If you wish to become financially independent, being in your twenties is arguably the most important decade in your life as you have a long runway ahead of you. It is also at this stage where we are prone to making the wrong financial decisions as we are not trained financially.

For many, receiving their first paycheck often means that their spending will increase accordingly. Also, many insurance advisers will approach and encourage you to purchase a barrage of confusing insurance products. Most would be afraid to start investing and accumulating wealth. To sum it up, most of us are losing precious time and giving up opportunities which are imperative for compounding to occur.

In this article, I will share more about setting up a financial framework for young working adults.

1. Build an Emergency Fund, NOW!

Build up an emergency fund which would cover 3 – 6 months worth of expenses. The need for this is prominent, especially in today’s Covid-19 environment. The fund protects against unforeseen medical expenses, home repair and most importantly, unemployment. This helps prevent you from liquidating your investments at the worst of times, as unemployment usually coincides with a recession.

2. Getting the Right Insurance.

When it comes to insurance, I adhere to Warren Buffett’s suggestion, “Never ask a barber if you need a haircut.” Do not rely solely on your agent’s advice. Instead, spend time to understand the products for yourself. Without careful consideration, 2 seconds spent on signing the contract may result in 2 decades of regret.

Having said that, insurance is essential as it protects against downside risk. As a rule of thumb, NEVER EVER mix investment with insurance products. For instance, Investment-Linked Insurance Products (ILPs) and endowments should be avoided, especially if you are young.

To help streamline your research, I have listed a summary of essential insurance types, in order of importance:

The following are good to have if you can afford it:

3. Setting a Budget and Automating Your Finances.

When it comes to budgeting and following through on it, I recommend Sethi Ramit’s method. Create a spending plan into 4 major buckets where your money will flow:

- Fixed costs (e.g. phone bill, rent, utilities, insurance)

- Investments

- Savings (e.g. holiday, wedding, mortgage down payment)

- Guilt-free spending (e.g. shopping, movies, restaurants)

The key to success here is in automating the flow of your money. By automating the flow of money into your Investment account and Savings account, you protect your budget against temptations.

You may apply the 50-30-20 rule here for simplicity:

- 50% for Expenses (includes fixed costs and guilt-free spending)

- 30% for Investments (retirement)

- 20% for Savings

4. Consistently investing in an ETF

Successfully picking individual stocks can be difficult and time consuming. For most people, investing in a diversified, low-cost index fund would work best. Over the past 90 years, the S&P 500 averaged a 9.53% annualized return—beating 90% of active fund managers on an after-fee basis.

Investing in an index such as the S&P 500 is akin to buying the 500 biggest companies in USA, including the likes of Amazon, Google, and Apple. The procedures are relatively simple; you just need to open a brokerage account and set recurring purchases (e.g. Regular Savings Plan). You may consider setting your purchases on monthly or quarterly basis.

Apart from low fees, indexing helps to fight against an investor’s greatest enemy—themselves. This prevents us from buying high (out of FOMO), and selling low (out of fear). It is also a great solution for investors with no time or interest in researching companies.

I would recommend against Singapore’s Straits Times Index (STI) ETF as the portfolio of companies in STI are of lower quality (i.e. less growth).

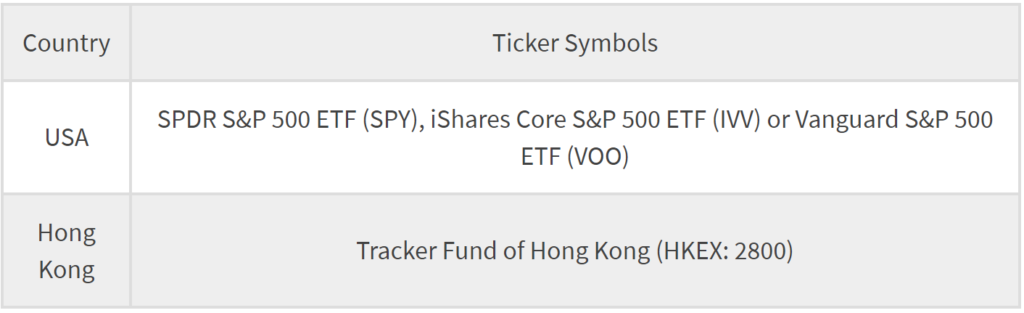

You may consider the following low-cost ETFs for exposure to the S&P 500 (USA) and the Hang Seng Index (Hong Kong):

To sum it up

Your actions today will determine if you are able to retire comfortably decades down the road. It is important to take action on building an emergency fund, budgeting, and investing, but it is also important to avoid mistakes when it comes to purchasing insurance.