In my report to Steady Compounding Insider Stocks members on March 21, I highlighted that Sea Limited’s finances were beginning to improve. The company generated a cumulative US$1.2 billion in free cash flow (FCF) for the financial year 2023 and ended the year with US$6.7 billion in cash on their balance sheet. However, they weren’t quite out of the woods yet, primarily due to Garena’s lukewarm performance:

“While Garena’s Digital Entertainment segment had an increase in bookings sequentially of 1.8% to US$456 million, we saw its active users decline sequentially by 2.8% to 529 million and its paying users decline sequentially by 2% to 40 million…As Free Fire remains Garena’s primary revenue driver, it appears they don’t possess the magic formula to recreate the success of this one hit. In the latest quarter, this segment generated only US$217 million in adjusted EBITDA, continuing its downward trend since Q2 2021, when it generated US$741 million.”

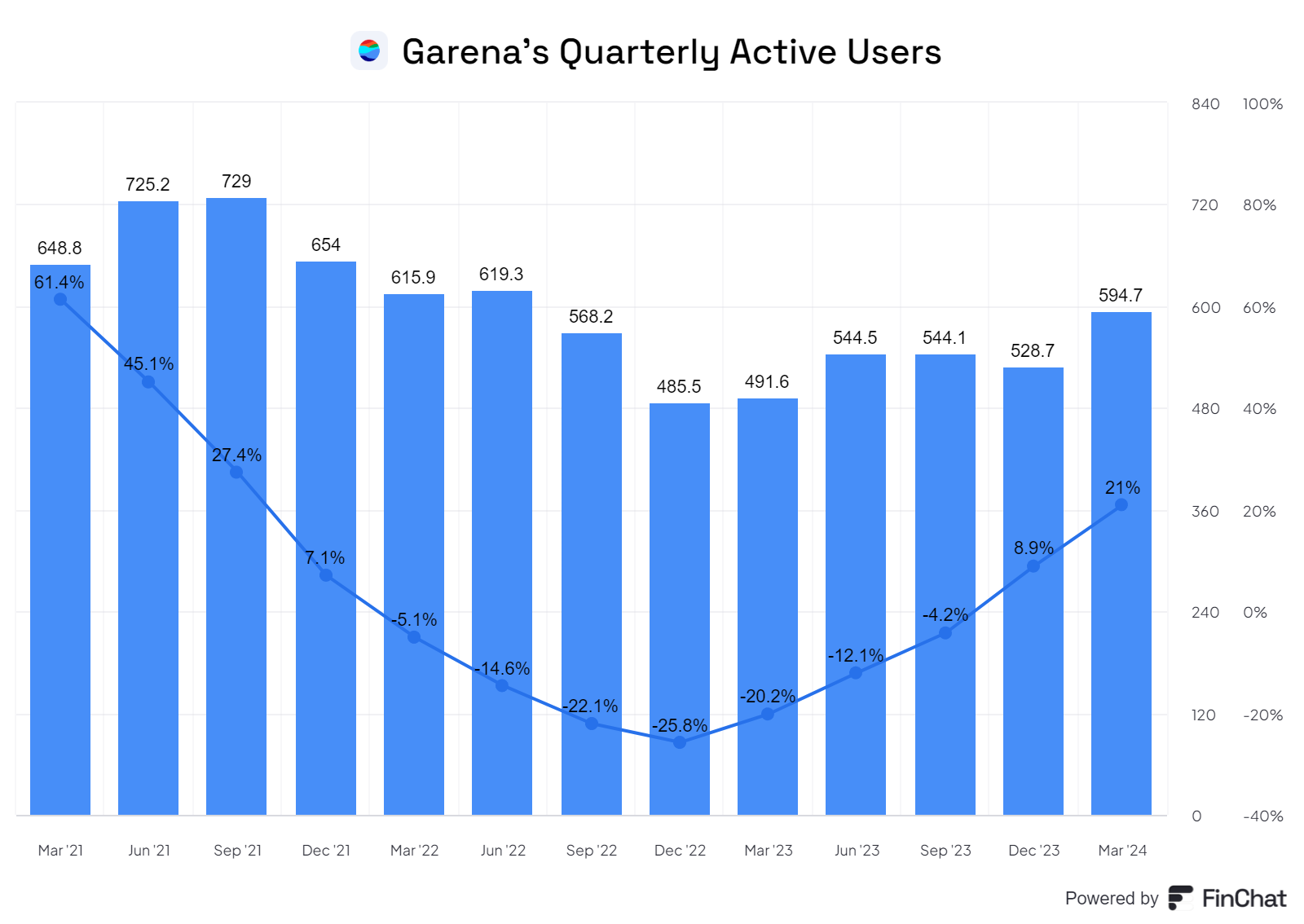

However, signs of recovery are emerging on the Garena front. Garena saw double-digit growth in Quarterly Active Users, from 492 million to 595 million, representing a 21% year-on-year increase.

Source: Finchat (get a 15% discount using this link)

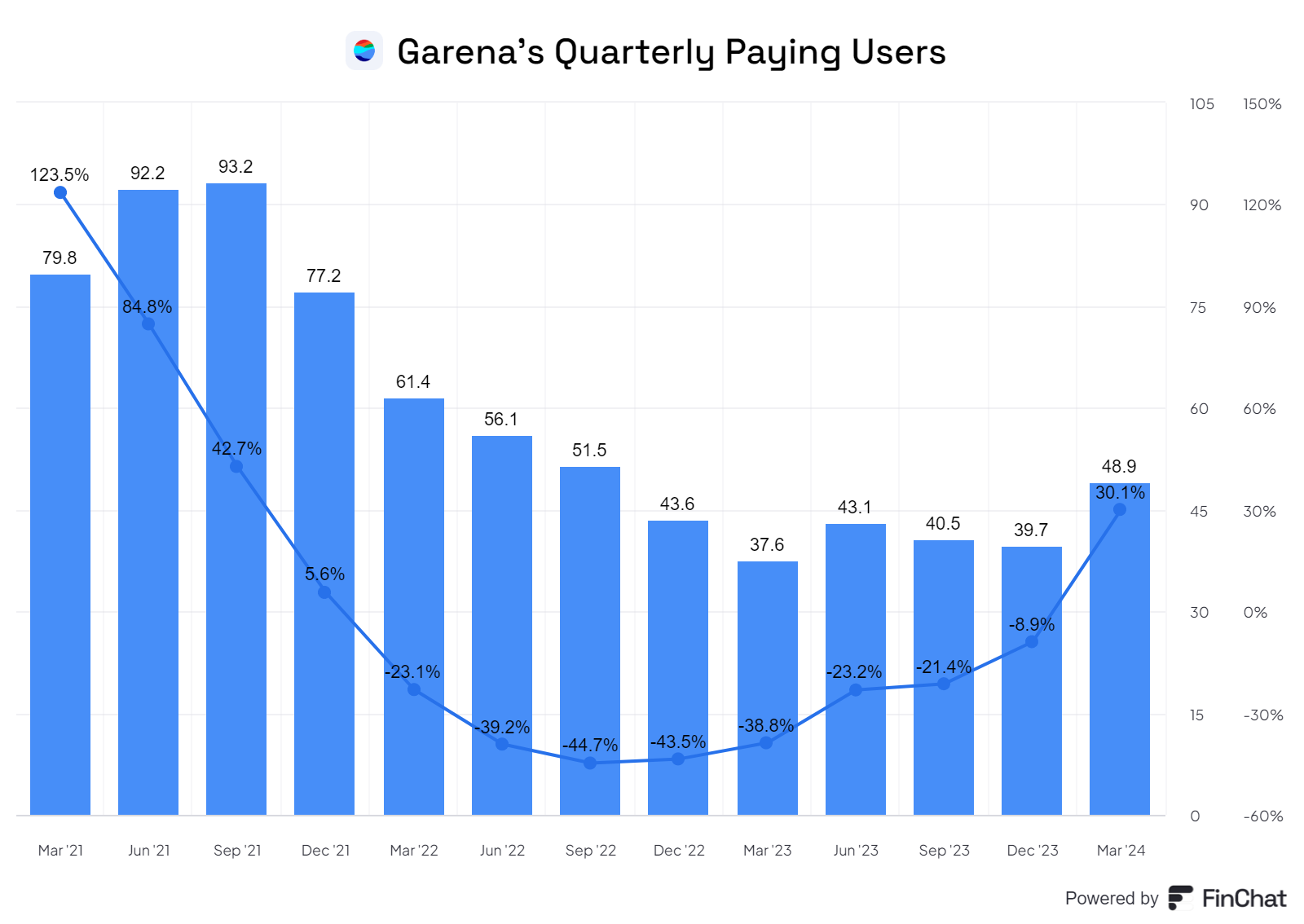

Even better, Quarterly Paying Users rose by 30.1%, from 38 million to 49 million. Impressively, the company achieved this growth while reducing its sales & marketing (S&M) spending, which fell to $19.4 million this quarter from US$23.4 million a year ago.

Source: Finchat (get a 15% discount using this link)

Achieving higher active users and even higher paying users while spending less on S&M is a clear win. The key now is whether Sea Limited can sustain this efficient growth over the longer term.

The driving force behind this solid performance is still Free Fire. As explained by Forrest Li, CEO, “According to Sensor Tower, Free Fire was the most downloaded mobile game globally in the first quarter. Given this track record of being able to sustain and grow Free Fire’s massive global user base, we are confident of building Free Fire into an evergreen franchise.”

Li further noted that post-COVID, there was a churn as gamers started to explore other forms of entertainment once lockdown measures eased. However, the company is now seeing many of these gamers return. “During the COVID time a gamer used to play a lot as there’s not many options for entertainment, and they felt burned out. That’s why after COVID, gamers started to look for other entertainment. But after another 2 years, we see that trend starting to come back and the gamers are rejoining Free Fire.”

If this trend persists and more gamers return to Free Fire, it would bode well for Sea Limited, as Garena has historically provided significant FCF for the company’s ambitions. Adjusted EBITDA for its digital entertainment segment rose 22.4% year-on-year to reach US$715 million, providing a substantial cash boost for Sea Limited.

The company expects Free Fire to achieve double-digit growth in 2024, but this does not include the potential for Free Fire to return to India. They are currently working with authorities to get the game back in. “For the Free Fire relaunch in India, at this moment, we are actively working with the stakeholders—regulators and potential local partners—to figure out what is the best plan to relaunch Free Fire in India. If that is successful, I think that will be a meaningful potential upside in terms of the users and the bookings considering India is a very big market. And just to clarify, at this moment for our outlook for the rest of the year in terms of the double-digit growth… this does not take into consideration the relaunch of Free Fire in India.”

Over the next few quarters, we will have to monitor if the trend of gamers returning to Free Fire persists. If they manage to re-enter the Indian market, this will be a cherry on the cake for Sea Limited.

Shopee

For Shopee, gross merchandise value (GMV) grew 36.3% year-on-year to US$23.6 billion, with more than 2.6 billion orders placed on the platform, up 57% from a year ago.

Revenue grew 33% year-on-year to reach US$2.7 billion, with the take-rate remaining stable at 11.6%. Marketplace revenue, which includes the advertising and commissions that Shopee charges, rose in tandem, increasing by 33% to US$2.4 billion.

The company noted that there’s limited room for further growth via take-rate increases, but there is still plenty of potential to increase advertising revenue. Hou Tianyu, CFO, explains, “We still see there is meaningful room to increase the commission take rate, although probably not as aggressive as last year in terms of increase. We also see there’s a meaningful room on the ad take rate that we can look at… we believe that our ad take rate is still slightly lower than the peers that we see in other markets, so there is some meaningful room there.”

Shopee scaled back on its sales and marketing (S&M) expenses sequentially, spending US$676 million, or 24.6% of Shopee’s revenue. This is significantly lower than during the COVID lockdown period when they were spending upwards of 50% of Shopee’s revenue on S&M expenses.

Regarding S&M, management expects to continue scaling back. “In the coming quarter, I believe that we’ll continue to optimize our sales and marketing spending. And we do believe that the general trend will come down.”

Shopee has returned to near breakeven at -US$21.7 million, which aligns with management’s promise to investors in Q4 2023 that adjusted EBITDA for its e-commerce segment would turn positive in the second half of 2024.

Focusing on Shopee’s operations in Brazil, it is also approaching breakeven, with its loss per order narrowing to -US$0.04, significantly down from -US$0.34 a year ago.

Shopee Asia is cash flow positive, with adjusted EBITDA coming in at US$11.5 million, while its other markets (i.e., Brazil) reported a deficit of -US$33.2 million.

I’m encouraged to see that the company is making significant strides in developing its logistics capabilities, though there is still considerable room for improvement compared to e-commerce giants in the US and China. During the earnings call, Forrest Li highlighted the importance of this effort: “Our integrated logistics capability has become a key differentiating factor of our service quality. We have put a lot of hard work into SPX Express, and today, it is one of the fastest and most extensive logistics operators in our market, greatly enhancing our customer experience.”

Li further noted that about 70% of SPX Express orders in Asia were delivered within three days and emphasized that logistical costs are decreasing: “Because of the scale we have achieved in our market, we have managed to steadily reduce costs. SPX Express’ cost per order decreased by 15% for Asia and 23% for Brazil year on year in the first quarter.”

Tony Hou, CFO, added that more than 50% of Shopee Asia’s orders are now handled by SPX Express. For Shopee Brazil, over 70% of orders are managed by Shopee Express. Both segments are expected to increase their share over time.

SeaMoney

SeaMoney continues to deliver strong growth, with revenue rising 21% year-on-year to US$499 million. However, it’s frustrating that management still refrains from providing key metrics such as total payment volume and the number of users.

Despite ramping up S&M expenses to US$57 million, adjusted EBITDA margin for its digital financial service segment remains robust at 29.8%, translating to US$149 million, a 50.4% year-on-year growth.

In justifying their S&M expenditure, Tony Hou, CFO, explains, “I think our businesses have a fairly good margin, as you can see from the EBITDA. At the same time, our business is still in a very early stage… So we see a huge potential there to grow over time… there is an intention to acquire more users to our digital financial service ecosystem, given the very big unit economics we have seen so far.”

This segment is in its sweet spot, delivering both profitability and rapid growth simultaneously. What’s less appreciated is how their established e-commerce presence with Shopee in the region significantly lowers the cost of customer acquisition for SeaMoney, enabling it to grow profitably. Forrest Li elaborates, “our credit business benefits from Shopee’s transaction volume and the user base.”

Conclusion

Things are finally looking back on track for Sea Limited post-COVID across all three segments—digital entertainment, e-commerce, and digital financial services. The company faced a sharp decline in users for Free Fire and a rising cost of capital, setting it on a path to aggressively cut down costs. Now, the company has a much healthier balance sheet and is growing again on a leaner cost structure. This is the first quarter where we’re seeing green shoots from Garena, though it remains a one-game wonder. We’ll need to monitor if users are truly returning to Free Fire and if it becomes the evergreen game that Forrest Li claims it to be. For now, I’ve become more comfortable holding on to my Sea Limited shares.

P.S. Steady Compounding Insider Stocks members, you can go through the past archives of member-exclusive Sea Limited reports here.

Not a member yet? Click here to join Steady Compounding Insider Stocks and gain access to all my stock research: https://steadycompounding.com/membership/

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in Sea Limited at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).