Part 1 of 3: The Origin Story (1999–2007)

The Pitch

In the spring of 1999, Marcos Galperin was a second-year MBA student at Stanford when John Muse, the billionaire co-founder of Hicks, Muse, Tate & Furst (now HM Capital Partners), came to campus to give a lecture.

Galperin had learned his lesson about recognizing opportunity. Earlier that year, he sat next to Warren Buffett for ten minutes without realizing who he was. He would not make the same mistake twice.

After the lecture, Galperin secured the chance to give Muse a lift to his plane. With a captive audience, he pitched his idea for a Latin American online marketplace. When Muse seemed interested, Galperin missed the exit on purpose, stretching the drive by twenty minutes.

By the time they reached the airstrip, Muse had heard enough. He dropped his suitcase and told Galperin he wanted to invest.

That conversation led to MercadoLibre’s seed round: $7.6 million from Muse’s firm, JP Morgan Partners, Flatiron Fund, and Goldman Sachs. It closed in October 1999.

Within six years, MercadoLibre would be the only significant survivor of Latin America’s dot-com massacre, outlasting more than eighty competitors who had raised, in aggregate, far more capital. This is the story of how they did it.

The Founding

MercadoLibre launched in August 1999 from a garage in Buenos Aires. Galperin had returned from Stanford with two co-founders: Hernán Kazah, who would serve as CFO and later COO, and Stelleo Tolda, who took charge of the Brazilian operation.

The CTO was Galperin’s cousin, Marcelo, who made a decision that would prove critical: rather than buying software off the shelf, he would build the technology platform from scratch.

The business model was straightforward: a regional clone of eBay, the American auction marketplace that had gone public in 1998 and become one of the hottest stocks of the dot-com boom. Latin America, with its 500 million consumers and nascent internet adoption, seemed ripe for a similar platform.

The founders considered three models: Yahoo’s portal play, Amazon’s inventory-heavy retail operation, and eBay’s asset-light marketplace. They chose eBay.

The decision to avoid holding inventory would prove prescient when capital markets collapsed when the dot-com bubble burst.

What set the founders apart was their mental model. At Stanford, Kazah had been exposed to thinkers who, as he later recalled, “disrespected the linear process and encouraged exponential thinking.” Rather than launching in Argentina and expanding country by country, MercadoLibre went regional within the first year, operating across multiple Latin American markets simultaneously.

It was designed for scale before it had any.

Within three months, the platform attracted 15,000 users and processed $2 million in cumulative transactions. The early signs were promising. But so were the signs for dozens of competitors chasing the same opportunity.

The Competition

In the late 1990s, roughly eighty e-commerce startups launched across Latin America, most pursuing business models similar to MercadoLibre’s. The most formidable was DeRemate, founded by Alec Oxenford just weeks after MercadoLibre’s launch.

DeRemate took the opposite approach. It had eleven co-founders, licensed off-the-shelf auction software, and bought its initial user base by acquiring a competitor called E-Bazar. The playbook was blitzscale: move fast, raise capital, buy market share.

It worked, at first. DeRemate raised a $12 million Series A from Citigroup, then a $45 million Series B led by Terra Networks. Eight months after founding, it was valued at $150 million.

It was growing faster than MercadoLibre and spending aggressively on brand awareness.

The marketing war was lopsided. DeRemate bought billboards at soccer matches and ran ads on open television. MercadoLibre, more conservative with its seed funding, could not match the spend. In terms of top-of-mind awareness, DeRemate was winning.

But Kazah saw the situation differently. Only two or three percent of Latin Americans had internet access. Spending millions to reach the other ninety-seven percent was, as he put it, “shooting with a bazooka to kill a fly.”

Still, by early 2000, MercadoLibre was burning through its seed capital faster than planned. The team had grown to 200 employees, too many for a company with zero revenue. They needed to raise again.

The Crash

In March 2000, the NASDAQ began its collapse. MercadoLibre was in the middle of fundraising.

Kazah, who spoke about this period in a 2025 interview on the Product Market Fit Show (LINK), remembers it vividly. The company had drawn interest from multiple investors, but as the market cratered, they withdrew one by one. Every day brought another phone call: “Hey, remember when I said I was interested? I’m no longer interested.”

By the time the last investor pulled out, MercadoLibre had a negative runway. They had already spent more than the $7.6 million they raised, funding the gap with debt. The company was technically insolvent.

Kazah recalls thinking they would not survive.

Then, improbably, they caught a break. Susan Seeger, who led Chase Capital Partners’ Latin America practice and sat on MercadoLibre’s board, pressured Goldman Sachs to honor an earlier term sheet. In May 2000, just as the technology sector was entering freefall, MercadoLibre closed a $46.5 million round.

“It’s one of those games that if you play it ten times, you lose nine. But we won.”

Hernán Kazah, co-founder of MercadoLibre

What happened next defined the company’s culture for the next two decades.

Rather than celebrating the fundraise and accelerating spend (as most of their competitors did), the founders treated the near-death experience as a warning. Capital markets in Latin America would remain frozen for nearly a decade. They had one chance to get it right.

The team implemented what one early employee called “nuclear winter” planning. They cut the workforce from 200 to 100. They slashed marketing by ninety percent. They shut down regional offices and pulled everyone back to Buenos Aires.

The goal was no longer growth. It was survival.

“The fear of running out of money was so deep, so harsh, so painful, that it basically outweighed any fear of competitors.”

Hernán Kazah, co-founder of MercadoLibre

Their competitors, meanwhile, made marginal adjustments. They had also raised capital before the crash, and most had money in the bank. But because they had not experienced the same existential terror, had not stared at the spreadsheet showing negative runway, they continued spending.

Some cut staff from 200 to 150. Some reduced marketing by twenty percent instead of ninety. They made marginal adjustments. They all ended up dead.

DeRemate, the most aggressive, ran out of money and sold to MercadoLibre in 2005 for a fraction of its peak valuation. Dozens of others simply disappeared.

The Rebuild

With survival secured, MercadoLibre began building the foundation for everything that followed. Two strategic moves during this period gave the company advantages that would compound for years: the eBay partnership and the Google arbitrage.

The eBay Partnership

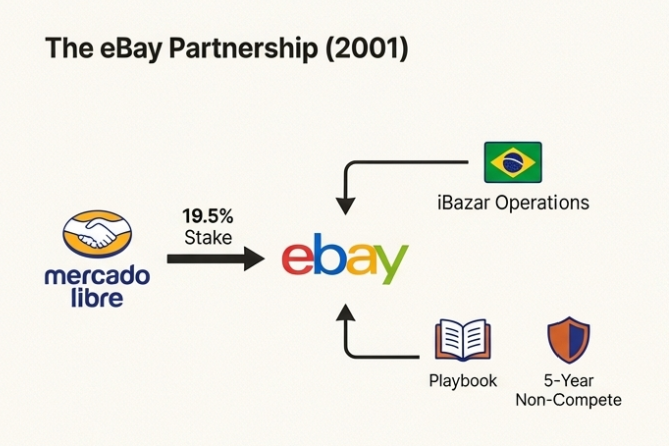

In September 2001, eBay approached MercadoLibre with an unusual offer. The American company had acquired iBazar, a marketplace operating in Brazil, and wanted to exit the region. Rather than taking cash, eBay proposed a stock swap: MercadoLibre would get iBazar’s Brazilian operations, and eBay would receive a 19.5% stake in MercadoLibre.

The deal came with two critical provisions. First, eBay agreed to share best practices, giving MercadoLibre access to the playbook of the world’s leading online marketplace. Second, eBay committed to staying out of Latin America for five years, eliminating the threat of direct competition from a company with vastly superior resources.

But the partnership taught MercadoLibre more than best practices. It taught them what not to do.

Kazah later described witnessing a “Lake Como moment,” when eBay’s leadership lost the hunger that had made it great. The company that had pioneered online marketplaces grew comfortable, and Amazon, still primarily a bookseller, overtook it.

As Pedro Arnt, who served as MercadoLibre’s CFO (now CEO of dLocal) for over a decade, observed on the climbers & scalers podcast: “Amazon should never have happened the way it did, if eBay had done things right.”

The lesson crystallized into what MercadoLibre calls a ‘perpetual beta’ culture”: the belief that no market position is safe and no product is ever finished. eBay would hold its MercadoLibre stake until 2016, but the cultural imprint of its failure remained long after.

The Google Arbitrage

While competitors spent on television and billboards, MercadoLibre found a different channel.

Google was just beginning to expand internationally, and its Latin American advertising inventory was essentially unsold. Kazah flew to Mountain View and made a proposition:

“We became the first and only customer of Google in Latin America for a year because they didn’t pay attention to Latin America. We went to Mountain View and told them, ‘Hey guys, we want to buy all your traffic in Latin America.'”

Hernán Kazah, co-founder of MercadoLibre

They bought all of it.

While competitors targeted the general population through mass media (the ninety-seven percent without internet access), MercadoLibre targeted the three percent who were already online. The cost per acquisition was a fraction of what competitors paid for their billboard campaigns.

The company layered on additional organic growth engines: search engine optimization (which Kazah called “ancient strategy” but was cutting-edge at the time) and an affiliate program that paid website owners for referrals. Every channel was measured against a strict return threshold.

While the others were painting the car and putting stickers on the windshield, MercadoLibre was building the engine.

By the end of 2001, GMV had reached $21.3 million. Transactions never stopped growing. The company had found a formula that worked, and unlike its competitors, it could afford to keep executing.

From Marketplace to Payments

Mercado Pago, the payments platform that now processes over $200 billion annually, was in Galperin’s original Stanford business plan. But launching it required solving a problem that had defeated most Latin American commerce initiatives: nobody trusted strangers on the internet, and almost nobody had a credit card.

Cash and checks dominated Latin American commerce. Credit card penetration was minimal. The infrastructure that Americans took for granted (reliable payment processing, dispute resolution, fraud protection) did not exist.

Mercado Pago launched in Argentina in late 2003, expanding to Brazil and Mexico in early 2004. The early operation was almost comically manual.

Paula Arregui, who joined to build the payments business, later reflected on the climbers & scalers podcast (LINK):

“If we had fully understood the complexity of what we were attempting, we might never have started.”

Paula Arregui, Senior Vice President of Acquiring at Mercado Pago

Her team processed transactions by hand, entering credit card numbers into spreadsheets, faxing information between parties, and creating physical coupons for buyers who wanted to pay in cash.

The first solution was an escrow service built on a network of collection agents: buyers would pay a local agent, who logged the receipt; the seller would then ship the goods; and upon confirmation, the seller would receive payment at a pickup point on their end.

It was primitive. It was also revolutionary.

The real problem wasn’t moving money. It was trust. Mercado Pago solved this by holding funds in escrow until buyers confirmed delivery, turning Latin America’s biggest e-commerce barrier into a moat. By holding funds until buyers confirmed satisfaction and building reputation systems for both parties, MercadoLibre transformed the biggest barrier to e-commerce adoption into a competitive moat.

This was what Arregui later called the ‘inconscience advantage’ on the climbers & scalers podcast. Exhaustive feasibility studies might have killed the project. Instead, the team built something that worked, learned from its failures, and iterated. From manual spreadsheets to neural network fraud detection, Mercado Pago evolved into the backbone of Latin American digital payments.

But only because someone was naive enough to start.

By 2006, Mercado Pago processed 8.3% of MercadoLibre’s GMV, approximately $89 million in total payment volume. It represented 14% of the company’s revenue. The foundation for a fintech empire had been laid.

Product-Market Fit

For years, MercadoLibre charged nothing for listings or transactions. The marketplace was free, a necessary condition for building liquidity in a region where consumers were skeptical of online commerce and had limited ability to pay.

The question was whether anyone would pay when they started charging. When a free service starts charging even a cent, Kazah noted, most users say they are no longer interested.

The transition happened gradually. MercadoLibre introduced fees, watched carefully for churn, and adjusted. The marketplace continued to grow.

By late 2005, the company achieved something that had seemed impossible during the dark days of 2000: profitability.

Kazah remembers the exact moment he knew they had product-market fit:

“The moment you go to sleep at night with $1,000 in the bank and you wake up the following morning with $1,001 is: ‘Wow, this is working.'”

Hernán Kazah, co-founder of MercadoLibre

With profitability came optionality. The company still had a substantial portion of its $46.5 million war chest, capital that competitors had burned through years earlier. After acquiring DeRemate in 2005, other struggling competitors followed to be acquired by MercadoLibre.

By 2006, MercadoLibre had consolidated the market. Net revenues reached $52.1 million, up 85% from the prior year. GMV exceeded $1 billion. The company operated as the dominant e-commerce platform across twelve Latin American countries.

It was time to go public.

The IPO

MercadoLibre went public on August 9, 2007. That same morning, BNP Paribas halted redemptions on three funds exposed to U.S. subprime mortgages. It was the first domino of the global financial crisis.

The timing, once again, seemed catastrophic. But MercadoLibre had been forged in crisis. While investment banks scrambled to assess their subprime exposure, the company from Buenos Aires became the first Latin American technology company to list on NASDAQ.

The S-1 filing told the story of a company that had survived everything Latin American markets could throw at it: the dot-com crash, the Argentine economic crisis of 2001-2002, currency devaluations across the region, and the constant threat of competition from better-funded rivals.

It emerged as the dominant player not because it had more resources, but because it had more discipline.

The $46.5 million raised in May 2000 had funded seven years of operations, and the company still had a quarter of it left when it went public. That capital efficiency was not an accident. It was the scar tissue from nearly dying.

The Lesson

The near-death experience of 2000 shaped everything that followed.

It taught them that capital markets can close without warning, and that the companies making marginal adjustments will die while those making radical ones might survive. It taught them to focus on technology, unit economics, and organic growth rather than brand awareness.

As Kazah observed, the crisis “created the right culture in the company.” The fear of running out of money became institutional memory, a discipline that persisted long after the immediate threat had passed.

Most importantly, it taught them that survival was just the beginning.

Part 2 picks up where survival ends. Galperin moves his desk next to the CTO’s. A three-year platform rebuild tests the company’s nerve. And a 2018 crisis in Brazil forces the bet that would define the next decade.

>> Click here to subscribe for free to get it when it’s ready.

Great article, thanks Thomas!

Glad you enjoyed it!