Earlier, we have covered the first three lines of the income statement – revenue, cost of goods, and gross profits. This allows us to calculate the gross profit margin (GPM), which measures pricing power and production efficiency. We also went through some of the common misconceptions about GPM.

Today, we are going to move further down the income statement – operating expenses. I pay special attention to this segment because this is where you can identify the characteristics of the next 100 baggers. Operating expenses include:

- Selling, general, and administrative costs (SG&A) – Salaries of headquarters staff, marketing expenses, and utilities bills.

- Research & development (R&D) – Salaries of staff doing R&D and its consumables used in developing new products.

- Depreciation – Fixed assets expenses recognized over time. E.g. A laptop costing $3,000 will be charged as $1,000 in depreciation expense over 3 years. Think about it as expensing it over its useful life.

- Amortization – Recognizing the impairment of intangible assets.

Update: The impairment of goodwill over 40 years has changed. It is not compulsory for companies to amortize goodwill over 40 years. Companies may opt for it to be evaluated for impairment on a periodic basis. If it is not impaired, the value will be carried on the company’s books indefinitely.

We are able to derive operating profits by subtracting the above expenses from the gross profits.

Operating profits = Gross profits – SG&A – R&D – Depreciation & Amortization

Dividing operating profits by revenue, we will obtain the operating profit margin (OPM). The OPM gives us clues as to how the management is managing operating costs compared to past years and compared to its competitors.

Reported Earnings versus True Earning Power

As usual, we are going to use case studies to understand these concepts. Reported earnings of high growth companies are often misunderstood by investors. Current earnings do not equate to real earning power.

Companies that are growing rapidly often reinvest heavily and their earnings are distorted as a result.

Earnings are the reported numbers. But real earnings power reflects the ability of the company to earn high rates of return on capital and grow at a high clip.

Companies that are able to generate high returns on capital and grow rapidly often will enjoy a big share price increase from multiple expansion and earnings growth.

Monster Beverage

Adapting from Chris Mayer’s 100 baggers, investing $10,000 in Monster Beverage would return $1,000,000 in 10 years. This is the essence of 100 baggers, the stock returning 100 fold your original investment. If held for 18 years it would have returned more than $7,000,000 (700 bagger!).

Monster copied Coca Cola’s playbook, by adopting a capital-light business model—focusing only on marketing and branding. They have no in-house manufacturing and have outsourced their bottling business.

At the start, Monster spent a disproportionately large percentage of its revenue on marketing (i.e. SG&A). The company understood that they needed to develop their competitive advantage by building up Monster’s brand and rapidly eat up market share.

Scaling and Building Its Moat

There are several reasons why Monster focused relentlessly on expanding market share and building up its brand:

- Economies of scale in marketing – Less advertising dollars are required to sell additional Monster drinks as it becomes increasingly popular.

- Lower distribution costs – Offer less discounts and distribution partners may offer concessions to retain Monster Beverage.

- Operating leverage – A dollar increase in sales will result in a multiple fold increase in earnings due to fixed cost.

Monster aggressively ramp up its marketing efforts. We are able to see that the marketing team grew by almost seven times within five years. The net sales per marketing employee stayed stable, suggesting that the company did not over-hire.

Monster’s investment in marketing paid off, as net sales increased more than six fold, from $96.5 million to $605.8 million within five years! We get net sales by subtracting promotions (e.g. discounts we see at the supermarket) from gross sales.

Lollapalooza Effect

As the Monster brand gains awareness and experience rapid growth, the benefits of rising bargaining power, and operating leverage kicks in:

- Increasing net sales/gross sales – Less promotions (discounts) were required to be given to retailers.

- Rising gross profit margins – Copackers and distribution partners offered concessions to retain Monster as their client.

- Rising operating margins – Due to operating leverage, operating income rose 32 fold! From $5.3 million to $171.3 million over 5 years. We can also observe this from the jump in operating margins.

This combination of positive factors stated above created a Lollapalooza effect. Investors watching the Monster story play out had until 2004 to jump on this ride before it began its ascent.

Warren Buffett on Marketing Expenses

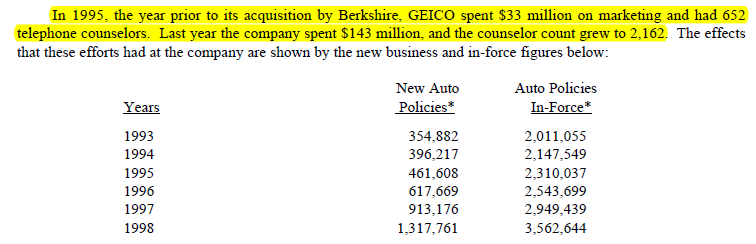

Buffett covered this topic extensively in his 1999 letter to shareholders. GEICO, the low cost car insurer owned by Berkshire Hathaway increased its spending on marketing from $33 million in 1995 to $242 million in 1999.

Buffett explained that he does not care if marketing expenses depress current year earnings. As long as the value of the brand outweighs the cost in the long-run. This is vastly different from most companies that are concerned about Wall Street’s estimates and would cut back on expenditure that increases the size of the moat.

He further illustrated that it probably wouldn’t cost this much to maintain GEICO’s brand position. However, with a large Total Addressable Market (TAM), the benefits from gaining scale was huge. GEICO had approximately 4.1% market share of the auto-insurance market back then.

Limitation of Accounting

Accounting rules require companies to recognize marketing expenses, R&D, etc as they are incurred. For example, GEICO spending $242 million in marketing would reduce its pre-tax profits by the same magnitude.

This is despite such expenditure providing benefits that go well beyond one year. Brand names such as Coca-Cola, Nike, etc. spent huge dollars on marketing. As a result, they dominate consumers’ minds and we favor these products over others when making our purchasing decisions.

As investors, we have to analyze the company’s operating expenses together with management’s strategy explained in conference calls and annual reports. It helps to ask ourselves these questions:

- Are the earnings depressed because they are aggressively spending to build up the company’s moat?

- Is the TAM huge compared to its current market share?

- Are the benefits of the company’s expenditures reflected in operating metrics such as higher sales, rising gross margins or operating margins (over time)?

- These must be evaluated in conjunction with the strategies laid out by management in the annual report and conference calls.

Our next article will discuss R&D expenses with Amazon as the case study. At first glance, Amazon looks like it has razor-thin operating margins. Diving deeper, it was actually a result of Jeff Bezos reinvesting a large portion of earnings back into the business to increase the size of the company’s moat.

If you wish to follow along, do subscribe to our newsletter or like our Facebook page for updates!

P.S. I strongly recommend Chris Mayer’s book 100 baggers to understand the essence of investing in high-quality compounders.

Thank you for another great read! I can’t wait for your next article about Amazon.

Thanks for this sharing. Just curious why is the scale in the share price graph not uniform? At first glance, it looks like the price didn’t grow as much after 2008, but that’s not the case. It shot from $8 to $67.

Tks for reading Simin! Yeah its amazing how Monster compounded. I think its because this graph is not on log scale in koyfin and Monster’s range is huge.