Amazon is a different beast from when it first conceptualized in 1994, where Jeff Bezos had the idea of building an online bookstore with millions of titles. Bezos knew that the opportunity with ecommerce would be huge but he started with books because:

a) people wanted them,

b) physical stores were limited in what they could carry,

c) books were easy to pack,not fragile and

d) Amazon was located strategically near a major book distributor, so a warehouse inventory was not required to get started

In the early years, Bezos packed the books himself. With him and his small team (including his ex-wife) spending many back breaking nights packing books on the floor and rushing them out for shipment. This was when the norm for ecommerce delivery was anywhere between 2 weeks to 5 weeks!

With the current amount of data optimization for delivery, storage, and automation in Amazon’s warehouse, it makes it difficult to believe that back then the biggest productivity scheme was to pack books on tables rather than on the floor.

Amazon soon began selling music, DVDs/videos, toys, and everything else. Extending into toys presented a challenge because it was difficult to predict holiday season demand, unsold toys are not returnable to manufacturers, and it is extremely fad-driven. For a young company like Amazon, manufacturers were giving their best selection to giant retailers such as Toys “R” Us. Bezos would drive his Honda Accord to Toys “R” Us and max out his credit card to get his hands on the most popular selection for Amazon.

Amazon’s Early Days: 1P Marketplace

Notice that up till now, Amazon has been operating a 1P marketplace, where they will buy the inventory and sell directly to internet users. Contrast that to eBay who operates a 3P marketplace, where they do not take inventory, instead, they are merely a platform that earns a commission by bringing third party merchants and consumers together.

A 1P marketplace will have a much lower profitability profile. Since Amazon has to purchase the product before reselling to consumers, its cost of sales is much higher compared to eBay. eBay’s costs would typically only be payment processing, customer support and data server usage.

In the following chart, we can see that Amazon gross profit margins are significantly lower than eBay’s, at ~23% and ~79% respectively.

Also, cash will be locked up for working capital requirements under the 1P model, because Amazon has to spend cash first to hold inventory in the warehouse, before getting paid by customers later. eBay on the other hand, would receive cash from customers first for a sale, before having to pay third party merchants.

As a result, we can see that cash from operations as a percentage of revenue for eBay being significantly higher than Amazon.

Having a 1P marketplace is not a bad thing in itself. It provided Amazon with control over its customers’ experience and, because of its size, it gained unrivaled logistical prowess in the United States.

Today, Amazon (and Jeff Bezos) is a different beast. The profitability of the business has improved considerably. With the growth of its high margin segments such as (1) 3P marketplace, (2) advertisement, (3) AWS and (4) subscription.

1. The Growth of 3P Marketplace

Amazon Marketplace launched in November 2000, which started out as an attempt to copy eBay’s business model and focused on being a platform for users to buy and sell second-hand items.

“There’s always been a huge desire among customers to buy used, rare and collectible merchandise, and we’re only beginning to understand how Amazon Marketplace can channel that demand to benefit customers, manufacturers, publishers, artists and the industry as a whole.” — Jeff Bezos, 2001 press release.

There was plenty of resistance, coming from different stakeholders such as publishers which complained that the second-hand marketplace would rob authors of their royalties, and from competitors such as Walmart which tried selling its books at a loss to crush Amazon. More importantly, there was plenty of resistance coming from Amazon’s management team as they were cannibalizing their own 1P marketplace.

Customers got to choose whether to purchase the item from Amazon itself or from a third-party seller. If they chose the latter, either because the seller had a lower price or because the product was out of stock at Amazon, the company would lose the sale but collect a small commission.

Neil Roseman, one of Amazon’s earliest executives said, “Jeff was super clear from the beginning, if somebody else can sell it cheaper than us, we should let them and figure out how they are able to do it.”

And over time, we can see that Amazon’s 3P marketplace took off and accounts for ~55% of Amazon’s total e-commerce sales.

Many investors keep harping about the value of AWS for a good reason. It is a highly profitable business with high switching costs and economies of scale. But many missed out on the even more incredible beast: its 3P marketplace which is a high margin and high growth business.

Amazon doesn’t break out its 3P marketplace margins, but when we look at established 3P marketplaces, the gross margins are in the range of 65% to 80% with operating margins of 20% to 30%.

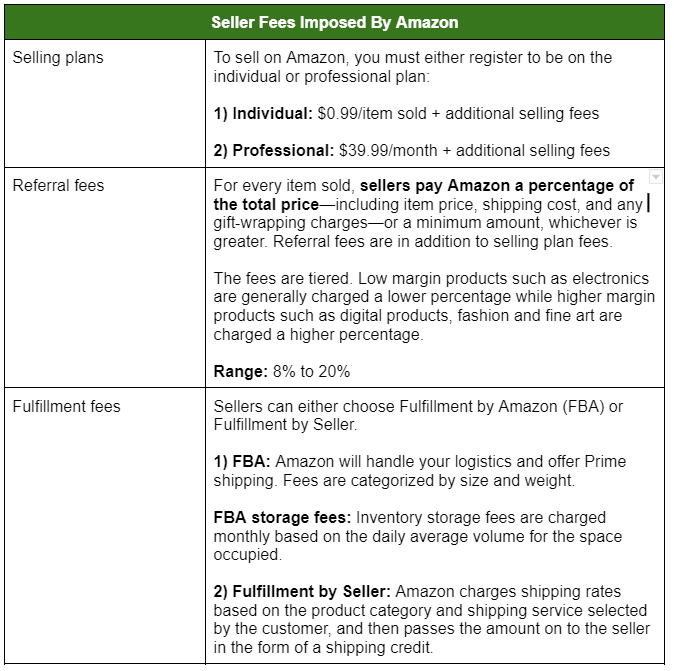

When merchants sell on Amazon, there are mainly three types of fees they will have to pay Amazon:

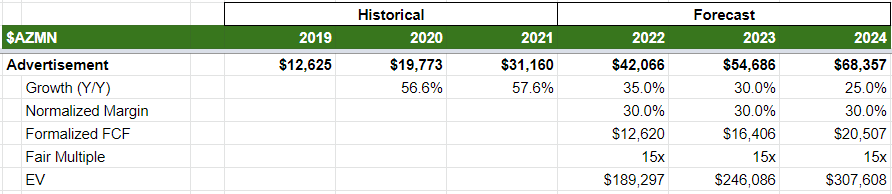

The rapid growth of its 3P marketplace gave rise to its even more profitable advertisement arm.

2. Advertisement

So how huge is Amazon’s advertising revenue?

Top ad revenue generators for 2021:

• Google Search: $149B

• Meta: $115B

• Amazon: $31B

• YouTube: $29B

• Microsoft: $8.53B

• Apple: $5B

• Snap, Pinterest & Spotify: $7.8B

Out of nowhere, it climbed to third place! While Amazon has not yet broken out its advertisement margins, the largest digital advertising companies typically make between 40% and 50% operating margins. Its operating margin is likely higher given that advertisement is an add-on to its retail business.

Look at how fast Amazon has grown for the past the three years:

• $12.6B

• $19.8B (+57.1%)

• $31.2B (+57.6%)

Stratechery highlighted three advantages of Amazon’s advertising business relative to Facebook’s:

1. Search advertising is the best and most profitable form of advertising.

When advertisers know that they are showing their ads to receptive customers, the more they will bid on that ad slot, and text in a search box is always more accurate than best targeting.

2. Amazon is not subject to any data restrictions.

Data collection, ad targeting, and conversion all happen on Amazon’s platform – Amazon.com and the Amazon App. App tracking transparency (ATT) only affects third parties, so it doesn’t affect Amazon at all.

3. Amazon benefits from ATT.

E-commerce was one of the most affected areas of Facebook advertising. In the case of an e-commerce seller whose Facebook advertising suddenly underperformed due to ATT, it is natural to shift the advertising budget to Amazon or Google.

The increasing emphasis on privacy against third party applications will benefit Amazon at the expense of social media companies. And this is on top of the mega tailwind of advertising dollars shifting from traditional mediums (e.g. TV and radio) to digital mediums.

3. Amazon Web Services (AWS)

The rise of cheap computing infrastructure (AWS) enabled anyone with an idea to have access to world-class computing power, storage, and web hosting, without having to hire teams of engineers or buy expensive servers.

AWS was an Amazon invention that, oddly, went unchallenged for seven full years! The concept was touted as absurd when they first started it and this allowed them to be well entrenched as the market leader in this field. And cloud computing, similar to e-commerce is one where scaled economics shared makes the market leader stronger as they grow.

The story of cloud computing is similar to that of electricity retailers. In the late 1800s, factories and businesses each had their own power plant. It was expensive to maintain and wasn’t a core competence of these businesses. Entrepreneur Samuel Insull pitched to these businesses to buy electricity from his centralized power station on a usage basis rather than maintaining their own expensive and complex power plant. Today, very few businesses choose to own their own power plant instead of relying on a central power grid.

The concept of cloud computing is the same. Get rid of your on-premises servers, engineers, and data centers. Instead, buy the compute power, storage, and any business logic you require (databases, machine learning, etc) and pay for what you use. AWS is also highly scalable and can accommodate rapidly growing businesses or adjust to peak sales periods (e.g. at the end of the year).

When Amazon broke out its AWS segment, it was a sight to behold:

Sales has been growing at above 30% and operating margins are coming in strong at 30% despite dropping prices a whopping 107 times!

This is operating leverage and scaled economics shared at its finest, where increased sales begets a lower cost structure and by passing some savings to your customers, they reward you with increased sales. This forms an incredible flywheel for the market leader and it is extremely tough to disrupt.

4. Subscription

Amazon Prime provides fast, free shipping on millions of items, access to stream award-winning movies and series, and other benefits. As Bezos wrote in an earlier shareholder letter: “We want Prime to be such a good value, you’d be irresponsible not to be a member.”

Amazon Prime was launched in 2007 with two-day free shipping, and Bezos decided on $79 per year, saying it needed to be large enough to matter to consumers but small enough that they would be willing to try it out.

At that price point, Amazon forecasted that it’ll cost the company $160 in shipping, far above the $79 fee.

And it’s not just about throwing in a bunch of benefits to their Prime members. In the vast sea of offerings included within their membership, Amazon utilizes recommender systems to engage members with information about Prime benefits that they would find most interesting. Afterall, it’s not just how much value you provide, but how much value members perceive. If you are interested about how their algo works, you can read more here: The science behind Amazon Prime.

Look at how big this high-margin subscription business has grown into, from 46 million in 2015 members to 200 million members in 2020 worldwide.

Likewise, the high margins subscription revenue grew to an astounding $31.8B business. For comparison, Netflix and Costco’s subscription revenue came in at $3.3B and $3.9B respectively.

Prior to 3 Feb 2022, Amazon offered a monthly and annual membership payment option of $12.99 per month (or $155.88 in 12 months) or $119 per year respectively. Also, there is the option of signing up for Prime Video membership at $8.99 per month.

And Amazon Prime membership has consistently high renewal rates! Annual memberships are consistently above 90% and monthly memberships hovering around 70%. Slightly more than 50% of the members are monthly members. For reference, the Costco’s renewal for annual membership is at 90%.

Rapidly Improving Profitability Metrics

The growth of its 3P marketplace, advertisements, AWS and subscription revenues led to Amazon’s margins profile dramatically improving. This is despite the company facing significant headwinds in the supply chain and rising labor costs due to COVID-19, and heavy reinvestments into logistics.

From their earnings call in Q4 2021 “…we did see more than $4 billion in costs from inflationary pressures and loss productivity and disruption in our operations. The inflation primarily relates to wage increases and incentives in our operations as well as higher pricing from third-party carriers supporting our fulfillment network. Loss productivity and network disruptions were driven primarily by labor capacity constraints due to challenges in staffing up our facilities for peak. This is driven by the very tight labor market in the second half of 2021 and more recently by the emergence of the Omicron variant.”

Amazon’s margin profile will continue to look better for several reasons:

1) Hangover costs from COVID-19 will diminish over time

2) Operating leverage kicking in across all its services

3) Further growth from its high margins operations

The King of Side Hustles

Mohnish Pabrai coined the term “spawner” to describe companies that can expand into multiple verticals and extend their growth runway. And Amazon has been a best in class spawner, turning their side hustles (Ads, AWS, 3P, etc) into core revenue drivers.

In this slide from Social Capital, we see how Amazon has been able to turn costs into revenue generators. Not many companies have it in their DNA to enter so many different verticals and to do it that well.

Reinventing Amazon to Become a Building Block

Today, Amazon has reinvented itself to be the core building block of many businesses. It’s no longer that juggernaut that’s out there to destroy businesses (remember Jeff Bezos famous line “your margin is my opportunity”), rather it has become a platform that enables multiple businesses to build their business on top of Amazon.

AWS has enabled significant advancement in technology because it has made computing power so cheap and accessible for new companies to experiment and innovate.

Amazon’s 3P marketplace takes care of SMBs warehousing and fulfillment needs, allowing business owners to focus on the product itself and marketing.

Amazon Kindle’s distribution network gave self-publishing authors a platform to push out their work at low costs.

And many more!

Amazon’s Long Runway

AWS

For AWS, IDC forecasts that the combined Public Cloud revenue will grow to $400 billion in 2025 with a CAGR of 28.8% from 2021-2025.

AWS is currently the market leader with more than 50% market share of the global IaaS and PaaS market. With scaled economics shared, it is reasonable to assume that AWS maintains market share of at least 50% by 2025.

eCommerce

It might seem like Amazon is already huge (it is), but e-Commerce continues to remain a small percentage of total retail sales in the US at 17%, compared to China’s 50%. e-Commerce penetration is expected to continue to grow in the teens for the next few years.

Likewise, Amazon is the dominant player in the US. In a survey by Applico, it is expected to increase its market share with GMV rising to $75 billion by 2023.

Advertisement

Likewise, digital ad spending is expected to continue. With stricter privacy rules, Amazon stands to benefit as marketing dollars will flow from third-party platforms such as Meta to companies who own their platform (including Apple with iOS and Google with search and Android).

Subscription

Amazon Prime Users are also expected to continue to march upwards. As Jeff Bezos said, “We want Prime to be such a good value that you’d be irresponsible not to be a member.”

Its US Prime Users is expected to grow at 2.12% over the next five years given that the bulk of the population are already members.

For Germany, it is expected to grow at 5.02% over the next five years.

For the UK, it is expected to grow at 4.05% over the next five years.

Also, I believe there is a strong untapped pricing power for Amazon Prime. With so much value being given, their subscriber count has continued to increase even with the price increases over the years.

Logistics as a Service?

Amazon is now doing more volume than FedEx and if history is an indication, very soon they will start selling extra capacity and provide Logistics as a Service.

Valuation

For valuing Amazon, we will value each business individually and I classify them into: (1) Subscription, (2) 3P Marketplace, (3) Advertisement, and (4) AWS.

Subscription

I will be valuing Amazon’s subscription together with its 1P Marketplace. A similar business for comparison would be Costco, which makes approximately 12% gross margins (by choice), which is enough to cover its operating expenses with some loose change. Its membership fees flow straight down, forming the bulk of its net income.

Amazon shares a similar philosophy, pricing its products at near breakeven and monetizing primarily from its Prime Member fees. For Costco, its free cash flow (FCF) as a percentage of its membership fees revenue is generally between 100% to 120%.

For Amazon, we will assume a 90% FCF margin for its subscription revenue and apply a 20x FCF multiple (Costco’s priced at approximately 25x FCF).

3P Marketplace

For its 3P Marketplace, using mature 3P players as a proxy, we will assume a 20% FCF margin and apply a 15x FCF multiple.

Advertisements

For advertisements, using Google and Facebook as a proxy, we will assume a 30% FCF margin and apply a 15x FCF multiple.

AWS

For AWS, we will assume a 25% FCF margin and 25x multiple given its stickiness and growth runway.

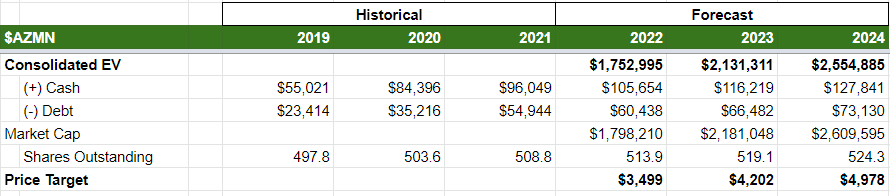

Assuming that its cash, cash equivalents and debt grows at 10% annually and shares outstanding to increase at 1% annually.

This will give us an estimated price target of $4,978 by 2024, which is a 20% CAGR from 23 Feb 2022 share price of $2,896.

I have made the intrinsic value spreadsheet available for you here. Feel free to save a copy for yourself and play around with the variables.

Risks

Apart from the usual regulations and antitrust lawsuits against mega caps, we need to watch two other risks: (1) Competition, and (2) Edge computing.

Competition

Competition is brutal in retail and in cloud computing. Two days shipping used to be above and beyond, but now other retailers have begun to match that. Furthermore, the popularity of order and pick up may also reduce the attractiveness of Amazon’s convenience. But of course, even before the competition had the chance to catch up, Amazon began rolling out same-day delivery and 2-hours delivery for almost 200,000 items.

Likewise, for clouding computing they are constantly reducing prices and putting pressure on the competition. For example, at a $19.2B run rate, Google Cloud is still running an operating loss of $3.1B. In 2017, AWS was already throwing off operating profits of $4.3B on a $17.5B run rate. Amazon passing on savings from operational efficiencies to consumers makes them hard to compete against.

Edge Computing

Competition from AWS is not limited to cloud players, but also edge computing and multi-cloud setups. If edge computing takes off and latency-sensitive applications are deployed at the edge as opposed to centralized cloud services, it’s possible that some of the dollars flowing to AWS will move to edge computing platforms.

Conclusion

Since day one, Amazon has been focused on maximizing free cash flow per share in the future. The company has invested heavily into building up its moat and making sure its customers are happy, so much so that it’s extremely difficult for competition to catch up. With the spawn of high margins revenue segments such as advertisement, AWS, 3P marketplace and subscription, Amazon’s profitability profile is likely going to see a strong uptick very soon.

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in Amazon at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).