Amazon share price has recently broken $3,000 per share and is currently trading at a lofty P/E of 147x. In fact, the company often trades above 80x P/E. Merely looking at the earnings would deter most value investors from owning Amazon.

Building on our income statement series on gross profit margins and marketing expenses, Amazon is the poster boy for not giving a hoot about reported earnings. Here is what Bezos has to say:

Bezos has an incessant focus on the Amazon’s long-term prospects. He emphasized a high return on invested capital (ROIC) by reinvesting relentlessly to become the market leader. He understands that for growth to deliver long-term value, the ROIC must be sustainably high.

Amazon built up its moat by spending aggressively on research and development (R&D). R&D expenses include developing new products and infrastructure to enhance customer experience and improve process efficiency:

Looking Beyond Reported Earnings

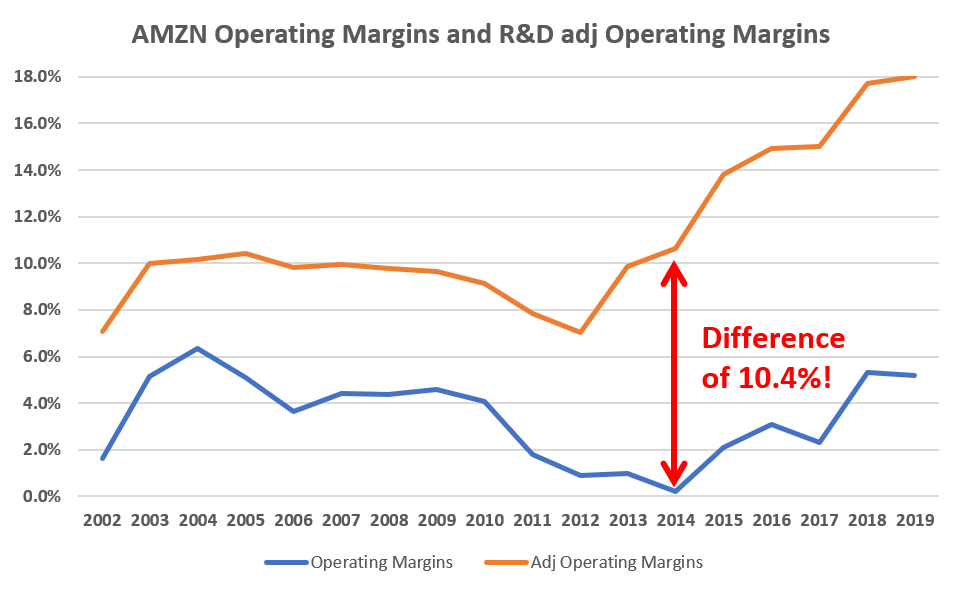

When we look at Amazon’s operating income, it looks rather mediocre. In 2014, the company made a meager $178 million in operating income on the back of $88 billion in sales, giving it a razor-thin operating margin of 0.2%.

Adding R&D expenses into operating income would paint a drastically different story. In 2014, Amazon spent $9.2 billion on R&D. Adjusting for R&D expenses would give the company an operating margin of 10.6%.

This is a consistent trend for Amazon over the years. On the surface, the operating margin continued to linger below 6% even in recent years. Adjusting for R&D expenses, we can observe that the margin has actually exploded upwards to 18%.

This is largely due to rapid growth from higher margins segment third-party seller services (3P) and Amazon Web Services (AWS) operating segment. This is the result of their aggressive investments in R&D earlier.

Capacity to Suffer

The “capacity to suffer” is key because often the initial spending to build on these great brands in new markets has no initial return. Many companies will try to invest smoothly over time with no burden on currently reported net income, but the problem is that when you are trying to invest in a new market, smooth investment spending really doesn’t give you enough power to make an impression. You end up letting in a lot of competition that will drive down future margins.

Tom Russo, Gardner Russo & Gardner

“Capacity to suffer” is a term coined by Tom Russo and it’s a key trait I look for in companies. It identifies companies that have the capabilities to look beyond short-term Wall Street expectations. Family controlled businesses or founders who have a majority of the voting rights are a common place to look for such businesses.

Amazon could have appeared very profitable if it wanted to, by pulling the plug on R&D expenses which drove growth and strengthened the company’s moat. But that’s not how Bezos does things. It always boils down to achieving growth and sustaining a high ROIC.

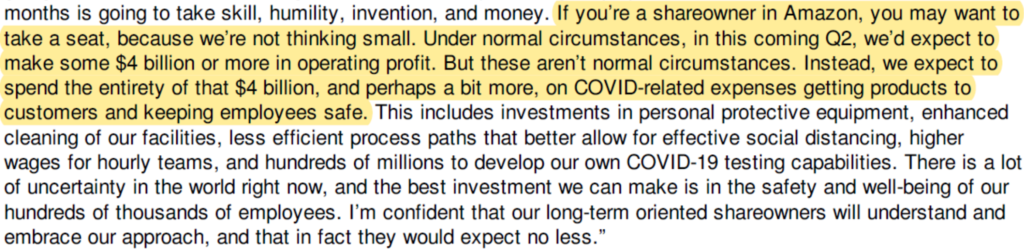

Here is my favorite statement from Bezos this year:

The Problem with GAAP Earnings

For digital companies, their economic engines are built on the back of R&D, brands (i.e. marketing efforts), customer relationships, software, and human capital. These intangible investments are akin to the traditional industrial company’s hard asset investments—factories, buildings, and machinery.

For the traditional hard asset investments, expenses are recognized over its useful life. A machinery with a 10-year lifespan that cost $10,000 would reduce the current year’s earnings by $1,000. This expense is recognized over its useful life of 10 years, given that wear and tear reduces the value of these assets over time.

However, for the digital company, investment in its economic engine is not capitalized as assets. Instead, they are treated as expenses and charged in entirety towards the current year’s earnings—despite intangible investments generally having multi-year benefits, or in certain cases, enhancing in value over time.

When a firm engages in R&D, marketing, software development, or training employees, it must charge these long-term value-creating expenditures the same way it recognizes general expenses such as office space rents in the current year period.

In short, there is a mismatch between the value delivered and the timing of recognizing the expenses. Also, these intangible benefits are not recognized as assets on the balance sheet.

Take Amazon for example—its value increases as it onboards more sellers, which in turn attracts more customers as it offers a great range of products and vice versa. Its value growth is driven by the network in place, not by increments of operating costs.

Hence, the most important thing for digital companies is to invest aggressively in their early years to achieve market dominance and command a “winner-takes-all” profit structure.

Here is a short excerpt from Marcelo Lima’s 2Q 2018 letter to Heller House fund clients:

“Winner-Takes-All” Structure

Since 1996, Amazon has grown revenue at a 50% compounded annual growth rate (CAGR). Even at its current size, adjusted operating income (excluding R&D expenses) grew at 28% CAGR for the past 5 years.

The eventual profitability is a result of continuous investment into the company’s economic engine to achieve market dominance in e-commerce and cloud (i.e., AWS).

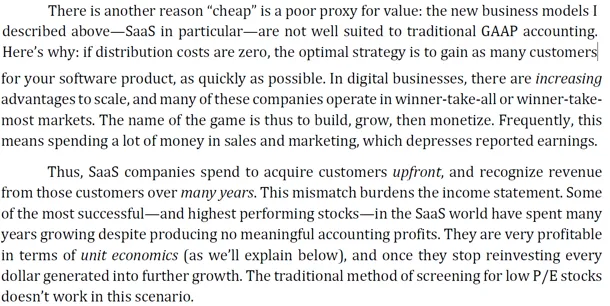

For Software-as-a-Service (SaaS) companies, many have spent years and tons of capital growing despite producing meager accounting profits or are running losses. They are profitable though, when evaluated in terms of unit economics, and when they stop investing every dollar generated into further growth (i.e. once market dominance is achieved). A good example would be Adobe.

In our next article, we will discuss how to analyze the unit economics of SaaS companies by looking at two important metrics—Customer Lifetime Value (LTV) and Customer Acquisition Cost (CAC).

If you wish to follow along, do subscribe to our newsletter or like our Facebook page for updates!

Conclusion

Where the key value driver of a company is in intangible investments, investors need to look beyond reported earnings. This is especially true for innovative companies in their early stage as they invest heavily in growth, which results in compressing their earnings and balance sheet assets.

Thank you for all these great articles on how to read an annual report and what to focus on in reading up one

Thanks for reading!

Hi Thomas,

I am still confused as Amazon, would continue to spend money on R&D and it will never stop paying R&D, R&D will recur every income statement, so how can we take this expense out?

what above Anon was talking about? did you write an article on how to read an annual report as well?

Hi Sikawat, that is a great question. Generally under the footnotes or during earnings call the management will explain how much of these ‘capex’ expenses are for the pursuit of growth.

Apart from adding back the expenses, another trick to spot a company like Amazon is to focus on its operating cash flows or free cash flows.

While the income statement shows that it isn’t profitable for quite some time, they became OCF positive at a much earlier stage. This is also largely due to their working capital advantage. Their suppliers are essentially funding part of their growth as well.

I haven’t wrote in detail how to read an annual report but I have written quite extensively on how to read the income statement.

I’m currently doing a 10-K challenge and you can follow me on @Steadycompound at twitter to see what I zoom into when reading annual report.

Thanks Thomas for your prompt reply, you mentioned ‘capex’, did you refer that to R&D in atypical sense?

Thanks

Yes! I was referring to the new form of ‘capex’, R&D and marketing expenses.

There’s an insightful chart which shows that investment in intangibles (i.e. R&D and marketing expenses) exceeded tangible investments at around 2015. I’ll send it to you if I find it!