In my April 2022 report titled “Netflix: The Streaming Giant,” I wrote:

“While new subscriber acquisitions seem to have slowed down, given the large and growing addressable market, coupled with the massive entertainment value they bring for a low price point, Mr. Market seems to have overreacted to the near term outlook for subscriber growth.“

Right after I published, Netflix released Q1 2022 earnings.

The stock nosedived 25.8% after hours—from $340 to $252. Then it kept falling to $180.

The outlook was…

Bleak. Bleak. Bleak.

Today?

The pendulum has swung completely. Netflix recently breached $1,300 per share. The stock now wears a golden halo—the kind usually reserved for defensive stalwarts like Costco.

The New Defensive Stock

Investors believe Netflix will thrive regardless.

Trade war? Recession? AI disruption?

Doesn’t matter.

Netflix is being regarded as a defensive stock now. After all, as much as people complain about prices going up for their Netflix subscription, at $24.99 monthly for premium or $7.99 with ads, Netflix represents a tiny fraction of household expenses.

Yet it delivers outsized entertainment value.

Measure it by dollar cost per entertainment hour—it’s tough to find a rival. Even if people tighten their belts on frivolous expenses, they’re more likely to cut other expenses before Netflix.

Netflix Co-CEO Gregory Peters reinforces this:

“We also take some comfort in the fact that entertainment historically has been pretty resilient in tougher economic times. Netflix specifically also has been generally quite resilient, and we haven’t seen any major impacts during those tougher times…And we think that we represent an incredible entertainment value, starting at $7.99 in the U.S. and Canada with the ads plan. It’s an accessible price point.”

With this belief, Netflix is currently trading at a last twelve months PE multiple of 60x, and a forward PE multiple of 48x.

So what warrants the streaming giant trading at this multiple?

Q1 2025: Triple Beat

Let’s examine the Q1 2025 results.

They had a triple beat on estimates:

- Revenue grew 13% year-on-year to $10.5 billion

- Operating income rose 27% to $3.3 billion with margins expanding 360 basis points to 31.7%

- EPS jumped 25% to $6.61

Cash generation? Exceptional.

Free cash flow surged 26% year-on-year to $2.8 billion, predominantly driven by rising operating cash flow.

Looking ahead, management guided for revenue growth to reaccelerate. They expect 15.4% year-on-year growth to $11 billion in Q2—alongside operating margins climbing to an eye-watering 33.3%.

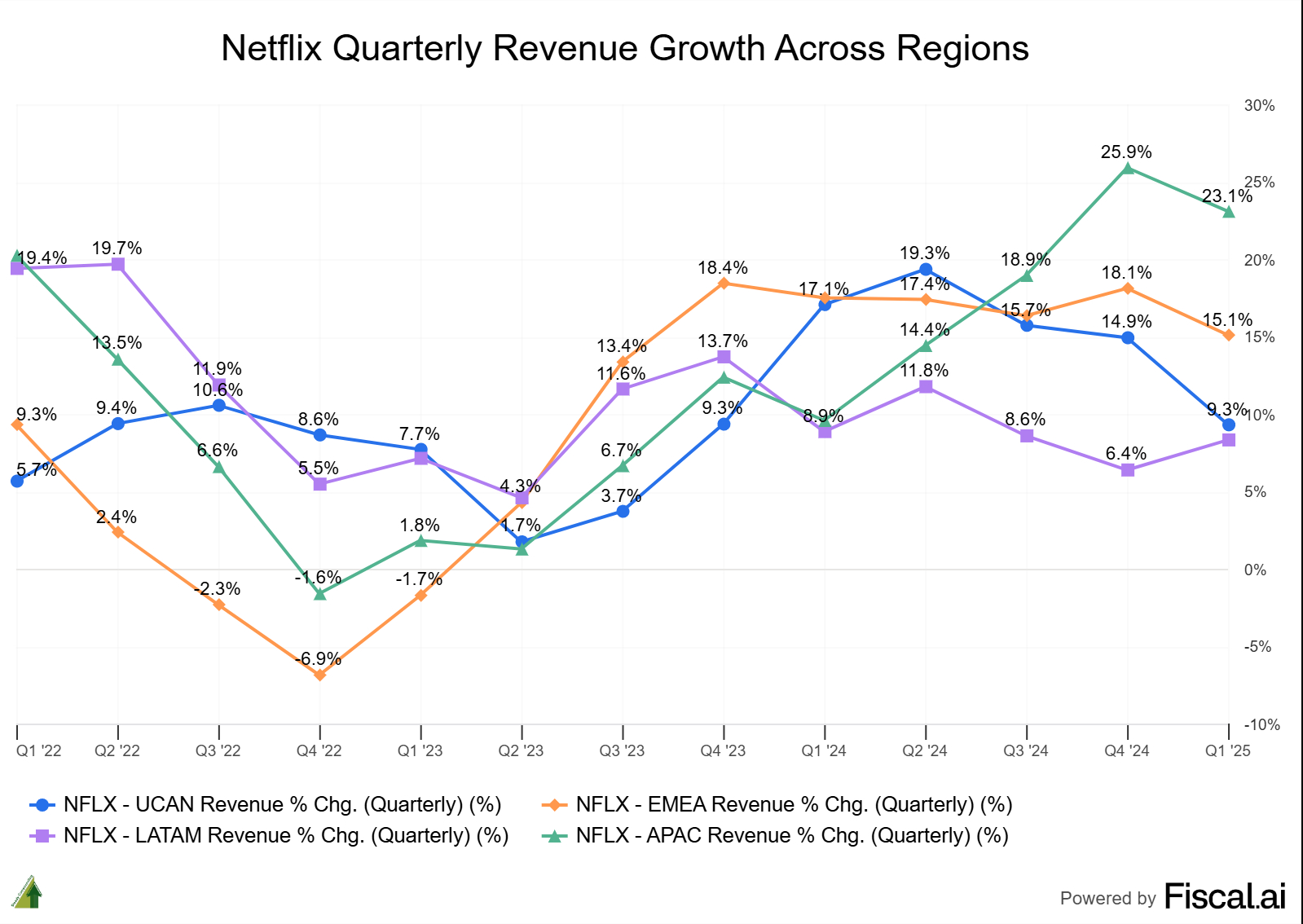

Regional Performance: The UCAN Dominance

While Netflix frustratingly no longer breaks down subscriber numbers, their regional revenue tells a compelling story.

U.S. growth decelerated slightly to 9% year-on-year—but don’t read too much into this. The slowdown reflects only a partial quarter impact from price changes, plan mix shifts, and the absence of those lucrative Christmas Day NFL game ads.

Management expects UCAN revenue growth to reaccelerate in Q2.

Source: Fiscal AI (get a 15% discount using this link)

What about international markets?

EMEA, LATAM, and APAC are all firing on all cylinders. LATAM appears to be growing single digits, but that’s an FX illusion. Strip out currency headwinds, and growth has consistently exceeded 27% each quarter.

Despite strong international performance, UCAN still contributes overwhelmingly to overall revenue. Netflix has grown its most mature market through a combination of price increases and the introduction of the more affordable ad-tier to increase overall subscriber count.

The AI Wildcard

There’s considerable speculation about how AI will impact Netflix.

Jim Cameron, whose notable work spans from Titanic to Avatar, famously said AI could make it 50% cheaper to make movies. Theodore Sarandos, Co-CEO of Netflix, thinks it can make movies 10% better.

Who’s right?

Both could be.

Netflix stands to benefit either way. Lower costs mean higher margins. Better content means happier subscribers.

The Leaked $1 Trillion Club Memo

In April 2025, The Wall Street Journal reported on a leaked internal Netflix business review that sent investors into a frenzy.

The leak revealed Netflix’s 2030 ambitions:

- Revenue Goals: Double revenue from $39 billion in 2024 to approximately $80 billion by 2030

- Operating Income: Triple from $10 billion in 2024 to $30 billion by 2030

- Advertising Revenue: Target $9 billion in global ad revenue by 2030

- Market Cap: Ambition to reach $1 trillion

- Subscriber Growth: From 301.6 million to 410 million

The memo specifically highlighted expansion opportunities in high-broadband markets like Brazil and India.

Investors got excited.

Too excited.

Co-CEO Ted Sarandos rushed to clarify: these were “long-term aspirations,” not guidance.

What This Means for Subscribers

These figures give us fascinating insights into Netflix’s future—for both investors and subscribers.

For subscribers:

As of Q4 2024, revenue came in at $10.2 billion with 301.6 million subscribers. This means revenue per subscriber is roughly $34 per quarter, or $11.32 per month.

With the revenue goal of $80 billion and 410 million subscribers in 2030, revenue per subscriber would be roughly $195 annually, or $16.26 per month.

From $11.32 to $16.26 per month—that’s roughly 6.22% annualized growth.

What if we strip out the ad revenue?

With $9 billion in ad revenue goals for 2030, subscription-only revenue per subscriber would be $173 annually, or $14.43 per month. That’s 4.13% annualized for subscription revenue.

If you’re a Netflix subscriber, you can roughly expect price increases of 4% annually.

The Advertising Growth Story

While Netflix doesn’t report advertising revenue because it’s still small, eMarketer estimated the streaming giant brought in roughly $2.15 billion in ad revenue for 2024.

With a goal to hit $9 billion in ad revenue, this represents annualized growth of roughly 27%.

Strip the estimated ad revenue from today’s numbers, and Netflix’s subscription-only revenue for 2024 would be $37 billion. Strip ad revenue from the 2030 goal, and subscription revenue alone would be $71 billion.

From $37 billion to $71 billion in subscription revenue alone—that’s an annualized growth rate of 11.5%, coming from a combination of subscriber growth and price increases.

Valuation: The $1 Trillion Question

Now, let’s examine Netflix’s $1 trillion market cap goal.

With revenue of $80 billion and operating income of $30 billion, operating margins would reach 38.5%.

Netflix has paid an effective corporate tax rate between 12-13% over the past five years. Assuming a 12.5% tax rate with minimal interest payments, net income margins would be roughly 33.7%, or $26.3 billion.

That’s a trailing PE multiple of roughly 38x.

Like its revenue and operating margin goals, this is on the ambitious end.

Where are we today?

Netflix with a market cap of $552 billion reaching $1 trillion by 2030 represents annualized growth of 11.4%.

I see this as a very rosy scenario—if the company executes on all its ambitious goals.

The expected returns of 11.4% under this scenario?

Not something to be excited about.

Conclusion

Netflix has obviously executed extremely well, and the market’s valuation reflects just that.

Valuations today are steep, even under rosy assumptions.

I look forward to seeing when they’ll start reporting their advertisement numbers.

Compound steadily,

Thomas

P.S. If you’re curious about my thoughts when Netflix crashed in 2022, check out these reports where I argued the selloff was overdone:

- 13 April 2022: Netflix: The Streaming Giant

- 20 April 2022: Netflix Down After Hours

- 12 August 2022: Disney Overtook Netflix

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in The Netflix at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).