Software as a Service (SaaS) companies’ share prices skyrocketed since March 2020 as the market recognized that COVID-19 has caused rapid digitalization. SaaS companies also have a fantastic characteristic – recurring revenue.

Understanding Its Moat

Despite most of the SaaS companies commanding lofty valuations, not all of them will meet the high expectations set out by investors. We have to first ask ourselves if this company has a moat – e.g. high switching costs.

Is it easy for competitors to woo their customers over?

Consider Adobe and Zoom, both offering their software services for a subscription fee.

Most designers will find it impossible to switch from Adobe due to the amount of time spent learning the software. They’re taught this in school and would be very resistant to master another designing software. Doing this would be akin to having to pick up another language for work.

Zoom’s success has been dependent on its user interface — its ease of use. You don’t have to set up an account and it is not cluttered with buttons. However, ease of use is a double-edged sword. Users can easily switch away when Zoom stops innovating and delivering added-value to fend off competition.

Comparing Adobe and Zoom, Adobe has a much stronger moat (i.e. switching cost). Its users are locked in and thus Adobe is able to extract value for a longer period (higher lifetime value).

This is important as SaaS companies spend huge capital outlay (i.e. sales and marketing expenses) in acquiring customers. With distribution costs near zero, the optimal strategy is to acquire as many customers as possible.

Read earlier articles on marketing and R&D expenses to understand why SaaS companies appear unprofitable at first!

Its returns are highly dependent on its ability to retain customers. Bringing us to our first metric – churn rate.

Churn Rate

Churn rate measures the percentage of customers who canceled their subscription over the period. The best way to think about this is how much gross profits were lost as a result of customers canceling their subscription?

The churn rate provides us insights into how sticky the software is and it is a key determinant of profitability for the company.

Lower churn rates equate to longer customer lifespan. This directly translates to higher lifetime value (LTV) of each customer.

The longer a customer stays subscribed, the more value may be extracted from the initial capital outlay – customer acquisition cost (CAC).

Churn rate may be expressed in the formula below:

For example, you have 100 users each paying $100 per month for your software. Taking the typical gross profit margin of 80% for most SaaS companies (GPM ranges between 75% – 80% for mature SaaS companies).

This gives us a gross profit of $8,000 per year (100 x $100 x 80%).

Say 20 users dropped out that year, resulting in a loss of $2,000 in gross profits ($100 x 20). The churn rate would come up to 25% ($200/$800).

Customer Lifespan is simply the inverse of churn rate. With a 25% churn rate, the projected customer lifetime is 4 years (inverse of 25%).

Understanding the churn rate will allow us to know the Lifetime Value (LTV) of a customer.

Lifetime Value

LTV is how much I can expect to receive from each customer on average over the lifespan of their subscription.

LTV may be expressed in the formula below:

Knowing the LTV gives me an idea of whether the customer acquisition cost (CAC) provided good returns.

It helps answer the question—Did acquiring these customers bring in more profits than what it cost?

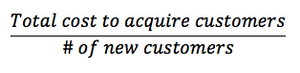

Customer Acquisition Cost

CAC is the total sales and marketing cost to acquire each customer. This includes items such as salaries of sales staff, advertisement expenses, and everything else it took to successfully onboard the customer.

CAC may be expressed in the formula below:

Let’s say it costs $1,000 in a year to acquire 100 new paying customers. Our CAC will be $10.

In other words, it costs, on average $10 to bring in one new customer!

By knowing the LTV and CAC, we can understand if the company can make more profit from a customer than the total cost of acquiring them.

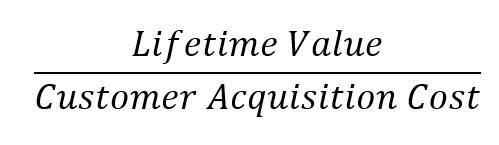

Unit Economics

Unit economics is simply an evaluation of profitability on a per-customer basis. Copying Buffett’s euphemism, CAC is what you pay and LTV is what you get. SaaS companies are ‘profitable’ if LTV exceeds CAC.

A useful way to evaluate this is to look at the LTV to CAC ratio:

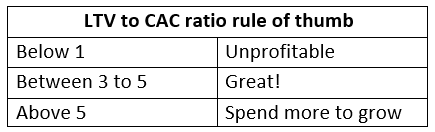

Ideally, this ratio should be between 3 and 5. The company’s customers are providing profits three to five times the cost to acquire them.

If it is below 1, that would mean that the cost spent to acquire a customer is higher than their lifetime value. Some companies start off with below 1 to get a network effect going (e.g. Grab and Uber offering massive discounts initially). However, this is ominous if it persists over a prolonged period.

If it is above 5, the company could be missing out on valuable opportunities. Customers are bringing in huge returns and companies may want to spend more on sales and marketing to quickly scale the business.

Update: Insightful discussion on LTV-CAC ratio with the team from Moneywisesmart below:

The timing of the LTV would affect the Internal Rate of Return (IRR) of customers (time value of money). Also, shorter payback times are advantageous as less working capital is required. This in turn provides companies the ability to scale faster.

Conclusion

It is important to understand the LTV vs CAC trade-off when evaluating businesses. Especially for SaaS companies, this metric must be closely studied to understand its profitability.

Bluegrass Capital put it across succinctly, “If I can find a company that invests $1 in acquiring a customer and they can get back $3 to $5 in gross profits, it doesn’t matter to me if the EBITDA margin is negative or positive.”

For many of the SaaS companies today, they are spending heavily today to scale. These companies will not appear profitable today but would be highly profitable in the future, provided they have a strong moat and sound unit economics.

To end off, I will re-share this gem from Marcelo Lima’s 2Q 2018 letter:

In our future article, we will go through a case study on evaluating a SaaS company.

If you wish to follow along, do subscribe to our newsletter or like our Facebook page for updates!