Prior to seeing Warren Buffett and Charlie in person, I attended the Value Investor Conference, which featured speakers such as Chuck Akre, Tom Russo, François Rochon, Robert Cialdini and more.

Over several posts, I’ll share what I learned from my week in Omaha!

Let’s get started.

Dr. Robert Cialdini at the Value Investor Conference

Dr. Robert Cialdini: The 7 Universal Principles of Persuasion

1. Scarcity

Cialdini began by discussing scarcity. It’s human nature to want more of what we can’t have. According to him, this is closely related to Daniel Kahneman’s loss aversion bias, people are more likely to act when they perceive that they are at risk of losing, rather than gaining.

Instead of telling homeowners they’ll gain $1 a day if they insulate their homes, tell them they’ll lose $1 a day if they don’t! There is a significant increase in action rates in the latter case.

2. Authority

In today’s world of information overload, people often turn to authorities for guidance. According to Cialdini, we look to what legitimate experts are doing for reference.

The endorsement of sports gear or supplements by professional athletes is a popular example. Consumers have a hard time choosing between so many products. By observing what these experts do or use, we could speed up the decision-making process.

Credibility can also be built by using multiple testimonials. Multiple testimonials, contrary to conventional wisdom, amplify the impact, instead of diluting it. To establish authority right from the start, he suggested placing testimonials first.

3. Social Proof

Then Cialdini talked about social proof, the tendency to seek confirmation from others when we are uncertain. We are more likely to try a software our friends recommend, bypassing the need to test it personally or do extensive research.

The research of Dr Robert Cialdini raised tax payment compliance in the UK by showing taxpayers that X% of people pay their taxes on time in their community. By zooming in on their peers, compliance rates were raised.

4. Commitment/Consistency

We inherently desire to be and appear consistent. Cialdini explained that persuading people to take a small step in our direction often leads to them taking bigger steps later.

He cited the case of Gordon’s Restaurant, which significantly reduced no-shows by simply adding a pause after asking customers to call if they needed to cancel their reservation. This pause allowed for a verbal commitment, reinforcing the principle of consistency.

5. Reciprocation

Moving on to reciprocation, Cialdini emphasized the power of giving first. He used the example of a Brazilian McDonald’s experiment where giving a balloon to a child before ordering led to a significant increase in the family’s purchase.

Balloon is given before vs after order:

– Size of family purchase +25%

– Size of coffee purchase +20%

Coffee spending, which is obviously for the adults, increased despite the balloon for the children and not the adult. The rationale is the principle of unity, which is covered under principle 7. When you do a favor for my child, you do a favor for me.

This principle doesn’t necessitate material gifts – focused attention, information, or effort can also trigger the reciprocation instinct.

6. Liking

Positive connections breed liking. Three key components facilitate this: similarities, compliments, and pleasant experiences. Cialdini encouraged us to find and highlight similarities when trying to connect groups. He also emphasized the power of complimenting traits rather than actions, as traits are enduring qualities. Lastly, associating with pleasant experiences can significantly enhance liking – a simple smile can be a game-changer.

7. Unity

The final principle discussed was unity, the sense of togetherness or “We-ness.” Cialdini noted that highlighting existing unities and asking for advice rather than opinions could foster unity. He cited Warren Buffett’s practice of referring to his shareholders as family as a perfect example of fostering unity.

Joseph Shaposhnik: Focusing on businesses that we can predict

Joseph manages TCW’s New America Premier Equities Fund. During his presentation, he emphasized the importance of focusing on businesses that we can predict. We do not need to have an opinion on every stock that crosses our desk.

According to him, if you cannot predict them, how can you value them? The fund’s mantra is to invest in businesses that generate free cash flow and grow at a predictable pace.

Because of the fund’s emphasis on predictability, they prefer companies with recurring income for the following reasons:

- Far easier to value

- Far easier to manage; fewer emergencies

- Increases the odds investments in projects pay off

- Allows management to deploy capital in a shareholder friendly manner

However, not all recurring revenue business models are created equal.

Transactional recurring revenue and subscription recurring revenue

The transactional recurring revenue model is based on volume levels or transaction activity (aka usage). Customers’ business activities may be cyclical and unpredictable, making this type of recurring revenue less predictable. Twilio or Amazon Web Services, for example, charge consumers based on usage.

Subscription recurring revenue refers to regular payments made in exchange for goods and services. With this type of recurring revenue, you can predict it with a high degree of accuracy. Adobe and Microsoft 365, for example, have fixed subscription fees regardless of how many times consumers use them.

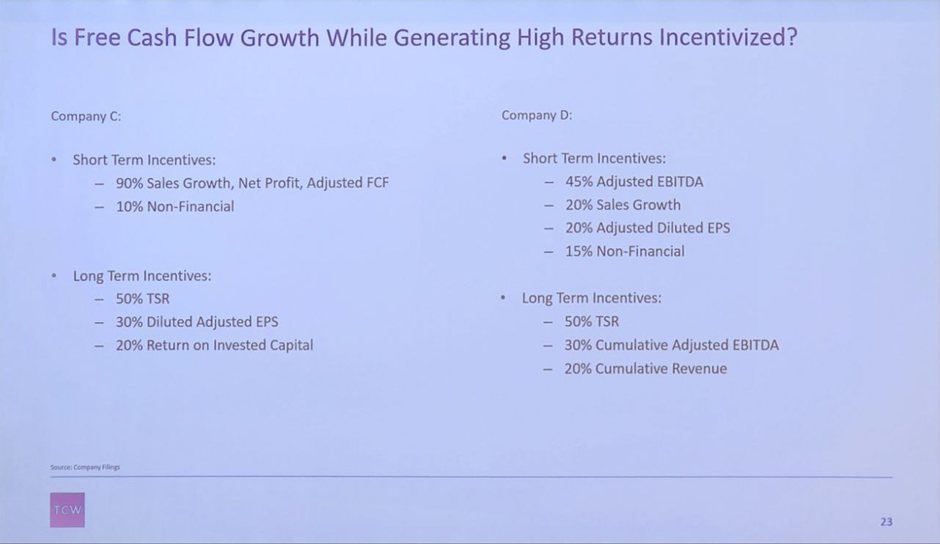

Study management’s incentives

Incentives for management will strongly impact the company’s return on invested capital and free cash flow.

The incentive structure of Company C rewards management directly for FCF and ROIC (20% or more), resulting in steadily rising FCF and ROIC.

That’s all I have for you today!

I will be covering more lessons from the Value Investing Conference in the upcoming posts and… of course, my lessons from Buffett and Munger sharing during the Berkshire AGM.

Stay tuned.

Thomas

Very helpful. I always read your post and find them meaningful. Keep helping us

Thanks Tejinder! Appreciate it.

Hi Thomas many thanks for your sharing!

I was there too (but in the overflow room), and would like to add on Joseph Shaposhnik’s interpretation of the Warren Buffett Test around “certainty” that I liked very much:

1. How much certainty can we evaluate the economic characteristics of the business? i.e. Will their product / service still be relevant in 5yrs-10yrs [Sales & Profit growth]

2. How much certainty that management can realise the business’s full potential and employ cashflows/excess cash wisely? [ROIC]

3. How much certainty that mgmt can channel the rewards of the business to shareholders rather than to themselves? [Corporate Goverance]

4. What is the price of the business? [Cheap enough?]

Hey Darrell,

That’s awesome. Saw quite a few Singaporeans at the event.

Happy to know that there’s so many like-minded folks from SG.

Great additions on Joseph Shaposhnik’s interpretation of the Warren Buffett Test around “certainty”.