If you enjoy stocks research reports like this, become a member and gain access to all my research on companies such as Amazon, Alibaba, Crowdstrike, Google, Microsoft, Netflix and more.

>> Click here to gain access to all my stocks research

In my early investment days, Peter Lynch’s “One Up On Wall Street” gave me an important insight: cyclicals are often misunderstood. As opposed to staples like groceries and toothpaste-or even gelato if that’s your thing-automobiles are big ticket items which are typically put off when times are tight.

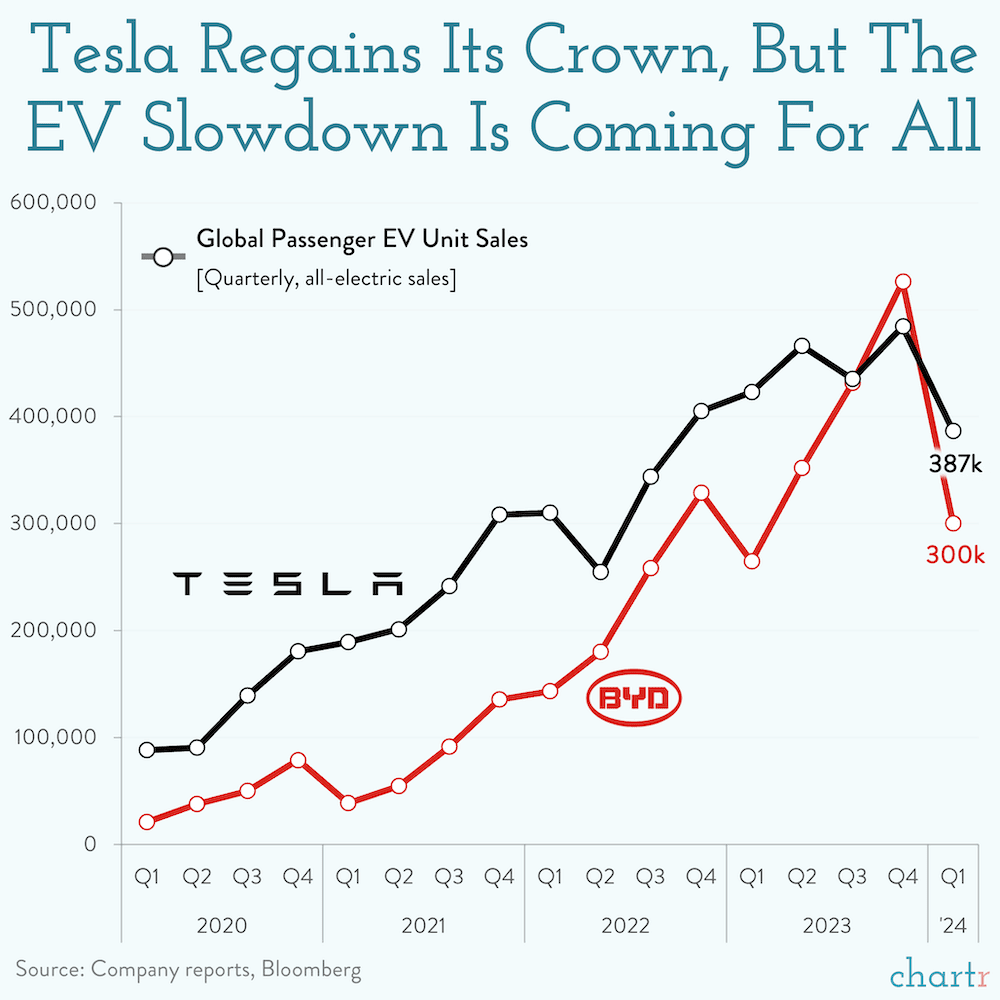

A rising interest rate environment and inflation have tightened consumer budgets, and the EVs industry has indeed felt the pinch. Tesla’s stock has plunged 40% this year, making it the worst performer among the magnificent seven.

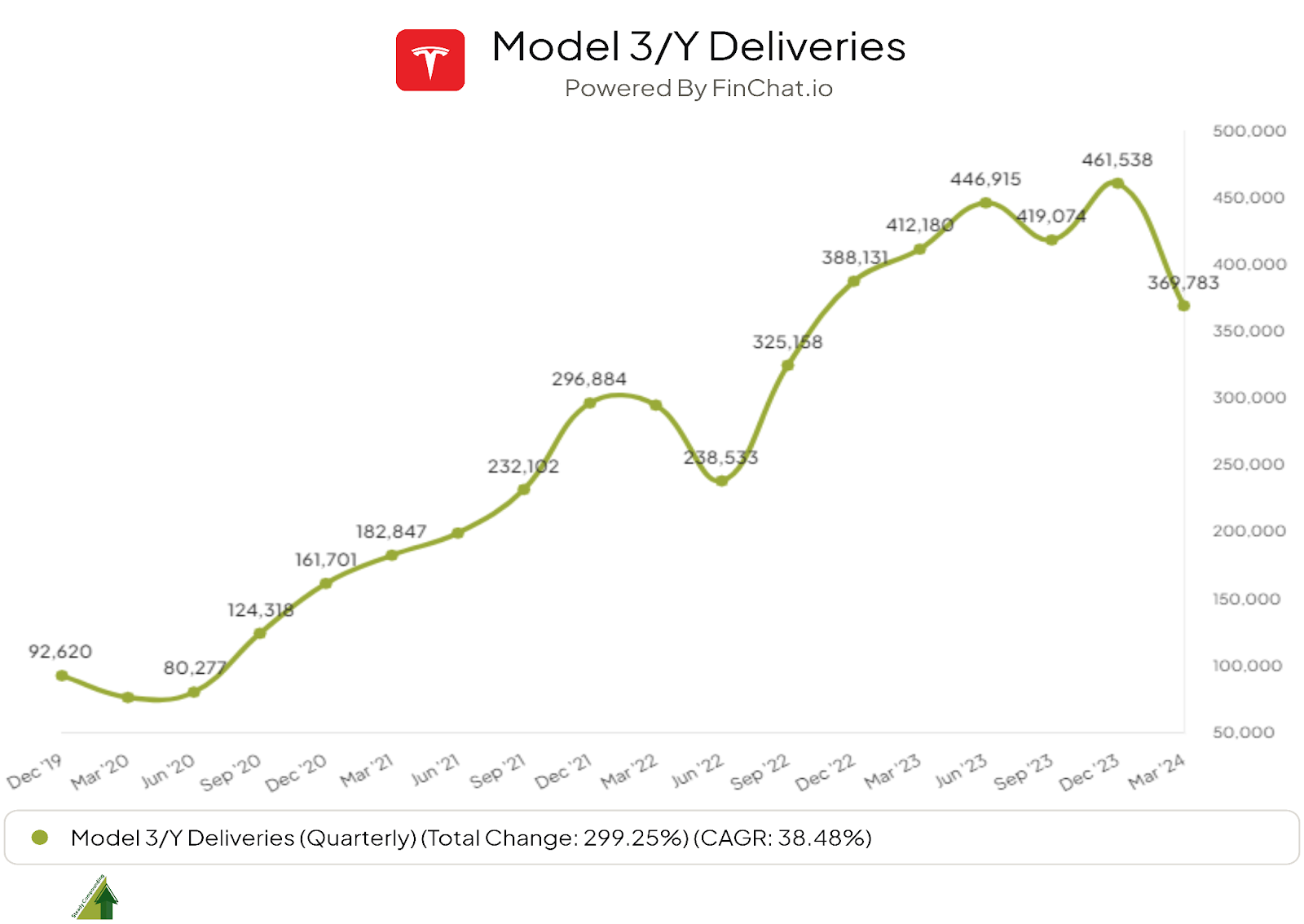

Recent delivery numbers have disappointed, marking the first year-over-year decline in Model 3/Y deliveries.

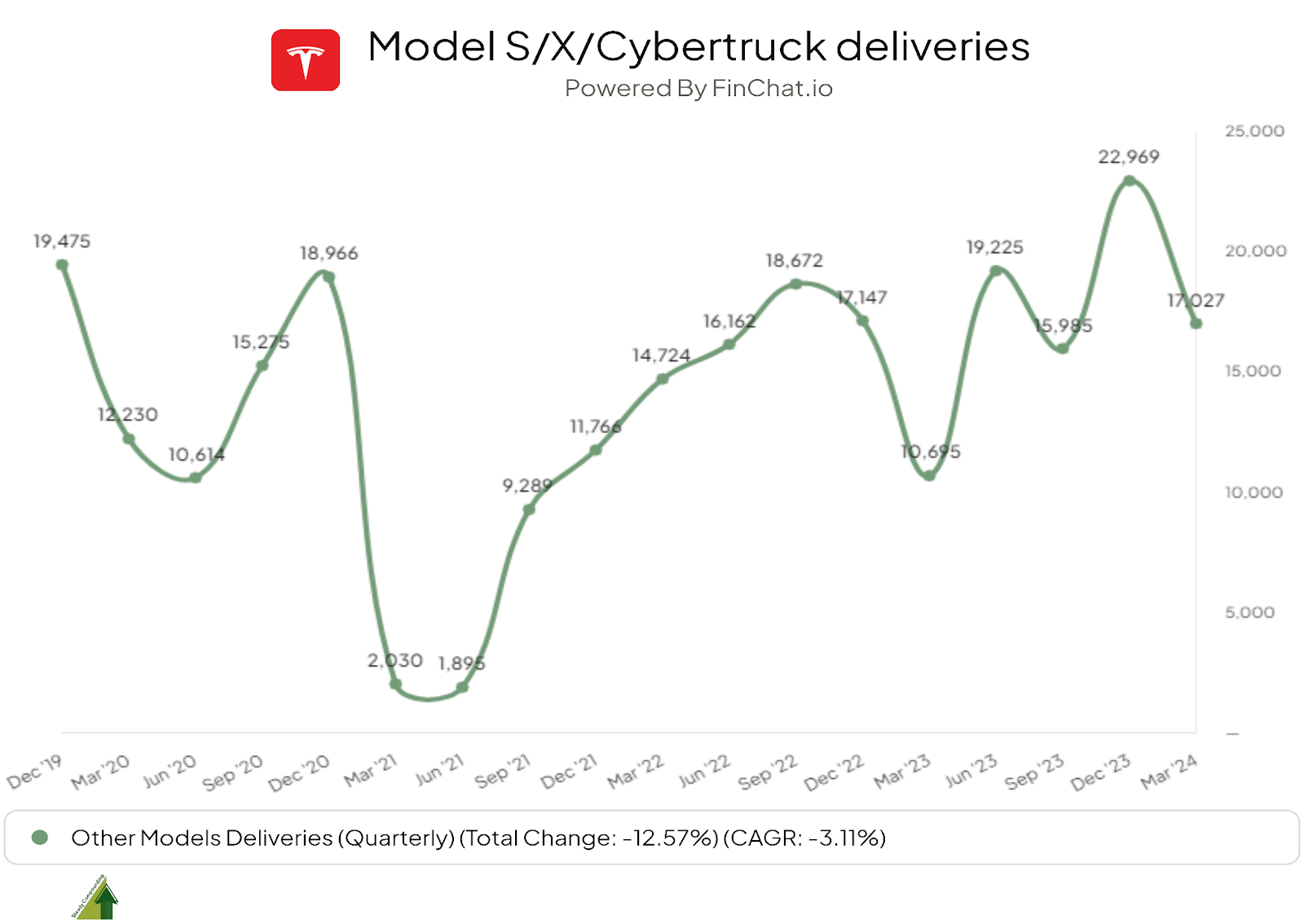

In contrast, Model S, X, and Cybertruck deliveries have risen by 59% over the past year, suggesting promising developments for the Cybertruck. This growth is notable even though it is still in its infancy and not yet a major revenue driver.

In order to determine whether Tesla is facing a temporary setback or a secular decline, let’s examine two critical questions:

1. Is the Electric Vehicle (EV) Market Tailwind Dying Down?

Absolutely not. Next question.

Okay, perhaps I should add a little more color. According to Reuters, EV penetration in North America stands at just 12.5%—far lower than in China and Europe.

EVs are pivotal for reducing emissions from road transport, which accounts for over 15% of global energy-related emissions. A number of factors will continue to propel EV adoption forward, including environmental awareness, government incentives, battery technology advancements, and electric vehicle charging infrastructure expansion.

2. Is Tesla Losing Ground to Competitors?

The EV space has indeed become more competitive. Initially, traditional automotive giants like Ford and General Motors were hesitant to enter the fray. Now, it’s universally acknowledged that a shift to EVs is imperative.

EVs are much less profitable than the big pickups and SUVs that dominate the two companies’ business, which poses a challenge to these traditional players because they are so much smaller compared to Tesla, which, even after recent price cuts, maintains an enviable profitability margin.

The more significant competition for Tesla comes from Chinese automakers. Elon Musk himself has stated, “…our observation is generally that the Chinese car companies are the most competitive car companies in the world. So I think they will have significant success outside of China, depending on what kind of tariffs or trade barriers are established. Frankly, I think if there are no trade barriers established, they will pretty much demolish most other car companies in the world. So they’re extremely good.”

In my opinion, the market is large enough to support multiple players, much like when the iPhone first came out, it was revolutionary, and competition entered, but it didn’t stop Apple from creating and capturing value.

In all likelihood, Tesla’s recent struggles are a temporary setback and not a permanent decline. As a result of economic pressures, consumer spending habits have tightened.

Considering this isn’t a permanent decline, and given that it’s cyclical in nature, why don’t I sell now and buy back later?

Market resurgences are notoriously difficult to time, as financial markets are forward-looking and recoveries often occur rapidly.

Instead of looking at short-term fluctuations, I’d rather keep my eye on the long-term picture.

Recent Developments and Strategic Moves at Tesla:

1) Price adjustments: Tesla recently modestly increased the price of Model Y

2) Further global expansion: Tesla’s factory in Berlin has begun manufacturing vehicles for export to India, marking a significant expansion into new markets. Furthermore, Elon Musk’s anticipated meeting with Prime Minister Modi this month could bring the opening of a new factory in India.

3) Robotaxi: Elon Musk has announced that the Tesla Robotaxi will be unveiled on August 8th.

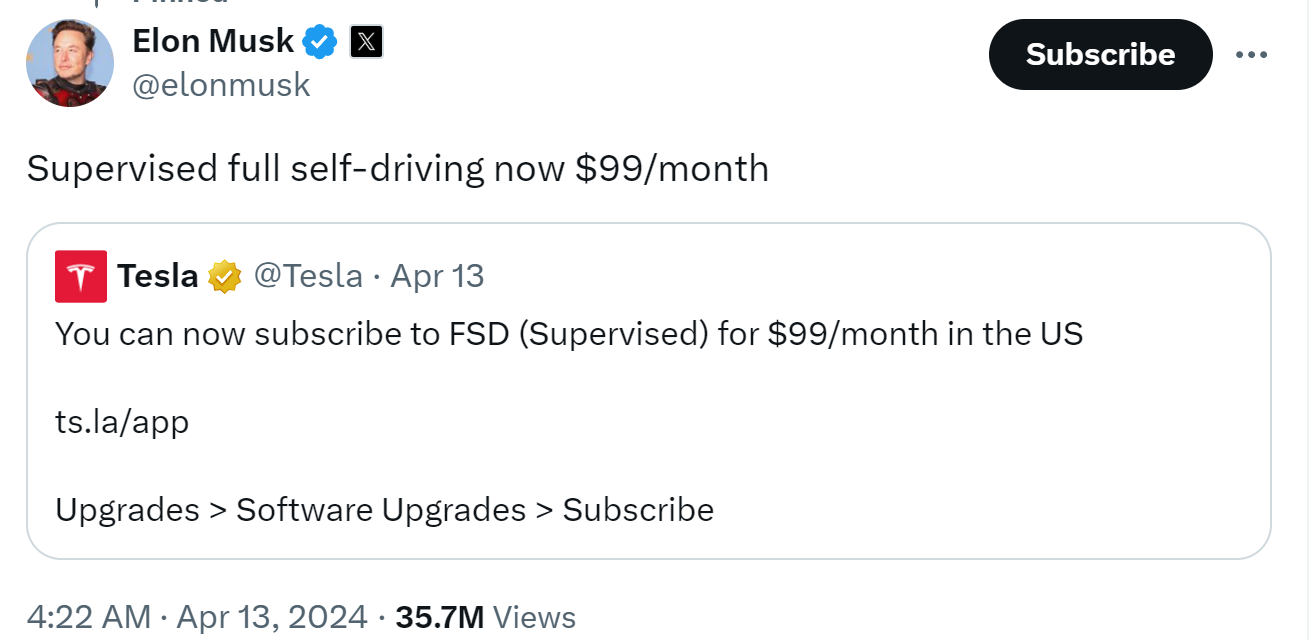

4) Advancements in Full-Self Driving (FSD) technology: There has been significant positive feedback on the advancements from FSD version 11 to 12.3. The transition to a video-based neural network marks a substantial improvement, which is expected to accelerate the rate of development in this area. To promote FSD 12.3, Tesla has introduced incentives such as a one-month free trial and reduced the subscription fee from $200 to $99 per month.

Elon even sent out an email to employees with this message:

“Going forward, it is mandatory in North America to install and activate FSD V12.3.1 and take customers on a short test ride before handing over the car. Almost no one actually realizes how well (supervised) FSD actually works. I know this will slow down the delivery process, but it is nonetheless a hard requirement.

Thanks,

Elon”

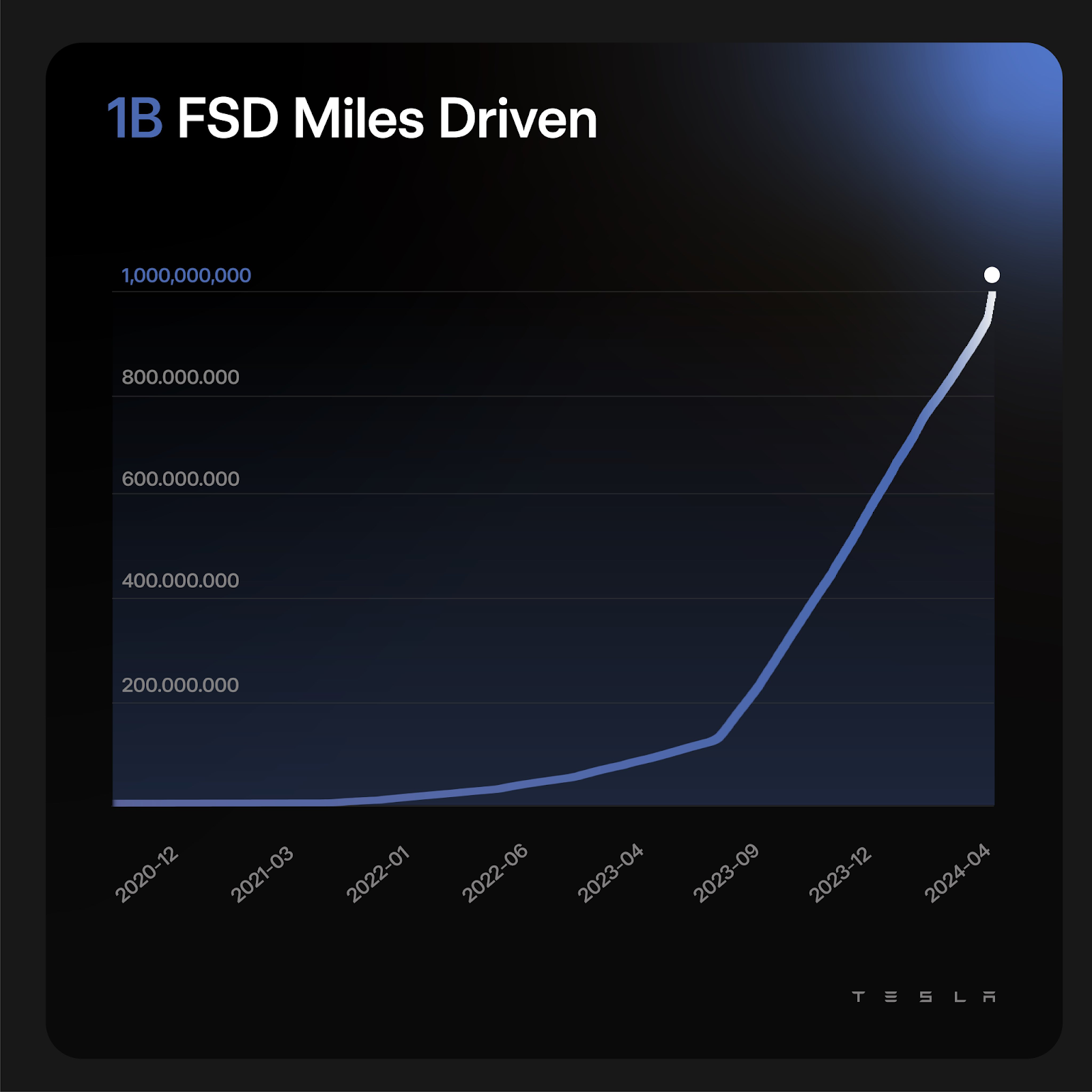

With over 1 billion miles driven on FSD, Tesla has accumulated a valuable dataset to further enhance its autonomous driving abilities-a distinct competitive advantage.

The key risk for Tesla

I’m not worried about the recent decline in deliveries, the company has plenty of growth engines and long-term catalysts. But the thing that keeps me up at night for Tesla is the key man risk. As I’ve highlighted in my Tesla deep-dive, the biggest risk and asset to the company is the eccentric genius—Elon Musk:

“Elon Musk is an engineer at heart and he’s the heart and soul behind Tesla’s brilliance. Much like Steve Jobs was to Apple. After the passing of Steve, innovation with the iPhone typically consists of more cameras and the iPad failed to sustain its place in most people’s tech inventories.”

Conclusion

Despite Tesla’s challenges, they seem temporary. Tesla continues to advance its technological capabilities and expand its market presence despite the widespread negative media narratives and social media chatter. New innovations and expansion into new markets like India demonstrate the company’s continued growth and resilience.

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in Tesla at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).

P.S. If you want access my entire stocks research archive, check out the Steady Compounding Insider Stocks below.