Starbucks is my first multi-bagger and it provided me with returns beyond just profits, it was the investment that made me understand the wealth-generating capabilities of investing in high-quality compounders—or, as many would say, that aha moment!

When we refer to high-quality compounders, it means that these companies are able to grow without using a lot of capital, able to generate returns well above its cost of capital, and more importantly, this group of companies have a moat to defend itself against competition.

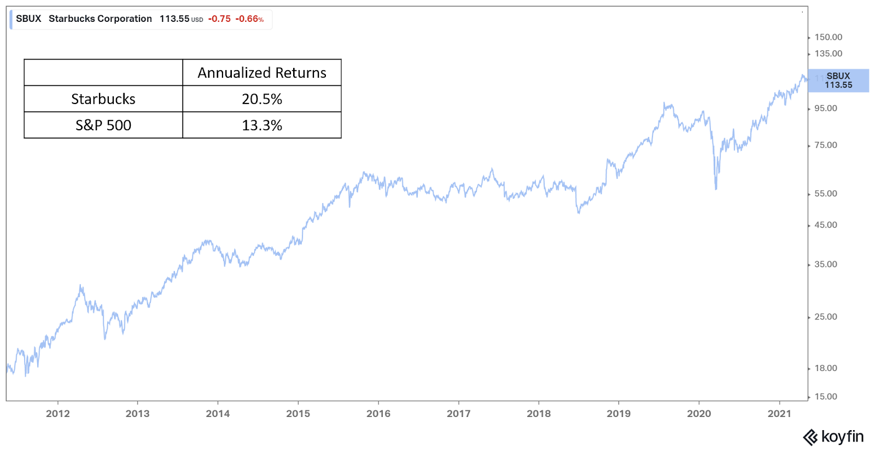

Let’s take a look at how Starbucks fares when it comes to shareholders’ return. Across a 10-year period, investing in Starbucks would have brought about a 20.5% CAGR, a good 7.2% above what the S&P 500 could have delivered!

This exceptional return was brought about by their strong brand, which allowed them to command a premium pricing whilst increasing market share.

Exactly how strong is the Starbucks brand?

When a coffee cup was aired on one of the Game of Thrones episodes, netizens immediately concluded that dragon queen Daenerys Targaryen needed her cup of latte.

And Starbucks was quick to capitalize on the blunder! 😂

More importantly, it shows that people have associated a coffee cup synonymously with Starbucks. Starbucks has occupied this strong share of mind without spending excessively on marketing efforts such as celebrity endorsements, sports sponsorships, or dishing out excessive discounts.

Compare this to their competitor in China, Luckin Coffee which has fallen from grace since their accounting scandal was exposed.

Luckin was incurring large expenses from celebrity endorsements and was dishing out discounts to increase market share to the point that they weren’t profitable on an unit economics basis, i.e., their losses increased with each cup of coffee sold.

For accounting buffs only: Luckin’s gross margins are positive because they parked their heavy discounts under operating expenses instead of the cost of goods sold.

Then on the other hand, you have Starbucks who charges a huge premium and is able to attract a large crowd in China.

Business Model

When it comes to analysing restaurant companies, there are three main business models:

(1) Company-owned stores: Where the company set up the restaurants themselves and earn revenues directly from customers who make visits to the restaurants.

Chipotle is an example of this business model, and the primary reason for companies doing this is to maintain quality and control over its restaurants.

(2) Licensed-stores: Where the company earns by franchising the restaurant, earning revenues from royalties, licensing fees, and a margin from the sale of coffee, tea, food, and other products to licensees.

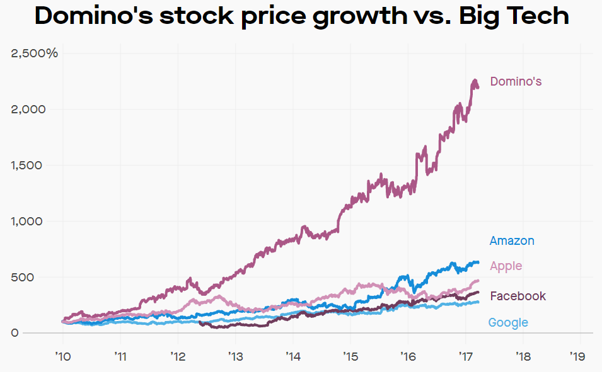

Domino’s is an example of this business model, and the primary benefit is that you don’t need capital to expand. The franchisees come up with the capital and Domino’s earns by collecting royalties, a cut of the franchisees’ revenue and by selling pizza dough and the equipment. With a proven product, restaurants adopting the licensed model could deliver tremendous returns due to how fast they are able to grow without capital constraints. So much so that they have outperformed our big tech firms by a huge margin when it comes to shareholder returns.

(3) A mixture of both of the above! This is the strategy Starbucks chose, with 80% of its revenue coming from company-owned stores. This is a different approach from McDonald’s franchising approach, whereby company-owned stores make up 45% of revenue.

There are good reasons for Starbucks adopting a mixed approach, with a preference towards having most of its stores being company-owned in important growth markets, to have control over the quality and branding of Starbucks, and in creating an incentivized culture.

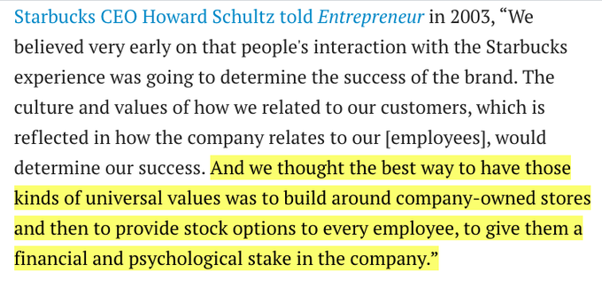

Howard Schultz, the founder and long-time CEO on creating an incentivized culture:

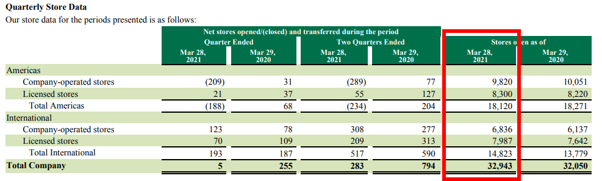

Here is a high-level view of the store counts broken out by company-owned vs licensed.

The total store count at the end of 28 Mar 2021 was 32,943. In perspective, McDonald’s has 39,198 restaurants at the end of 2020.

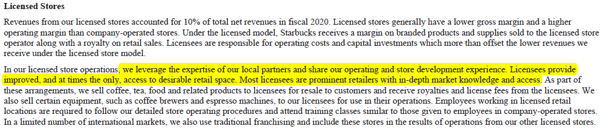

Now that we understand why running company-operated stores is important to Starbucks, why then do they have so many licensed stores, especially in international markets?

The reason is outlined in their annual report:

For emphasis, “Licensees provide improved, and at times the only, access to desirable retail space.”

When we look at the location of Starbucks in its international markets such as Japan and Thailand, it’s quite insane how good their locations are, and it’s also crazy how localized their designs are.

I mean, just take a look at these:

Right at the heart of Shibuya crossroad in Tokyo, one of the busiest and most touristy areas in Japan.

Edo style Starbucks in Kyoto.

Starbucks Reserve in Jewel, Changi Airport, Singapore, which looks more like an art museum.

With prime locations and best-in-class interior design and experience, these coffee houses basically market themselves. Customers are drawn to share their experiences on social media and be associated with the brand.

As Seth Godin, author of This Is Marketing, says, “The secret to marketing success is no secret at all: Word of mouth is all that matters.”

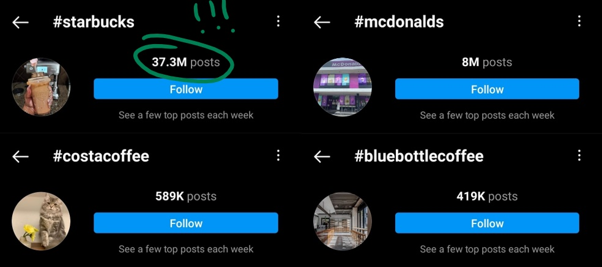

And Starbucks is one of the best at that—getting consumers to share their experiences at Starbucks on social media.

Just take a look at how much shares Starbucks gets from Instagram, the next top 10 competitors won’t come close to taking on the green mermaid when it comes to being viral.

If there’s one thing you can’t buy, it is word-of-mouth marketing, and Starbucks is able to be at the top of consumers’ mind thanks to social media. And this benefit is well reflected in Starbucks dominance in specialist coffee market share.

Now, let’s take a closer look at the growth in store locations by three geographies:

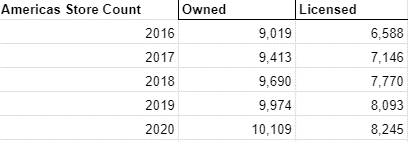

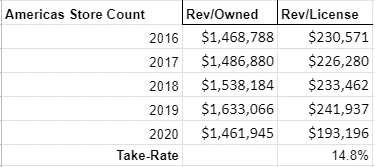

Americas (US, Canada, Brazil)

There were 1,090 new company owned stores vs. 1,675 new licensed stores. There is a greater emphasis on growing with licensed stores.

Licensed stores are found in airports or in a Target. Starbucks licenses its brand in retail centers and acts as a franchisor. The employees in these locations aren’t actually Starbucks employees, rather, they are employed by the retail location.

Licensed stores are found in airports or in a Target. Starbucks licenses its brand in retail centers and acts as a franchisor. The employees in these locations aren’t actually Starbucks employees, rather, they are employed by the retail location.

Looking at unit-level metrics, in the Americas, revenue per owned store is about $1.63 million pre-COVID-19.

And you can see, on average, Starbucks gets approximately 15% revenue cut as a license partner.

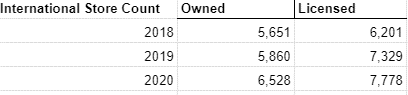

International

Starbucks only started to break out in the international store count format from 2018. There were 877 new company owned stores vs. 1,757 new licensed stores.

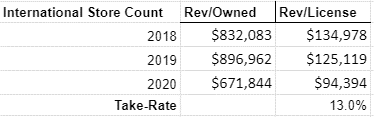

Looking at unit-level metrics, for its international markets, it made about $900,000 per store pre-COVID-19. And Starbucks gets approximately 13% revenue cut as a license partner.

While it seems like there’s a bigger emphasis on licensed stores in the international markets, Starbucks actually has different emphasis for CAP (China, Asia Pac) and EMEA (Europe, Middle East, Africa) regions.

As China is an important growth market, back in 2018 the company bought out its joint venture partners remaining 50% stake in 1,477 stores in China at $1.4 billion, which comes up to about $1.9 million per store.

On the other hand, Europe was the first place where Starbucks allowed franchising and it is the standard practice, and most of their stores are licensed.

Notice that the amount of revenue made in its international stores are about 50% of what they make in the Americas. This is largely because Starbucks is still young in Asia (especially China), with lower purchasing power. When the comps become closer to what they experience in the Americas, it would give Starbucks a decent growth runway.

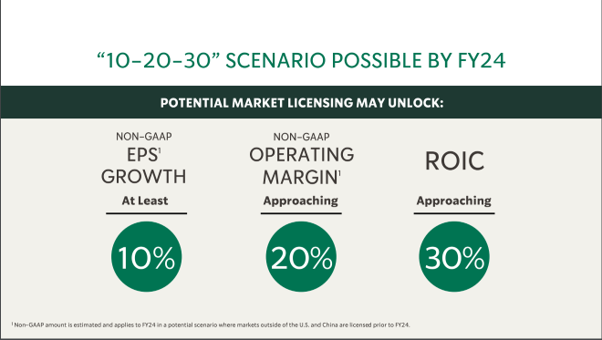

In the investor day 2020 presentation, Starbucks highlighted their plan to double down on markets driving their core growth engine with company-owned stores— China and the US, while pursuing the capital-light model of licensing for its other lower potential markets (e.g. they have licensed out all of their Singapore’s Starbucks stores).

This strategy of applying both company-owned stores and licensed stores would give them the benefit of both worlds. Allowing them to capture large market share while releasing capital in lower potential markets by adopting a licensing model instead. In turn, this will help boost EPS growth, improve operating margin profile and increase ROIC.

Unit Economics

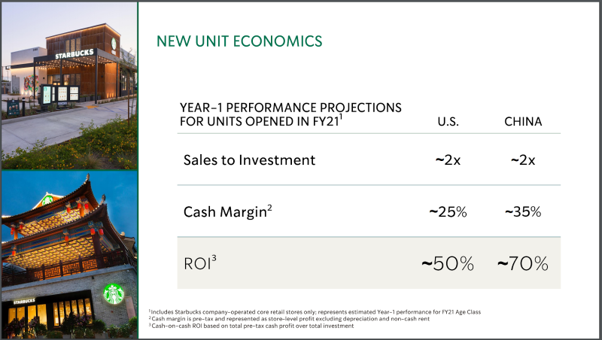

We know that Starbucks is a highly profitable business, but exactly how profitable are they?

New units in the U.S. generate ~25% cash EBITDA margins and ~50% pretax ROIC; new unit economics in China are even higher.

The payback period for US per Starbucks store is 2 years and for China it is 1.4 years. In other words, it only takes 2 years and 1.4 years respectively for Starbucks to earn back the cost of building a new store in the US and China respectively!

Increased Focus on Core Business and Digital Presence

Howard Schultz did a phenomenal job at bringing out the magic of coffee at Starbucks, making the green mermaid brand known throughout the world with his innovations—focusing on partners and customer experience, Starbucks Reserve, Starbucks Roastery, etc.

But he wasn’t the best capital allocator.

In 2012, Starbucks paid Bay Bread company $100 million for the La Boulange line of food and paid $620 million for the Teavana brand. A few years later, the company closed all 19 locations for its La Boulange bakery and all 379 locations for Teavana.

These were really costly mistakes and what Peter Lynch would refer to as diworsification.

In recent years, since Kevin Johnson joined as the Chief Operating Officer (COO) and subsequently succeeded Howard Schultz as the Chief Executive Officer (CEO), Starbucks has demonstrated a clear focus on its main coffee house business.

Let’s take a look at what they have done!

Outsourcing its Consumer Packaged Goods

They have signed an agreement for PepsiCo to sell and distribute Starbucks Ready To Drink (RTD) coffee and energy beverages.

Separately they also signed a deal with Nestlé to market Starbucks Consumer Packaged Goods (CPG) and Foodservice products outside of Starbucks coffee shops. Nestlé paid a really hefty upfront fee of $7.15 billion and will have to pay additional recurring market-linked royalties to Starbucks.

Both PepsiCo and Nestlé have a more extensive distribution prowess and you can see Starbucks CPG occupying good shelf space in supermarkets.

This move allows Starbucks to focus on what it does best, inventing new recipes and enhancing in-store experience while tapping on PepsiCo and Nestlé distribution prowess for a neat sum of fees.

Digital Presence

Starbucks is one of the first F&B players to launch its membership program on a mobile app. They understood that the future is digital and was quick to launch its app that allows members to collect points, to order and make payment, and collect data on its customers.

Currently, mobile orders represent 26% of US company-operated transactions, up from 18% a year ago and they run one of the largest membership program in the F&B industry with 90-day active Starbucks Reward (SR) members in the US approaching 23 million as of Q2 2021, an 19% increase from just 6 months ago.

Starbucks serves between 80 to 90 million customers a year and the 23 million SR members account for 52% of US sales. That’s right, an SR member spends on average two to three times more than a non-member.

This is why the management has a lofty goal of doubling the amount of SR members to 46 million!

Here is how they plan to do it:

- Partnering with technology companies that provide machine-learning algorithms (e.g. Amperity and BRIDGE), to deliver personalized offers and experiences to non-members.

- With Stars for Everyone, customers can choose from a range of payment options offering convenience, flexibility, and choice.

- Using its artificial intelligence (AI) program—Deep Brew to enhance customers’ experience. While invisible to customers, the AI program frees up partners to actively engage customers and deliver a better experience.

AI can help do the heavy lifting on processes like inventory, supply chain logistics and replenishment orders, saving partners time and making sure nobody runs out of Nitro Cold Brew or Banana Nut Bread. AI can help managers predict staffing needs and make schedules. AI can help anticipate equipment maintenance well before an oven or a blender goes on the fritz.

For customers, AI can help provide a “radically personalized” and warm experience. Using AI in the Starbucks app or on the drive-thru menu will present customers with thoughtful, personalized choices based on their own preferences, but also on things like weather and time of day. With the explosive popularity of mobile ordering and delivery services, Starbucks is looking at how AI can help baristas make beverages in an order that takes the whole picture into account. For instance, if a store gets a digital order for four iced lattes but the customer is still 10 miles away, baristas might make other drinks first.

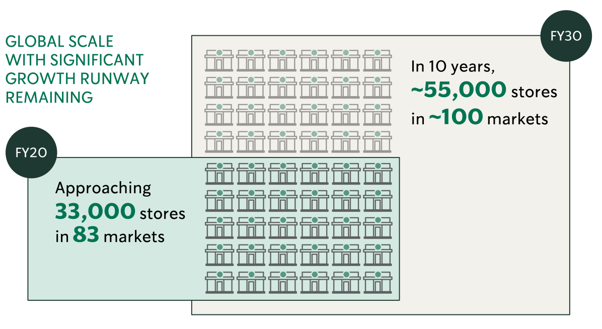

Growth at Scale

Growth is going to come mainly from two engines, firstly, opening more stores and, secondly, comparable-store sales growth—a combination of increased transactions, price increases, and/or increased ticket size (i.e. more stuff bought per transaction).

Starbucks aims to increase its retail penetration by expanding its store base to 55,000 by fiscal 2030, up 67% from 32,943 stores globally as of Q2 2021. Most of the new stores will be in China and the company expects the number of stores in China to grow at low teens annually.

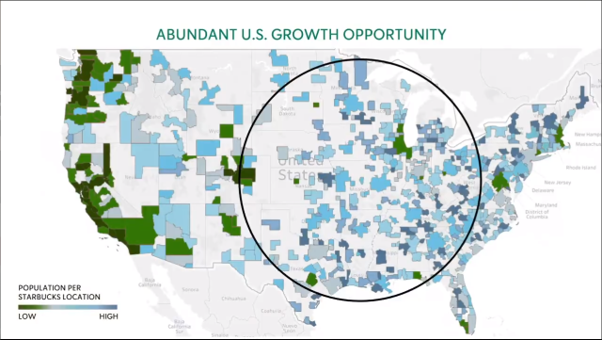

Even within the US, there remains quite a sizable room for growth outside of West America. Starbucks expects the number of stores in the US to grow at 3% annually.

On top of opening new stocks, Starbucks expects comparable-store sales growth of 4% to 5% annually, from 2023 onwards.

Americas Trade Area Transformation

Customer behaviors have changed due to the effects of COVID-19. The company shared five key insights into how customer habits have shifted, and they include: a need to be seen and feel connected with others; a desire for experiences that conform to their lifestyles; appreciation for consistent experiences; concern about using planet-friendly and sustainable products; and increased loyalty to brands that exhibit strong values.

As working from home gains popularity, Starbucks observed that a lot of their transactions have migrated from dense metro centers to suburbs and from cafes to drive-thrus. This was coupled with customers’ increased use of the Starbucks App to order ahead and the national availability of Starbucks Delivers through Uber Eats.

Based on these findings, Starbucks have plans to reposition 800 stores (~4% of total store count) in North America in 2021 into formats which support drive-thrus and curbside pickup to boost convenience for customers and deliver couriers to pick up their orders and reduce physical touchpoints for customers worried about COVID-19.

As of Q2 2021, they have closed 560 stores and approximately 200 of those stores have been rebuilt. Operating drive-throughs and pick-ups is expected to bring about margin improvement of 40 basis points (i.e., 0.4%) for this year.

Reinventing the Starbucks Experience in China

The digital landscape in China is much more competitive. In fact, most of the strategies that they are implementing in America were first tested in China. China is a mobile first country and most Chinese are on Alibaba and Tencent ecosystem. Starbucks was quick to launch its Starbucks Now Mobile Order & Pay service as a feature on Alibaba platforms such as Taobao, Amap, Koubei and Alipay. They have since expanded the service to WeChat.

Starbucks Now (also known as飞快 “Fei Kuai”) enhances convenience for both customers and couriers to suit the Chinese on-the-go lifestyle.

Mobile Order sales mix hit a record 34% of sales in China, up from 30% in Q1 with 15% driven by Starbucks Delivers and 19% from Starbucks Now. Starbucks Rewards customer engagement continues to grow as Mobile Order sales have more than doubled in China over this past year.

In 2021, Starbucks also launched its flagship store on JD.com, one of China’s leading e-commerce platforms, offering merchandise, stored value cards and seasonal food offerings among other products.

Financials

Barring the impact of COVID-19 for 2020, Starbucks has grown revenue at 10.1% CAGR from $14.9 billion in 2013 to $26.5 billion in 2019, driven by same store sales growth and new units opened.

Operating income has also grown at approximately 10% for the same period, from $2.2 billion in 2013 to $3.9 billion in 2019. Operating margins hovers between 14% to 18% throughout the years. We can expect operating income to grow faster than revenue going forward as management guides for long-term operating margins of 20% stemming from increasing licensed stores, repositioning traditional Starbucks stores into Starbucks pickup, and with technology driving efficiency (Starbucks App and Deep Brew).

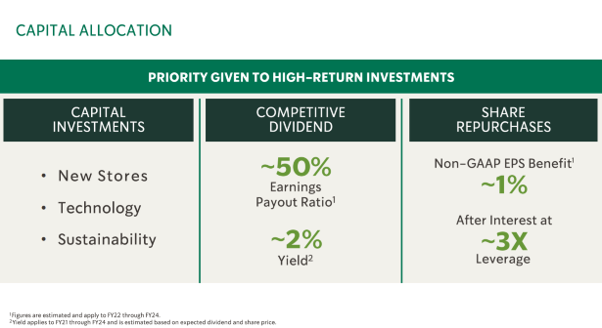

Starbucks currently has $14.6 billion worth of long-term debt, which is a sizable amount considering debt makes up half the size of its assets at $28.3 billion. It’s important to note that the company didn’t borrow because it needed the cash for operational needs, Starbucks borrowed to take advantage of the low-interest rate environment and proceeded to buy back shares aggressively.

We can’t use debt-to-equity when evaluating if Starbucks will be of sound financial standing because of its negative equity, which happens when a company aggressively buys back shares.

A better approach would be to use the Debt-to-EBITDA ratio, to find out whether Starbucks have the cash flows needed to pay down its debt. I have previously written about it here.

Generally, an investment-grade company would have a Debt to EBITDA ratio below 3. A ratio between 4 to 5 represents an elevated risk for rating agencies and creditors. Anything above 5 indicates significant financial difficulties and the strong likelihood that the company will be unable to borrow additional funds.

For Starbucks, the five-year average EBITDA is approximately $5.8 billion, with a long-term debt size of $14.6 billion, this puts the Debt-to-EBITDA ratio at a comfortable 2.5x.

Returning Capital to Shareholders

Starbucks has been extremely aggressive in share buybacks. The company spent $7.1 billion and $10.2 billion in 2018 and 2019 respectively. The company financed its share buyback program with loans, upfront fee of $7.15 billion from Nestlé and its ongoing operating cash flow.

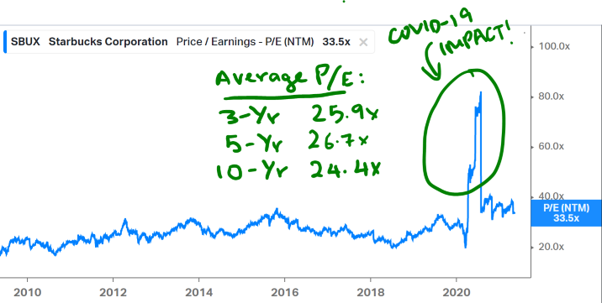

Valuations

For a company in the mature growth cycle like Starbucks, applying the P/E ratio for valuation would be apt. Ignoring the impact of COVID-19, Starbucks generally trades around 25x forward P/E.

Starbucks guided for full-year fiscal 2021 consolidated revenue to be approximately $29 billion (between $28.5 billion to $29.3 billion), for EPS growth to exceed 10% (through a combination of revenue increases and share buybacks) and for operating margin to approach 20% by 2024.

Assuming they are able to grow revenue by 8% annually for the next 5 years to reach $42.6 billion, with an operating margin of 20%, we will arrive at $8.5 billion in operating income. Let’s expense another 23% off for interest and taxes, and we will get $6.6 billion in net income.

There’s currently 1.18 billion shares outstanding as of 31 March 2021. With the company’s aggressive share repurchase program, let’s assume that share count will drop by 1% each year for the next 5 years to arrive at 1.12 billion shares.

Dividing $6.6 billion in net income with 1.12 billion shares, we will arrive at $5.9 earnings per share. Giving it an average multiple of 25x, we will arrive at $147.50.

Looking at Starbucks share price of $114 today, this is estimated to provide us with a return of approximately 7% annually (5.3% in capital appreciation, along with an additional 1.6% in dividend yield).

Personally, I require a hurdle rate of 15% in returns annually before I would consider adding on to any position. Discounting $147.50 at 15%, I would only consider adding to my position if it goes to around $80.

Another quick way to think about valuation is to look at its reinvestment rate and return on invested capital (ROIC). With a reinvestment rate of 50% and ROIC target of 30%, Starbucks will compound its intrinsic value at 15% (derived by taking 50% x 30%).

If multiples remain constant 33.5x PE (based on next twelve months earnings), investors can expect to compound their investment at 15%. But in all likelihood, the chances of the multiple shrinking over time to the historical average of 25x are much higher.

In other words, buying Starbucks at below 25x PE (NTM) will increase your chances of getting returns above 15%, while buying at above 25x PE (NTM) will bring your returns below 15%, barring any unforeseen circumstances.

Do note that this quick method of thinking about valuation doesn’t take into account dividends and the impact of share buybacks. Which will likely contribute an additional ~2% in returns yearly.

Conclusion

Starbucks is a great company and its management is doing many things right, revamping its stores, developing its digital ecosystem as consumer behaviours change. The only issue is that its valuation has gone ahead of its fundamentals and I have liquidated part of my holdings after having held it for many years. It is still a company I really like, and I will look to reestablish a position should Mr. Market become depressed again.

I have used the capital released from Starbucks and deployed them into Twilio, amongst several others growth stocks which have had a pullback recently. Just to throw it out there—even with the recent pullback for growth stocks, valuations are still sitting at historically high levels.

But when it comes to investing, multiples (i.e., valuations) matter a lot in the short run, but over the long-run, durable revenue growth is what drives your returns.

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I do not hold a position in Starbucks at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).

solid article!

Thank you! 🙂

This is an insightful and refreshing write-up!

Thank you for the kind words! Glad you like it 🙂

Great article, Thomas. When I lived in Japan, I visited the Starbucks in Shibuya nearly every time I was in the area. I have fond memories of my wife and I just sitting there, drinking coffee, and watching thousands of people a minute stroll by. At one of those moments, I realized the incredible value in Starbucks’ real estate. Much like McDonalds, it’s almost more of a real estate company than a coffee company.

Yeah absolutely, real prime real estate!

Great article Thomas I really like your in-depth analysis of the industry and company I hope you don’t mind me sharing this article with my FB investing community – Ein55 Investing Forum ?

Thanks for reading! Please feel free to share 🙂

Congratulations, Thomas!

Hi Thomas,

I was looking at the recent dip in Starbucks price to about $84.

Revisiting your previous analysis above, and also extracted the essence below:

“Giving it an average multiple of 25x, we will arrive at $147.50.”

“Personally, I require a hurdle rate of 15% in returns annually before I would consider adding on to any position.”

“Discounting $147.50 at 15%, I would only consider adding to my position if it goes to around $80.”

“It is still a company I really like, and I will look to reestablish a position should Mr. Market become depressed again. ”

Are your previous analysis/hypothesis still valid?

Or has any of the factors/data changed fundamentally since your article in Dec 2021? Appreciate your insights, thanks! 🙂

Since the report was published, there were quite a few hiccups with Starbucks. Most notably with how they dealt with unions.

While I think it still is a formidable brand, Howard Schultz has had to return again to clean up the mess. My biggest concern with the green mermaid is its succession issues. It appears that it isn’t a business that’s easy to run and Schultz has repeatedly returned to clean up the mess.