Valuation is an imprecise art and any sort of valuation exercise is a rough estimation of a company’s intrinsic value—future cash flow discounted to the present. It is helpful to understand what are the levers to a company’s valuation, or in fancy terms, “think in first principles”—to understand if market swings are justified or if they are just one of Mr. Market’s mood swings.

I earlier wrote about why the market overreacted in March 2020, with shares of high-quality companies plummeting 30% to 50%. Back then, it seemed like a great buying opportunity because when thinking about valuation from first principles—discounted cash flow analysis—if we assume losing 12 to 24 months of cash flow, it should reduce a company’s intrinsic value by no more than 5% to 10% (assuming they don’t go kaput, of course).

You may check out the article here: Has The Market Bottomed Out?

This latest white paper by Michael Mauboussin: The Economics of Customer Business is great for helping us understand the levers of customer-based corporate valuation (particularly SaaS companies).

Let’s begin!

Customer lifetime value (CLV) is the present value of the cash flows that a customer generates while they are engaged with the firm minus the cost to acquire the customer.

Let’s take Netflix, it costs $12 per month, or $144 per year. Assuming on average, each customer stays subscribed for 10 years, and spends a grand total of $1,440. But as we know, a dollar collected 10 years later is worth way less than a dollar collected today.

When we perform a DCF on the $144 that will be collected for 10 years, we find that the present value of these cash flows comes up to $973.30.

Before customers subscribe, there will be some cost incurred by Netflix to entice potential customers—marketing, advertising, etc. This is referred to as the customer acquisition cost (CAC).

A really quick and dirty way to calculate CAC is to take the marketing expenses and divide it by the number of onboarded customers. Netflix spent $2.2 billion in marketing and acquired around 29 million customers. Hence, CAC comes up to about $77.

Comparing the value of a customer ($973.30) vis-à-vis the cost to acquire the customer ($77) might suggest that Netflix has great unit economics.

But this method of calculating CAC is somewhat off the mark. Why?

Firstly, it can overstate CAC as not all sales and marketing expenses are dedicated solely to acquiring new customers.

Secondly, CAC could come in other forms, including freemium offerings, hardware subsidies, promotions, and installation costs which would be reflected as cost of goods sold (COGS) instead of just marketing expenses.

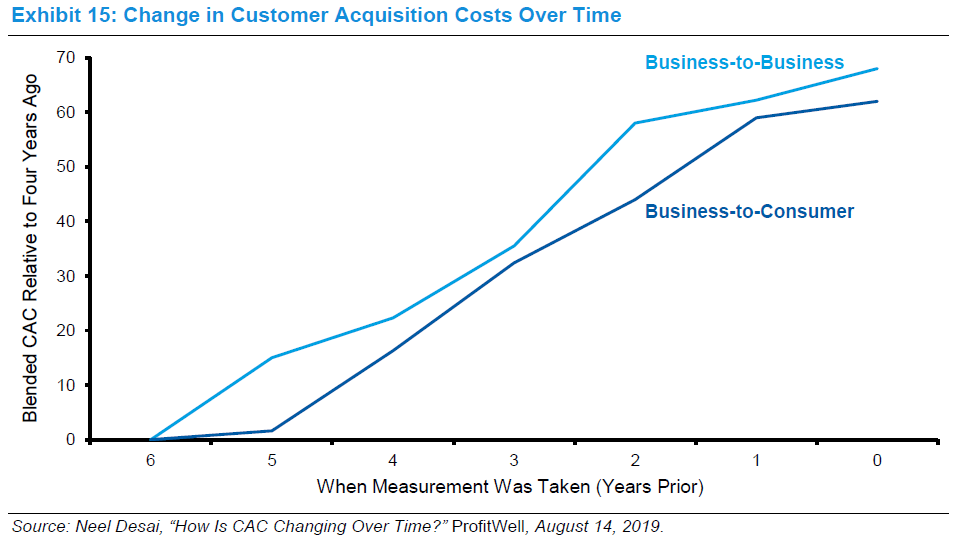

Thirdly, CACs tend to rise over time as a company makes its way from the early majority to the late majority adopters. In other words, it needs to spend more and more money on convincing “boomers” to try out their products.

People belonging to the early majority category will adopt new ideas way before it becomes mainstream. Think of all the techie and those people who will queue in front of a “fruit” store for hours on the day of launch.

Late majority are people who are a skeptical group, who are willing to be onboarded only after the majority of the people are on it. Think of those who comment “Uber isn’t safe” or “ecommerce is a scam”.

On the other hand, CAC can decrease for a business that enjoys a network effect—when the value of the product or service increases as more people come on board. Looking at ride-sharing companies such as Uber and Grab. When they were starting off, they dished out tons of discounts and bonuses to drivers and passengers in order to acquire these users. However, as word about Grab and Uber spread, more people came on board, and the amount of discounts decreased as discounts were no longer essential to attract customers.

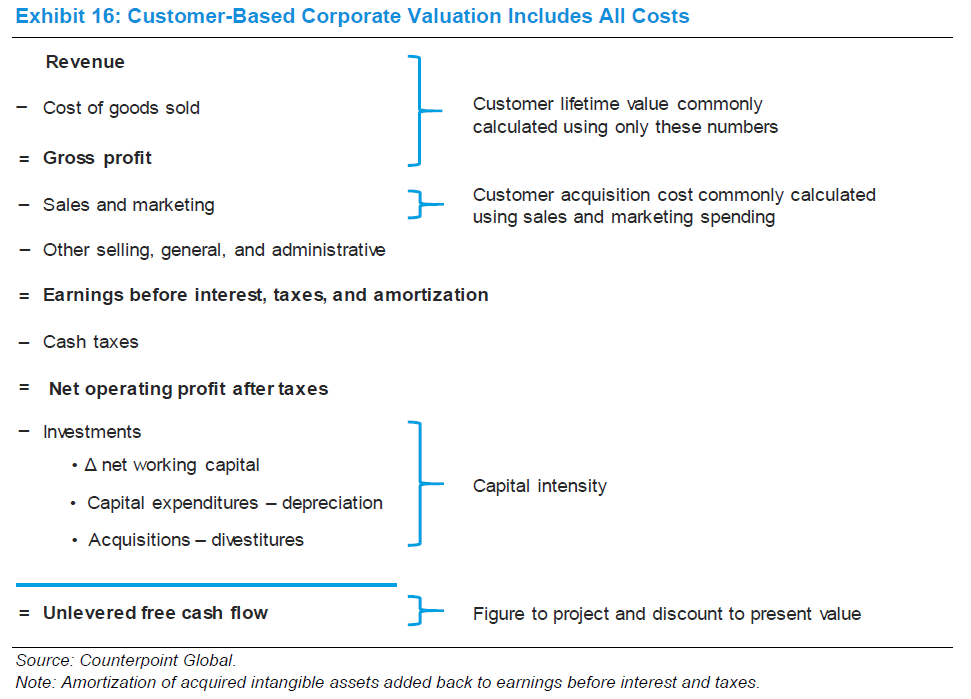

Mauboussin went on to add that LTV/CAC calculations should include all costs—many items such as costs of goods sold, sales and marketing expenses, research and development (R&D), and other selling, general, and administrative (SG&A) expenses are rarely considered in the calculation of CAC.

To arrive at the unlevered free cash flow necessary for a discounted cash flow analysis, we should also take into account working capital changes and capital expenditures. In other words, how much of the cash generated is locked up in the business for day to day operations?

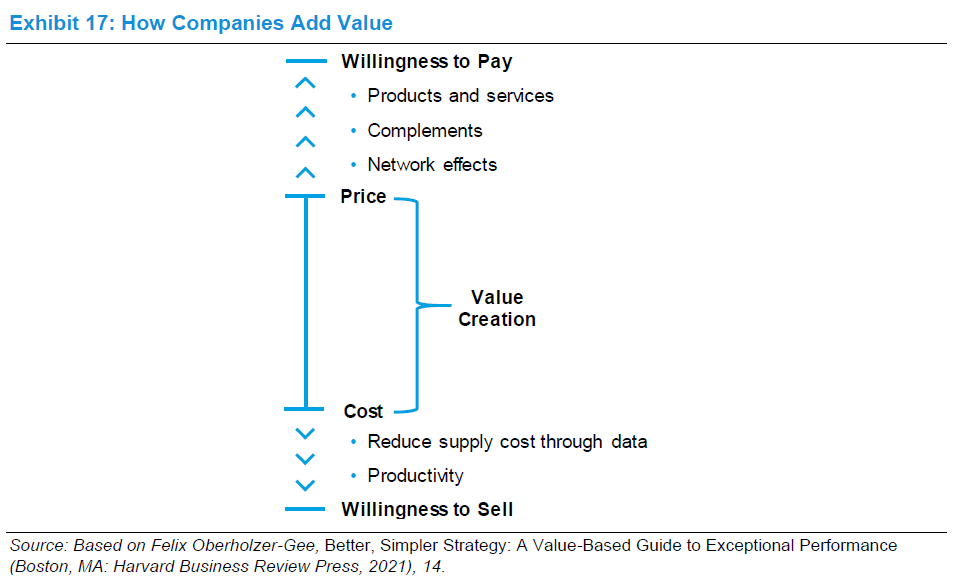

When it comes to creating value, there are four numbers to consider:

- Willingness to pay (WTP), the maximum a customer would pay for a good or service

- Price the firm charges for that good or service

- Cost for delivering the product

- Willingness to sell (WTS), the minimum payment a supplier would accept to provide a good or service

Customer LTV relates to both price and cost, so it is important to look at all factors.

To increase value, we could look into customers’ WTP and the price charged.

- Increase WTP by earning a reputation of always placing the best interests of the customer first.

- Reducing search costs, customized recommendations with data insights on consumer behaviour lead to further sales.

- Introduce products that complement each other, such as smartphones and smartphone applications.

- Increase network effects. Take Amazon, for example—as more customers come on board, more sellers will want to be on the platform and vice versa. With more choices/greater selection, customers will be more willing to pay for Amazon Prime Membership.

We could also create value by lowering cost and preserving value for suppliers by lowering WTS.

- Reduce supply cost through data. For example, through faster inventory turnover—keeping inventory locks up capital, imagine having a ton of goods that’s stored in the warehouse, those are cash that are locked up as goods.

- Increase employee productivity. By appealing to extrinsic motivation—paying more, or by intrinsic motivation—autonomy, mastery, and a sense of purpose.

Investors can consider the customer as the basic unit of analysis in understanding value. A company’s value creation opportunity can be framed by the concepts of WTP and WTS.

For more, do check out the full white-paper by Michael Mauboussin: The Economics of Customer Business.