“The most important thing [is] trying to find a business with a wide and long-lasting moat around it … protecting a terrific economic castle with an honest lord in charge of the castle,”

Warren E. Buffett

An economic moat is a term popularized by Warren Buffett, as he drew references to how business is like a castle, and having a strong moat is essential to deter invaders. Buffett invests in businesses that have a sustainable competitive advantage to protect themselves against competitors eyeing a slice of the market share.

Why should investors care about a company’s economic moat? The answer can be explained by the economic theory, mean reversion. Most of the time, investors & forecasters have a tendency to extrapolate the current trend. Companies that previously generated high growth are forecasted to continuously generate a high return and vice versa.

In reality, high returns will likely revert to the mean. Mean reversion is like gravity to returns on capital. An industry becomes attractive when incumbents generate high-returns on capital, enticing competitors to enter. New entrants will then compete for market share, which will in turn drive returns down for the incumbents.

Without a strong economic moat, high returns on capital would not be sustainable. Familiar examples that illustrate this trend in Singapore would be bubble tea, yogurt ice cream, poke/acai bowls, fried salted egg chips, etc… you get the point. Without a moat, the success of these trendy concepts will attract competitors to pop up and reduce the incumbents’ profitability.

The Outliers

That being said, there are companies that have defied mean reversion and continued to generate high returns on capital (in excess of 20%) for investors throughout the years. Some examples that spring to mind include Hermès, Costco, Facebook, Coca-Cola, and Illumina.

“When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

Warren E. Buffett

A company’s moat is either expanding or declining—it never stays stagnant. As investors, it is our job to determine if the business has a sustainable moat and evaluate if management continually investing to grow the moat. Popularized by Pat Dorsey, moats can be classified into the following categories: (1) Strong brands, (2) Patents or licenses, (3) Network effect, (4) Low-cost producer, and (5) High switching cost.

A Strong Brand Name

“It’s not Christmas or New Year until you see Coca-Cola ads.” Or so the saying goes. Occupying a share of consumers’ minds is no easy feat. Brands such as Coca-Cola, Ferrari, Hermès, and Tiffany & Co brands have been extremely successful in occupying a share of our minds, allowing them to earn a much higher return than their competitors.

To avoid this article becoming too long, we will discuss just one of the five moats—specifically, Ferrari (ticker: RACE) and how its strong branding has allowed investors to generate outsized returns over the years.

The Birth of Automobiles

Ever since the first introduction of cars in 1886, more than 2,000 carmakers have attempted to penetrate the market and most of them have ceased to exist. The automobile industry is notoriously competitive and capital intensive, companies often have to rely heavily on debt. Furthermore, it is also an extremely cyclical industry, where demand will taper off sharply (especially during times like these) as consumers will defer the decision to purchase a new vehicle when times are tough.

As a result, most carmakers have lumpy earnings and many generate negative Free Cash Flow (FCF), making survival in this industry very challenging. As an example, General Motors (GM) generated a cumulative negative FCF of -$50.9 billion over the last 5 years. And they have made up for this shortfall by aggressively piling on debt to survive.

“What you really should have done in 1905 or so, when you saw what was going to happen with the auto is you should have gone short horses. There were 20 million horses in 1900 and there’s about 4 million now (the year 2001). So it’s easy to figure out the losers, the loser is the horse. But the winner is the auto overall. 2000 companies (carmakers) just about failed.“

Warren E. Buffett

The Bright Red Car

Amidst the pack of car markers, Ferrari has the ability to charge astronomical prices for their vehicles. The power of the Ferrari brand is clearly evident here in Singapore. Despite our stringent speed limits and countless traffic lights, drivers still own Ferraris because the brand signifies status and affluence.

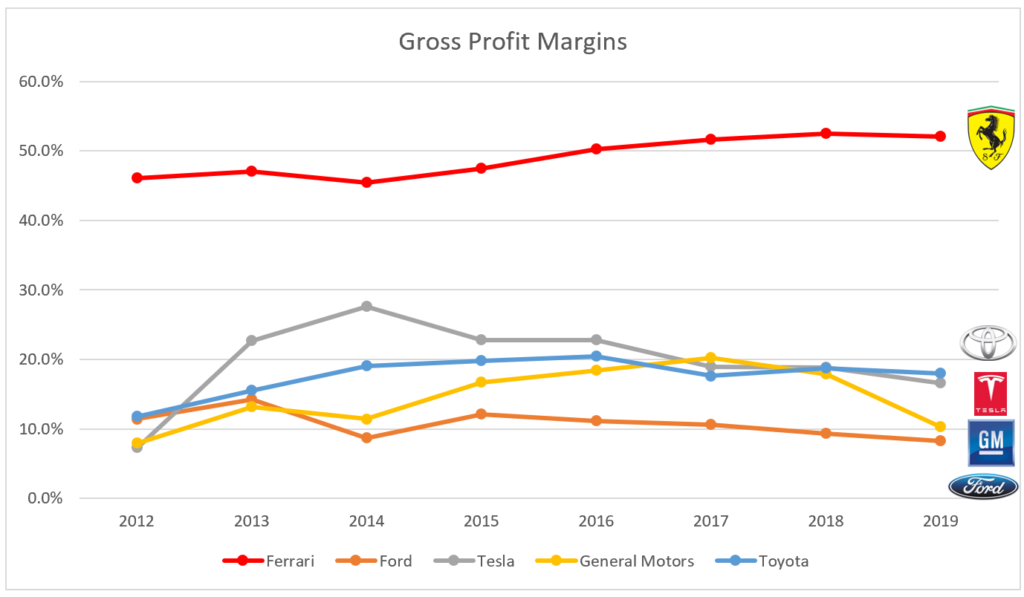

Ferrari’s moat allows it to earn outsized returns against other carmakers. The company has consistently commanded an average of 50% gross margins, while its competitors languish at an average of 15% gross margins.

In other words, the car which costs $50,000 to make can be sold at $100,000 for Ferrari. Its competitors, on the other hand, produce cars at the same cost of $50,000 but are only able to charge $59,000.

This fat margin leaves a lot of room for Ferrari to invest in widening its moat (e.g. invest in R&D and marketing) or to reward its shareholders.

Taking a look at their pricing power, Ferrari is able to command € 381,474 (SGD 588,000) per car on average. Competitors such as Ford and GM are only able to charge a fraction at $25,000 (SGD 35,600) and $16,000 (SGD 22,800) per car on average respectively.

Crisis-Proof

During the 2008/09 global financial crisis, we saw the United States’ new car sales plummeted by 40%, sending GM and Chrysler into bankruptcy while Ford had to take a substantial loan from the government just to stay afloat.

Car sales fell across the board for most carmakers, except for the company that made the bright red car. Despite the industry buckling down, Ferrari managed to see a 26% jump in the U.S. with its vehicles sold increasing to 6,587 in 2008, an increase of 122 from the previous year. And during 2019, it only saw a 1% decline in revenue.

The brand of Ferrari is so strong that its revenue growth continues to stay resilient through crises such as the 2008/09 financial crisis, Europe debt crisis, and trade war.

It targets the ultra-rich, and the company produces a limited number of cars each year. The long waiting list of up to two years, creates a real sense of exclusivity for customers who can get hold of one. Even if customers have the cash to purchase a new vehicle, there is a limited quantity. This discourages those on the waiting list from withdrawing their orders even during bad times. And even if they do drop out, there is a long list of customers eagerly waiting to take up their spot!

The moat surrounding Ferrari has proven immensely beneficial to investors. Since its spin-off in 2016, it has delivered a CAGR of 37.3%, delivering a 400% return prior to Covid-19 within a short span of four years. Comparing this result with Ford, GM, or even the S&P 500, Ferrari has generated astounding returns for its investors.

Conclusion

Having a strong brand that occupies a large share of consumers’ minds is a great moat that enables companies to sustainably generate high returns on capital. As investors of quality compounders, we need to monitor if management is engaging in activities that widen the company’s moat. Such activities include spending on marketing, increasing customers’ satisfaction, etc.

Nice article! Well done and keep it up!

Thank you for your kind words! I enjoyed reading your blog as well. Especially your updates on Value Investing Summits.

Hi Thomas,

Great article! Just two questions.

1)It seems like ASP have somewhat remained stagnant in the past few years, while cars sold has been consistently rising. Was just thinking, if volume sold continue to rise, do you see Ferrari losing that exclusivity to a higher pricing power? And if Ferrari is coming out with new, innovative models to adapt to consumer’s taste, will Ferrari’s GM be under pressure?

2) You also mentioned that Ferrari saw a jump in cars sold in 2008, and revenue only dipped slightly. Just curious, is this observation exclusive to Ferrari? Or is this trend prevalent across other luxury vehicles (RR, Lambo, BV)?

Thanks! Looking forward to your replies!

Hi MT!

Great questions.

1) It’s unlikely that their margins will come under pressure in the long run. In the short run, perhaps due to COVID-19, etc. Because for luxury products it has a funny dynamic, the more they charge the more people want to own it. With their branding, exclusive club and long waiting list I don’t see them losing their pricing power.

2) Yeah, this phenomenon only works on ultra-luxury products. Another one I can think of is Hermes, because they cater to the ultra-rich. Regardless of the economic cycle, it doesn’t really affect their spending power.

Thanks for the prompt response! Really good insights you have there!

Just another follow-up question. All in all, it seems like RACE’s revenue is highly driven, and somewhat dependent, on organic growth. Based on what you have researched, do you see RACE’s mgmt pursuing any near-term vertical/horizontal acquisitions to further drive growth? Because it seems to me that that’s a common growth strategy in the luxury goods sector, just like how LVMH grow over the years.

Thanks!

Good point! I see RACE following more of a Hermes playbook, whereby they just focus on existing products and generating value through price increases.

Great! Thx for the insights!