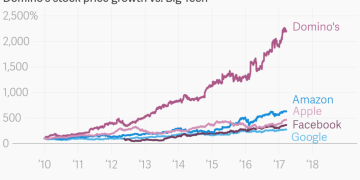

Investing Domino’s Pizza: How to Better Understand Restaurant Franchises by Thomas Chua October 25, 2020 6