10-K Challenge: I aim to read a 10-K every day and tweet my learning point(s) daily for the next 30 days. Join me on @SteadyCompound as I try to be 1% better every day.

Michael Mauboussin has written countless white papers on this topic. His paper published on 9 Jun 2020 introduced the concept of how stock duration and interest rates caused multiples of high-quality companies to justifiably shoot up.

High-quality companies have the following characteristics: Return on capital is significantly higher than the cost of capital, the company is able to grow, and the company has a competitive advantage (i.e. a moat).

How is Value Created?

Before we jump into new concepts such as stock duration, it is important to quickly recap how value is generated.

A company creates value only when its investments generate a return higher than the opportunity cost of capital (COC).

This means that having a large total addressable market (TAM) with huge growth prospects does not make a good investment. Revenue and earnings may show growth but it offers little with respect to value creation.

If a company generates a return on capital equaling COC, then it does not matter whether they grow. They are both worth the same multiple.

Mauboussin refers to this group of companies as commodity businesses that deserve a commodity P/E multiple.

The Commodity P/E Multiple

The commodity P/E multiple is the multiple you would pay for $1 of earnings into infinity assuming no value creation (return on capital = cost of capital).

You can find out the multiple by taking the inverse of the cost of equity capital. If the COC is 8%, the commodity P/E multiple is 12.5 (1/0.08 = 12.5).

This multiple is not constant. The multiple a commodity business commands is derived from the cost of equity capital for each period.

The Concept of Duration

Duration is a concept that bond investors would be familiar with. It measures how a change in interest rates would affect the price of a bond.

The faster an investor is paid back, the lower the duration. The longer it takes to be paid back, the higher the duration.

Here’s a simplified example.

Assume a five-year $100,000 bond at 5%. This means the bond will pay you $5,000 at the end of every year.

This would all be fine and the price would remain the same (at $100,000) if interest rates doesn’t change.

If interest rates shot up to 10%, investors would expect to be paid 10% for their investments.

To achieve this interest rate, the $100,000 bond paying $5,000 (5%) annually would have to drop its price to $50,000. Only then it will be able to match the 10% interest rates given by the current market ($5,000 interest on $50,000 bond).

Generally, the longer it takes for an investor to be repaid, the higher the duration will be. Accordingly, the bigger the magnitude the change in bond prices will be when interest rates shift.

How Duration Affects Stock Valuation

Similar to bonds, stocks of businesses that reinvest heavily in the short run to generate higher cash flows in the long run have longer durations than companies that lack the opportunities to reinvest.

Duration sheds important insight into understanding the magnitude of an asset price change when interest rates change. Mauboussin highlights, “Long-duration assets are more sensitive to changes in interest rates than are short-duration assets…companies that can invest a lot today at high returns on capital will not only grow faster than the average company, their stocks will have valuations that are more sensitive to changes in the discount rate.“

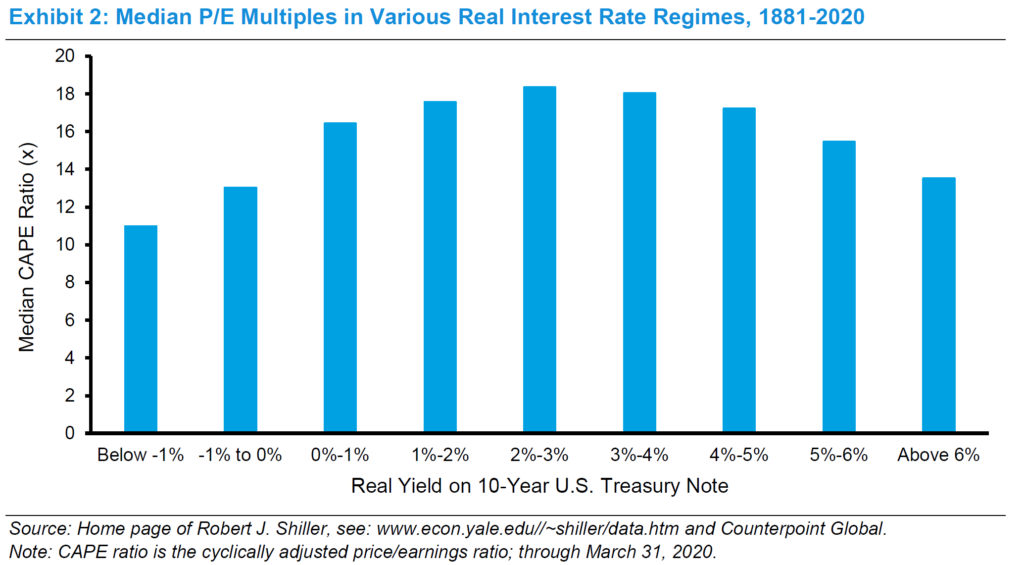

Low Interest Rates

Low interest rates are frequently associated with poor economic outlook and slow real earnings growth. This creates a conundrum where low interest rates raise asset values (i.e. higher value for a stream of cash flows due to lower discount rates), but the prospects are reduced by slower expected cash flow growth.

Data from Robert Shiller suggests that the impact of slow growth will outweigh the former. The P/E multiple for the market has followed an inverted “U”.

Low median P/E multiples are associated with very low and very high interest rates while high median P/E multiples are associated with real interest rates in the middle of the range.

Mauboussin continues to explain, “Research shows that low Treasury yields allow industry leaders to generate excess returns and that the magnitude of those returns increases as yields approach zero. While the median P/E may come under pressure as a result of slower growth prospects, a handful of companies may continue to generate strong growth and return on incremental investment.“

How the Math Works Out

Impact of growth rates on valuation

Mauboussin demonstrated how low-interest rates leads to bigger shifts in valuation multiples with the following:

Assuming the base year’s earnings are $100, slowing earnings growth from 10% to 7% reduces next year’s earnings by only 2.7% (from $110 to $107). However, the P/E multiple dropped a steeper 22.9% (from 32.3 to 24.9).

“Investors often calculate the P/E multiple using the current price and next year’s earnings. As a result, they sometimes believe that the market overreacts to what appears to be modest changes in the near-term earnings. But if expectations for the trajectory of growth really do shift down, the large apparent drop in the P/E multiple is completely justified.

Here, next year’s earnings are revised down by 2.6% (from $115 to $112) but the P/E multiple decline is 25.3% lower. When return on incremental invested capital (ROIIC) is well above the COC, the value of the business is very sensitive to changes in the growth rate of NOPAT.

As we can observe in the following graph, growth and the P/E multiple have an exponential relationship. In other words, small changes in growth expectations can lead to big changes in the P/E multiple.

This effect is amplified when the company growth rates are high.

“Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous.”

Warren Buffett

The key takeaway here is that growth doesn’t matter for businesses that generate returns close to the COC. However, for companies that are able to generate high returns on capital, it is a huge amplifier of value.

Impact of ROIIC on valuation

ROIIC indicates how much a company is required to invest to attain an assumed growth rate. A high ROIIC means that the company don’t need to invest heavily to grow, leaving a lot of cash on the table for shareholders and vice versa.

Take for example company A and company B, both of them aim to generate a 10% growth in earnings for the next year. From current year earnings of $100 to $110, an additional $10 in earnings.

All else constant, A generates 50% ROIIC while B generates only 25%.

A is only required to invest $20 of the current year’s earnings to achieve an additional $10 ($20 x 50%) in earnings the following year. This leaves $80 of the remaining earnings for its shareholders.

While B is required to invest $40 of the current year’s earnings to achieve an additional $10 (25% x $40) in earnings the following year. Leaving only $60 of the remaining earnings for shareholders.

Thus, a company generating higher returns on capital would rightfully command a higher multiple, assuming growth rates are constant.

Impact of discount rate on valuation

The cost of equity is comprised largely of two components – the risk-free rate (i.e. commonly referred to as the yield on the 10-year Treasury note) and the equity risk premium (i.e. how much investors expect in return for assuming risk).

As of 1 Jun 2020, Aswath Damodaran’s estimate of the cost of equity dropped to 6%. The 10-year Treasury note offering historically low yields at 0.7%, while the equity risk premium accounts for 5.3%.

Mauboussin observes, “Nearly 90% of the expected return from equities now comes from the risk premium, up from about 75% at the beginning of the year.”

Importantly, long-duration assets are highly sensitive to changes in the discount rate. In today’s environment of low expected returns, the valuation of these companies are substantially higher than before.

Conclusion

Nobody will know where interest rates are headed, but it is important to appreciate the relationship between the discount rate and long-duration assets. In other words, we should be mindful that an increase in interest rates will bring down the valuation of companies that are investing heavily today for higher future cash flows tomorrow.

It is also important to bear in mind that for most companies, return on capital will eventually drift lower with competition, maturation, obsolescence, and disruption. Without a moat protecting its returns, the company will suffer a multiple contraction as observed above.

You may find all of Michael Mauboussin’s work here.

Thank you for taking the time to read my blog.

If you’re enjoying the content so far, I’m sure you’ll find 3-Bullet Sunday helpful. As an extension to the regular posts, I send out weekly newsletters sharing timeless ideas on life and finance.

I do not share this content elsewhere.

Join others and subscribe to our newsletter today to receive a free investment checklist!

This is wonderful Thomas! Clear and relevant. Chanced upon your writing after your post in Seedly and I must say that you inspire me to keep reading up on personal finance and to write about it too. Had taken a brief hiatus from such readings upon becoming a mom. But the authors you’ve cited really do resonate with me and I’m going to start exploring these topics deeper now! Thank you!

Congrats on being a Mom and thank you for your kind words! They made my day 🙂

I look forward to reading what you write in the future.