I spent my week reading Terry Smith’s new book: Investing For Growth. Terry is the chief executive & CIO for Fundsmith Equity Fund.

I have been a fan of Terry’s presentations and writing because of his wit, humor, and candidness.

He is one of the fund managers who keeps it real.

Before I jump into what Terry has to say, it’s important to first start off with knowledge passed down by Warren Buffett on share buybacks.

Buffett on Share Buybacks

In Buffett’s 1999 letter, he highlights: “There is only one combination of facts that makes it advisable for a company to repurchase its shares: First, the company has available funds — cash plus sensible borrowing capacity — beyond the near-term needs of the business and, second, finds its stock selling in the market below its intrinsic value, conservatively-calculated.“

Capital must always be first deployed for business needs. This comes in two forms.

First, expenditures must be made to maintain its competitive position (e.g. remodeling of Starbuck’s stores).

Second, capital should be reinvested for growth when management expects that it will produce more than a dollar of value for each dollar spent (e.g. opening more Starbuck’s stores in China).

In other words, capital should be deployed where return on invested capital exceeds cost of capital.

After ensuring that the business needs are taken care of, share buybacks create value for shareholders only when the current market price is below its intrinsic value, conservatively estimated.

Let’s illustrate this with numbers!

How Buybacks Increase or Destroy Value

Imagine you own ABC Corp with two other friends, Joe and Julie. Let’s say ABC Corp’s intrinsic value is conservatively estimated at $3,000.

The three of you own an equal share of ABC Corp, at $1,000 each.

For some reason, Julie decided to sell her stake back to ABC Corp, intrinsically worth $1,000.

Scenario 1: ABC Corp Buyback at 20% Discount

If ABC Corp buys back Julie’s stake at $800, ABC Corp’s intrinsic value would now be $2,200 ($3,000 – $800) after the transaction.

This means that Joe and yourself now own 50% each of ABC Corp, an increase from 33%.

The value of your ownership increased from $1,000 to $1,100 (50% X $2,200).

Share buyback has created value for existing shareholders.

Scenario 2: ABC Corp Buyback at 20% Premium

If ABC Corp buys back Julie’s stake at $1,200.

ABC Corp’s intrinsic value would now be $1,800 ($3,000 – $1,200) after the transaction.

Similar to scenario 1, Joe and yourself would now own 50% of ABC Corp.

But, the value of your ownership would have decreased from $1,000 to $900 ($1,800 X 50%).

Share buyback has destroyed value for existing shareholders.

Scenario 3: ABC Corp Buyback at Fair Value

If ABC Corp buys back Julie’s stake at $1,000, its intrinsic value would now be $2,000.

Both Joe and yourself would own $1,000 of ABC Corp. No change from before.

In this case, share buyback does nothing for existing shareholders.

Terry Smith on Accelerated Share Repurchases

Ordinarily, share buybacks are usually done over weeks or months with multiple transactions. The amount of buyback done each day during this period depends on the volume of shares traded.

Hopefully, the share prices remain depressed during this period as the company buyback shares.

In accelerated share repurchases (ASR), the company does a significant share buyback programme in a single transaction with an investment bank or a small group of banks.

The investment bank(s) will make a short sale to the company by borrowing the shares from the market.

Thereafter, the investment bank will purchase shares to cover its short position. And of course, fees are involved in this.

A huge share buyback programme like an ASR is bound to generate share price rises at least in the short-term. No sane company would short shares knowing that they would need to cover up their position by buying at higher prices.

But this is exactly what ASR does. The investment bank would short shares at X dollars and buyback the shares at greater than X dollars. Of course the investment bank will not bear the losses of this short position.

On top of charging a hefty fee for providing this service, the losses it incurs by covering its short position will be passed on to the company.

This is exactly what IBM did in May 2007. In a 118.8m share ASR, it paid an initial price of $105.18 per share for shares purchased from the investments bank’s short sales totaling $12.5b, and then another $2.95 per share or a total of $351m to cover the high price of $108.13 at which the banks eventually closed their shorts.

They have effectively agreed to write a blank cheque to the investment bank to cover the cost of short-selling its shares. When it comes to short-selling, the potential of loss could be ‘unlimited’.

Who knows how far the share prices will shoot up when the market knows that the company started an ASR?

Study Management’s Remuneration

Generally, when the management is overzealous in buying back shares in good times and in bad, we can trace the reasoning back to how managements’ bread is buttered.

Many of them are filling up their pockets rather than shareholders’.

Two companies we are familiar with — Domino’s and Starbucks, have loaded up their balance sheet with debt to repurchase shares.

Today, let’s take a look at Starbuck’s leadership compensation plan.

You will notice that management is paid based on largely 2 short-term factors (over 3 years): (1) Earnings Per Share (EPS) and (2) How Starbucks share price performs against the market.

Share buybacks would help to financially engineer EPS by reducing the number of outstanding shares. Also, continuously buying back shares will likely prop up the share prices due to increased buying demand.

Starbuck’s management unleashed a huge share buyback programme. Back in 2019, it committed to return $25b on an $80b market cap.

It financed this by loading up its balance sheet with $5b worth of debt and by selling to Nestle the rights to sell Starbucks consumer package goods in grocery stores (e.g. coffee capsules and bottled coffee) for $7.15b (fantastic deal for Starbucks in my opinion).

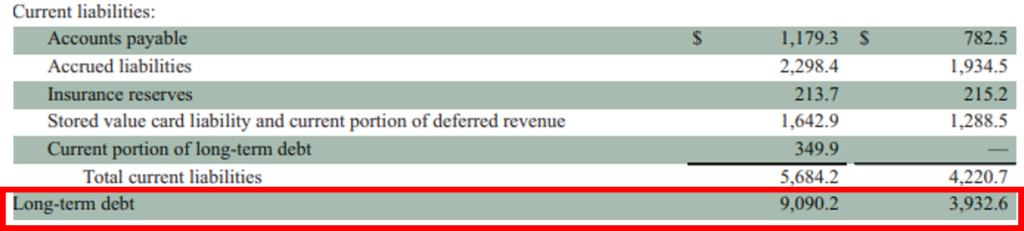

Here, we can see from long-term debt swell up on its balance sheet:

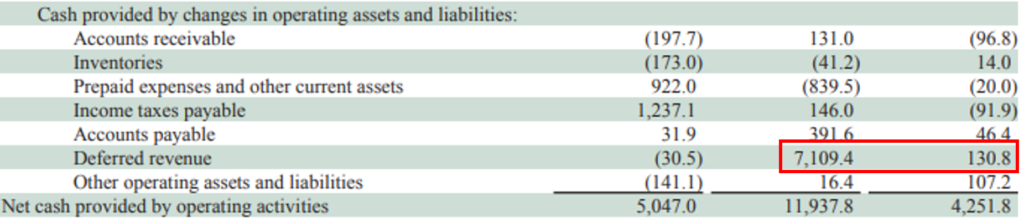

And the cash that came in from the Nestle deal (recorded as deferred revenue back then because Nestle made an upfront payment):

Some argue that the management did the right thing by taking on debt to buy back shares because of the record low-interest rates.

Of course in 2019, when all was going well, Starbucks had more than enough cash flow to cover interest payments.

But this put the company in a precarious position. In my opinion, there’s is no need to accelerate returns by taking on debt. Especially when it makes the company more fragile to black swan events.

This is akin to what Buffett said, “it’s insane to risk what you have for something you don’t need.” With its strong cash flow and proceeds from the Nestle deal, Starbucks was in a strong position to buyback shares. There’s no need to be that aggressive and take on debt.

And true enough, 2020 gave us the biggest of black swan in the form of COVID-19.

Not gonna lie, when Starbucks stores were shutting down early this year, the debt on their balance sheet made me sweat. I began stress-testing the company to find out how long can the company survive without revenue.

You can read more about it here.

Conclusion

Share buybacks increase value only if they are done below intrinsic value. The problem arises when management are incentivized based on short-term metrics such EPS and share price performance. Management could engineer the results by misallocating capital (share buybacks or worse, ASRs) at the expense of shareholders.

Thank you for taking the time to read my blog.

If you’re enjoying the content so far, I’m sure you’ll find 3-Bullet Sunday helpful.

As an extension to the regular posts, I send out weekly newsletters sharing timeless ideas on life and investing.

I do not share this content elsewhere.

Join others and subscribe to our newsletter today to receive a free investment checklist!