fixed, with labor being the largest component. This means that if visitor numbers decline (i.e. sales), their operating profit will decline at a much larger magnitude.

Fixed costs are costs that a company must bear regardless of the sales level. For example, Starbucks must continue paying its rent, labor, and utilities regardless of the amount of coffee sold per store.

Variable costs are costs that are linked to the sales level. For Starbucks, this would be their coffee beans, whipped cream, etc. The more Frappuccinos they sell, the higher the amount of cost they would incur for the raw materials (i.e. coffee beans, etc).

The chart below from Credit Suisse illustrates nicely the impact on operating profit margin based on revenue changes and cost structure (fixed vs variable).

The concept of operating leverage is best explained with an example. ABC is a company with a higher operating leverage, 75% fixed expenses and 25% variable expenses. XYZ is a company with a lower operating leverage, 25% fixed expenses and 75% variable expenses.

Both of them are having sales of $10,000,000 and $8,000,000 in expenses, giving them a profit of $2,000,000.

A 20% increase in sales from $10 million to $12 million would result in a proportional rise in variable expenses.

For ABC, variable cost would increase from $2 million to $2.4 million. And for XYZ, variable cost would increase from $6 million to $7.2 million.

The fixed cost for ABC and XYZ would remain fixed at $6 million and $2 million respectively.

Net profits for ABC jumped 80% while XYZ’s increased by only 40%! This is operating leverage at work. For ABC, a larger proportion of their expenses are fixed. When expenses don’t grow as fast as sales, net profit will grow at a much higher rate.

Operating leverage cuts both ways. For a company with high operating leverage, a decline in sales would cause net profits to decline at a much larger magnitude as well.

When revenue declines by 20% to $8 million, variable cost would decline to $1.6 million and $4.8 million for ABC and XYZ respectively.

Net profits for ABC declined a whopping 80% while XYZ suffered a 40% decline. Fixed expenses still must be incurred when sales decline. When expenses do not decline as fast as sales, net profit will tumble at a much larger rate.

Case Study: GameStop Corp (NYSE: GME)

Errors in analyst forecasts tend to be larger in businesses that have high operating leverage. Likewise, investors are often caught by surprise when investing in businesses undergoing a secular decline that have high operating leverage. As the decline in sales inevitably resulted in a much larger decline in earnings (and share prices).

Briefly, GameStop (GME) is a video game retailer largely in the USA. With the internet, sales have plummeted as Amazon took up its market share and platforms such as Playstation and Xbox began selling digital games directly, skipping a third-party retailer like GME altogether.

GME began to attract a lot of attention as ‘Big Short’ legend, Michael Burry, took a sizable stake in the company. The popular thesis was that the company has a ton of cash and a lot of value could be unlocked by GME repurchasing their shares. This would in turn create a short squeeze on the short sellers (the stock was heavily shorted).

Many investors focused on the potential upside as Burry took a position. But many missed the important fact that a company in secular decline coupled with high operating leverage could be disastrous to earnings.

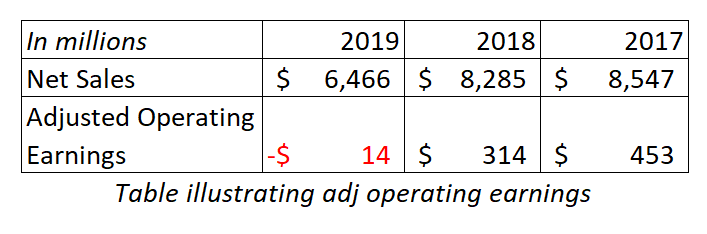

From their annual report, sales declined by 24%. However, it’s selling, general and administrative (SGA) expenses declined only 5%. This tells us that most of GME’s SGA expenses are fixed as reduced sales did not allow GME to save on SGA expenses. It still has to pay its employees and rent to run the business despite having fewer sales.

Adjusting for impairments, we are able to observe that operating earnings declined by a whopping 103%, from $453m to an operating loss of $14m, despite only a 24% decline in revenue.

Likewise, investors who bought in 2017 at $25 were caught off guard with the sharp decline in earnings. The stock tumbled 80% as it lingers around $5 today.

Key lessons

Here I will summarize the key learning points I hope you can takeaway:

- Operating leverage by itself is neither bad nor good.

- It works both ways, a company with rising revenue could potentially see a much bigger increase in earnings and vice versa.

- Companies with both high operating leverage and financial leverage will see greater swings in earnings.

- Companies with high operating leverage and financial leverage are often the biggest gainers off a market bottom.

- In the long run, all expenses are variable expenses.

I publish frequently at https://steadycompounding.com/

You can also follow my Facebook page for updates here!

Nice article, Thomas.

I am a newbie investor, having a few questions here

1.How do you know if the business has higher operating leverage or not in general? In the example, you showed the change in SGA, is it the amount of SGA+R&D?

2.Is the Op leverage depend on the industrial sector, that all companies in that sector has high Op lev? If so, what industrial sector?

3.So, what happened to Burry? Mike Burry was wrong on this one?

Hi Sikawat, thanks for reading!

1. I think a useful way is to track a company’s % change in SGA expenses against its revenue % change. In Game Stop’s case we can see that when revenue declined by 25%, the SGA only declined by 5%. It helps also to read footnotes of annual reports to understand what the SGA comprised of. For example, if it is largely operating leases (similar to rental expenses), we know that the company must continue paying even if business is bad. Otherwise, they will incur a large penalty.

2. There was a search done by credit suisse before called operating leverage: a framework for anticipating changes in earnings. In there they will publish the operating leverages by industry and rank them accordingly.

3. Currently he is trying to influence management to buyback shares aggressively as the company isn’t able to grow or create further value. Whether or not that will happen, only time will tell. But one thing for sure is that time is not the friend of a declining business.

Thx Thomas for your answers

Anytime 🙂 Hope I’m able to help with starting off your investment journey