“It’s not share of market. It’s share of mind that counts.”

—Warren Buffett

The happiest place on earth. It is near impossible to replicate Disney’s share of mind even if you have all the money in the world.

The Disney name is well-known to billions of people. It has a meaning—an emotion perhaps—attached to it globally.

It is hard to find another brand that is unanimously known as the happiest place on earth.

With Disney+, it is now possible to ship this happiness at an unprecedented scale.

Creating Movies Profitably

In Berkshire’s 1996 annual general meeting, Buffett explained why Disney makes money for shareholders, unlike many other movie companies.

Most movie companies are able to make a lot of money. But they make a lot of money for everybody else (e.g. acting cast, directors, etc) except for the shareholders.

Buffett shares, “The nice thing about the mouse (Mickey) is that he doesn’t have an agent… He is not there renegotiating (his salary).. every week or every month and saying, “Just look at how much more famous I’ve become in China.””

From 2006 to 2019, Disney made 44 films. Each film brought in an average of…

$850 million!

Pricing Power

“The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business. And if you have to have a prayer session before raising the price by 10 percent, then you’ve got a terrible business.”

Warren Buffett

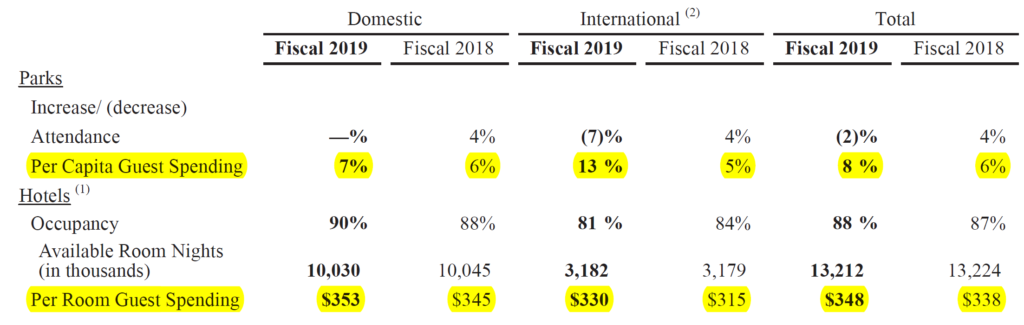

For Disney, let’s take a look at their pricing power pre-COVID-19.

Like clockwork, Disney theme parks, hotels, and cruises have been able to raise prices at approximately 5% per year.

Coming off a low base, Disney+ is set to raise its price from $6.99 to $7.99 after just 1 year since launch. In sales, it is always easier to sell an incremental dollar as compared to the first dollar.

The Oil Field that Keeps Gushing

Disney’s intellectual property (IP) is like an oil field that doesn’t dry up. We have seen the remakes of Beauty and The Beast, The Lion King, Aladdin, and many more.

Furthermore, IP created generates value beyond the box office. Box office hits will be translated into merchandise which ranges from toothbrushes and quilts, to figurines, watches, LEGO, and more.

A quick search for Elsa will show you an endless array of products that could bring a smile to your daughter’s face.

Buy her a counterfeit Elsa and you will see her smile melt faster than Olaf in the summer.

The oil field doesn’t end here. The benefits will trickle down to its theme parks, resorts, vacations, and cruise packages.

Disney+

“Disney is an amazing example of autocatalysis… They had all those movies in the can. They owned the copyright. And just as Coke could prosper when refrigeration came, when the videocassette was invented, Disney didn’t have to invent anything or do anything except take the thing out of the can and stick it on the cassette.”

Charlie Munger

With Disney+, the value of all the past IPs can be unlocked at scale. As Netflix’s and Spotify’s subscription-based business model suggests, monthly subscription fees are very sticky. They provide upfront, recurring revenue for Disney.

This is different from the traditional way of spending hundreds of millions of dollars upfront (e.g. Frozen costs $150 million), which locks up tons of working capital before the movie is released, reducing the amount of free cash flow for shareholders in order to grow its IP by producing more movies.

Depending on whether the movie becomes a hit, Disney would have difficulty estimating how much cash flow will be coming in. This leads to difficulty in budgeting for new projects.

This is all about to change with Disney+.

In its investors day on Dec 2020, Disney exceeded 137 million in paid subscriptions across its Direct-to-Consumer (DTC) services, smashing all of its earlier estimates.

Disney+ alone produced 86.8 million subscribers, with the rest coming from Hulu, ESPN+, etc.

To put it in context, it took Disney approximately one year to achieve what Netflix did in 10 years in subscriber count.

Disney+ estimates have been revised from 60 million to 90 million to 230 million to 260 million subscribers by 2024.

Netflix currently generates approximately $10USD per subscriber monthly. Applying that to Disney+, this will bring in $2.3 billion to $2.6 billion in upfront recurring revenue monthly, or $27.6 billion to $31.2 billion annually.

Data Is the New Gold

With Disney+, imagine all the data the company will be able to collect. It will have deep insight into how Disney fans interact with its content, potentially increasing its revenue per Disney fan.

Oh, your son watched Iron Man for the third time in the past two months, here’s an ad on how he could look like Iron Man!

Ride of a Lifetime

With Robert Iger’s 15 years at the helm, Disney has undergone some massive transformation.

In his book Ride of a Lifetime, Iger started making several gutsy moves once he took over. Taking over Pixar for $6.3 billion, bringing the world of Toy Story, The Incredibles, and Monsters Inc into Disney.

The acquisition of Pixar brought in Steve Jobs to Disney’s board of directors. Prior to the acquisition, Disney’s animation business had been struggling.

Disney then went on to acquire Marvel for $4.2 billion in 2009 with Avengers: Endgame raking in $2.8 billion in global gross box office receipts.

What seemed like expensive acquisitions turned out to be great deals.

After owning the world’s most valuable superhero property, Disney followed up by acquiring Lucasfilm (Starwars, Indiana Jones, etc) for $4.1 billion in 2012.

And of course, let’s not forget the biggest acquisition of the Twenty-First Century Fox, which closed in Mar 2019. This ended up costing $71.3 billion, flooding their balance sheet with debt.

All these moves required hard work in convincing the board of directors. But Iger understood that Disney’s moat is with its IP and he has executed beautifully by churning out blockbuster after blockbuster.

After his 15 years of service, Iger has set Disney up nicely for its big move into streaming—Disney+.

Disney’s Legacy Business

Disney media networks segment comprise of cable networks and broadcasting. It currently contributes approximately 25% of the operating income for Disney.

Operating margins for this segment have been declining over the years due to cord-cutting.

Streaming companies (Youtube, Netflix, and IGTV) are eating up traditional TV’s market share (eyeball time), much like what blogs, Facebook, and Google did to traditional newspaper advertising revenue.

With this as the backdrop, Disney+ seems to make sense from a long-term perspective.

In the short term, Disney is likely to face some pressure from this segment as it keeps its best content for Disney+. But it will benefit from its streaming business tailwind in the longer term.

This is similar to Adobe’s playbook when they first transited into a subscription model. Revenue would have been impacted in the short-term as they cannibalized their existing business. In the long-term however, the predictable upfront recurring cash flow will greatly benefit the company.

Conclusion

It is hard to find another brand that invokes a positive emotion and creates blockbuster hit after blockbuster hit. With Disney+ coming up huge amongst consumers, Disney stands to benefit hugely from introducing streaming into its ecosystem—upfront predictable cash flow, monetizing past content, data, and increased revenue per Disney fan.

Disclaimer: This is not a recommendation to buy or to sell securities. Please conduct your own due diligence or consult your advisor. I merely write to improve my investment and thought process.

Thank you for taking the time to read my blog.

3-Bullet Sunday is a free, weekly email, that hones your mind and keeps you growing. It is full of timeless ideas on life and finance.

Subscribe today to get weekly insights and receive a free investment checklist!