Remember when Sea Limited was almost done for?

The pandemic darling had burned through cash like there was no tomorrow. Interest rates were rising. Consumer spending was cooling. The company was shutting down operations in Argentina, Chile, Colombia, Mexico, Poland and France—retreating from markets they’d confidently entered just years before.

There was genuinely a point where Sea Limited could have run out of cash at the rate they were burning it.

Today? It’s back to playing offense. Except this time, they’re doing it without reliance on external capital.

The Comeback Story

Sea Limited is now firing on all three cylinders—digital entertainment, e-commerce, and digital financial services. More importantly, all three segments are gushing cash while their Southeast Asian competition has largely run out of breath.

Shopee: The Cash Machine

Shopee’s gross merchandise value (GMV) increased 21.5% to US$28.6 billion for Q1 2025. Gross orders kept pace, rising 20.5% year-on-year to 3.1 billion orders.

But here’s where it gets interesting.

Shopee’s revenue outpaced GMV growth, growing 28.3% year-on-year to US$3.5 billion. They increased their take-rate by 68 basis points to 12.3%.

Adjusted EBITDA came in at a strong US$264.4 million, compared to a loss of US$21.7 million a year ago. Operating leverage is coming in strong for its ecommerce arm and profitability is expected to widen.

Now, you may recall that Shopee also achieved EBITDA profitability in late 2022. But that was crisis mode—they’d shifted from growth to profitability overnight and revenue ground to a halt.

This time is different. Revenue grew 28.3% while they delivered strong profitability. That’s sustainable growth from a position of strength. Adjusted EBITDA margins rose 900 basis points to 8% for Q1 2025.

I like to look at this with a different lens—add back sales and marketing expenses to get a clearer view of the underlying business health.

From this perspective, you can see that Shopee has been a different beast since Q4 2022.

And they’re nowhere near done. Adjusted EBITDA as a percentage of GMV currently stands at 0.92%. Chris Feng, President of Sea Limited, mentioned they’re targeting 2% to 3%:

“If you look at the profit side, as a long-term trend, we’re still targeting around 2% to 3% of the EBITDA over GMV. Of course, in the short term, we are not squeezing our ecosystem as much as possible. We are still focused very much on the growth side.”

Think about that for a moment. Through a combination of rising GMV and expanding profitability, there will be a twin engine impact to Shopee’s bottom line.

Building the Moat: Logistics First

Here’s what most investors miss about e-commerce companies: logistics is critical to building a durable moat.

Anyone can start a two-sided marketplace. It’s not easy, but it’s possible. Logistics? That requires intensive capital and, more importantly, time to develop. And a good logistics capability is key to improving unit economics and customer satisfaction through speed and ease of returns.

Management shared they’ve reduced Shopee’s overall logistics cost-per-order by 6% in Asia and 21% in Brazil year-on-year. Meanwhile, they’re improving delivery times and expanding network coverage.

Notice what they’re doing with these savings? They’re passing them on to buyers rather than padding margins. That’s why value-added services revenue (mainly logistics) grew only 4% year-on-year despite massive volume increases.

They’re putting moat-building ahead of short-term numbers. Exactly what you want to see.

The Amazon Prime Playbook

The next step in their moat-building strategy? A subscription model like Amazon Prime.

In Q1 2025, they piloted Shopee VIP membership in Indonesia—their most important market. The program includes unlimited free shipping, bigger discount vouchers, and priority customer service.

CEO Forrest Li shared some encouraging early results:

“More than 1 million users subscribed as of the end of March. Members purchased more than 3x as frequently and spent more than 4x as much as regular buyers.”

With their strengthened logistics network and lower costs, unlimited free shipping becomes economically viable—something competitors are less likely to be able to replicate.

Winning the Ad Game

For merchants, Shopee continues rolling out tools like the Shopee AI Assistant and GMV Max, an optimized ad-tech solution for better audience targeting.

The results? The number of sellers spending on ad products increased 22%, and average ad spend increased 28% year-on-year.

This matters because ad revenue is highly profitable. As CFO Tony Hou noted:

“We still see there are meaningful potential for us to increase the ad take rate through both optimizing our efficiencies on the ad placement in our marketplace and also the seller adoptions. To increase seller adoptions, we both make it easier for sellers to invest in our ad but also make the efficient — the return of investment better for the sellers. So by doing all this, this will help us to increase the ad take rate. If you compare where we are right now versus the other marketplace similar to us, we still have meaningful room there. So that will help us in general on the monetization side.”

Brazil: Taking Share

In Brazil, they’re not stealing share from Mercado Libre, which remains formidable, but rather from Amazon and other players.

Management shared encouraging results:

“The pace of our user base expansion continued to outpace the market average as we gained market share, and we remain adjusted EBITDA positive. This was driven by our strong execution.”

Their execution includes expanding to serve more underserved market segments, onboarding more sellers, diversifying into higher ticket size product categories, and improving delivery speed while maintaining their logistics cost advantage.

But here’s the strategic breakdown from CFO Tony Hou on what’s driving their Brazil growth:

First, pricing advantage. “We have been a leading pricing advantage in the market. We always focus on to make sure that in our platform, the user can get the best pricing. And that has been very welcomed by our core mass user groups.”

Second, infrastructure improvements. They’ve been working extensively on SPX logistics, not only lowering costs but dramatically improving delivery times. Delivery times have shortened by 2-3 days compared to last year—a meaningful impact on user experience.

Third, urban penetration. They now offer same-day delivery in São Paulo, helping them penetrate better in cities.

Fourth, seller services. They’re starting procurement services for sellers. It’s early, but feedback has been very positive.

As Tony put it: “All this essentially help us to serve our users better, with the better pricing, with the better service and logistics with the lower shipping costs.”

The kicker? E-commerce penetration in Brazil remains relatively low even compared to Southeast Asia.

Translation: plenty of runway ahead.

From SeaMoney to Monee

The rebranding from SeaMoney to Monee may seem minor, but it’s important to view it through a marketing perspective. Just as Shopee’s catchy theme song can be irritating yet memorable, management emphasized that “Monee” is a name that is simple, cute, easy to write and pronounce, and aligns well with its sister brand, Shopee.

This rationale is 2x better than Facebook’s Meta rebrand, 10x better than Square to Block, 100x better than HBO’s Max confusion, and perhaps 1000x better than Twitter to X.

Okay, I might be getting carried away with the rebranding comparisons. But unlike most CEO ego projects, this name change actually makes sense from a marketing perspective.

Shifting Over to The Numbers

Monee delivered another incredible quarter, both in terms of growth and profitability. Revenue and adjusted EBITDA both grew more than 50% year-on-year, all while non-performing loans (NPL) remained stable at 1.1%.

The loan book grew 75% year-on-year to $5.8 billion, driven by an increase in user base. In Q1 2025 alone, they added over 4 million first-time borrowers.

On a sequential basis, revenue grew 7.3% to $787 million, with growth coming across Southeast Asia and Brazil. Strong growth across different markets diversifies their overall loan book, and because of its deep roots in local markets, it provides them with firsthand data to manage risks.

Sales and marketing spend as a percentage of revenue has remained stable, with a 430 basis point decline sequentially. Management attributes this partly to cost optimization during Q1.

We see this optimization in marketing spend flow through to adjusted EBITDA margins increasing 190 basis points sequentially.

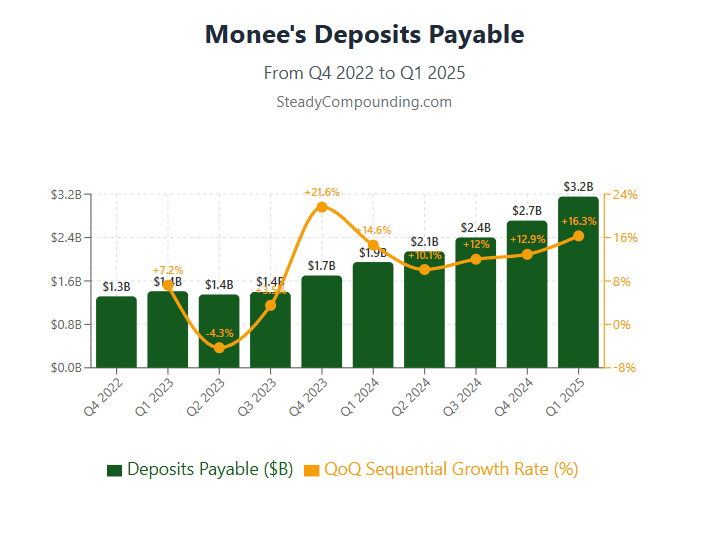

Perhaps more importantly, we’re seeing deposits grow at an accelerating pace, which generates float for the company. Deposits payable grew 16.3% sequentially to hit US$3.2 billion. And, mind you, this is in addition to the US$2.6 billion in escrow from Shopee’s operations.

When done well, the lending business is relatively straightforward, so long as the company remains prudent with its credit assessment. Despite the rapid growth, NPLs have remained stable with high profitability, so I’m happy with what the company has achieved.

Garena: The Comeback Kid

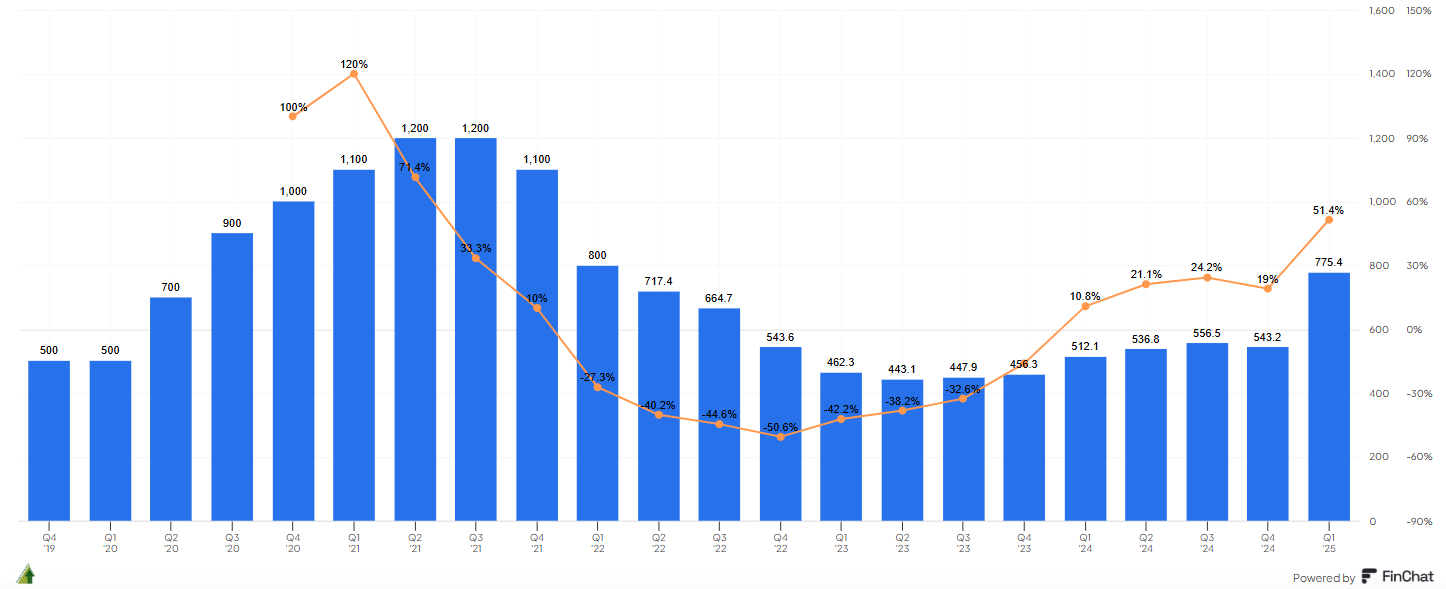

Garena bookings surged 51.4% year-on-year to US$775.4 million—a massive reacceleration not seen since pandemic days.

Garena’s Bookings (US$ Millions)

Management has usually credited growth primarily to Free Fire; however, in this quarter, they recognized a variety of other games contributing to this growth as well. This diversification is encouraging, as it reduces the reliance on a single revenue source like Free Fire.

CEO Forrest Li commented on this development:

“In addition to Free Fire, our other games, such as Arena of Valor, EA Sports FC Online, and Call of Duty: Mobile, have also had a good start in the first quarter, giving Garena a strong growth outlook for the year.”

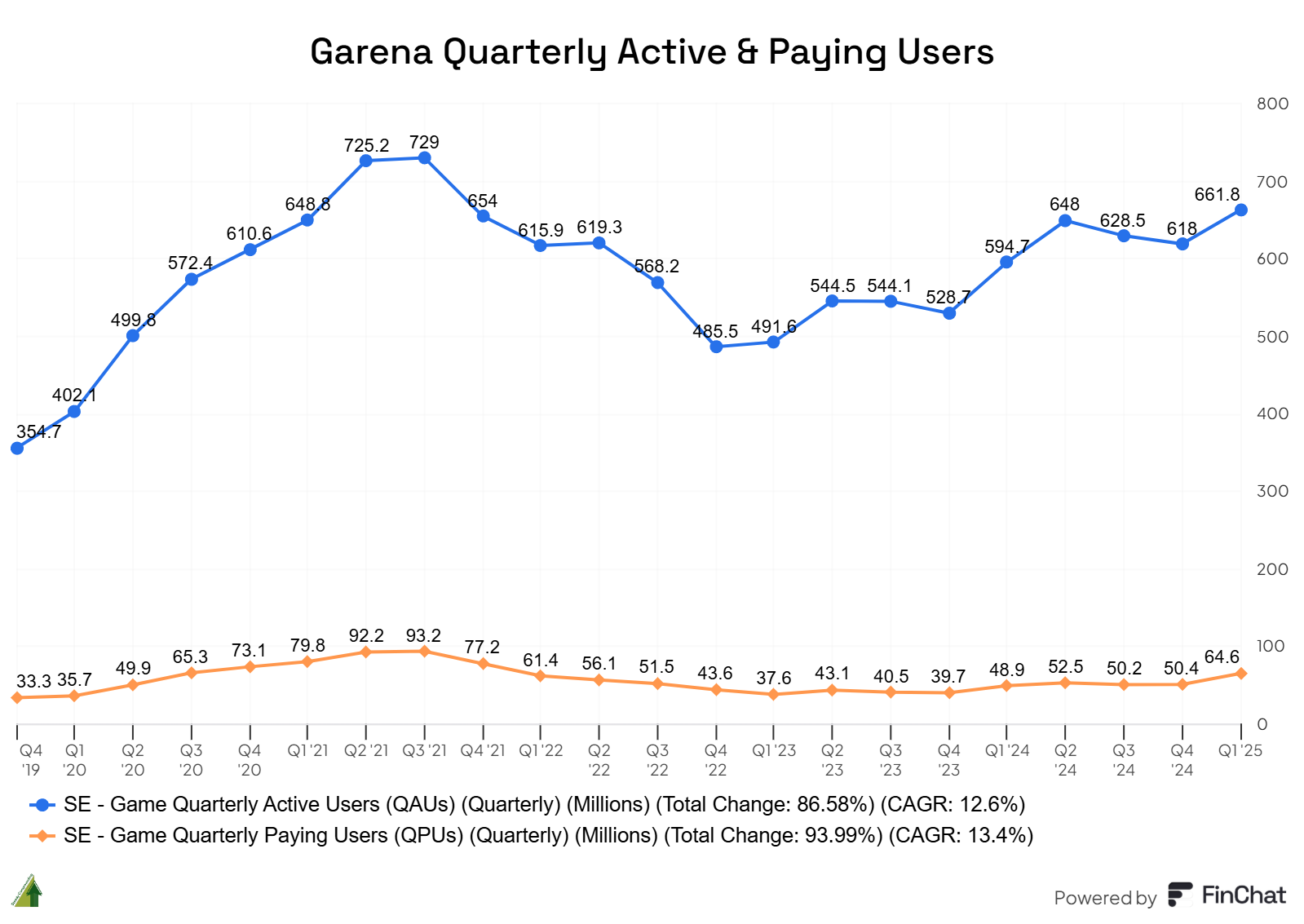

Quarterly active users increased 11.3% to 661.8 million. More importantly, quarterly paying users jumped 32.2% to 64.6 million.

The paying user ratio increased 154 basis points to 9.8%. Monetizing free players requires careful balance—you need to incentivize payments without making the experience unfair for non-paying users.

Here’s the most encouraging part: Free Fire’s average daily active users is close to pandemic levels. But this time, it’s not driven by temporary lockdown measures. It’s sustainable user acquisition. CEO Forrest L revealsi:

“Free Fire’s average DAU in the first quarter was close to its peak quarterly average DAU during the pandemic. This further reinforced Free Fire’s position as the world’s largest mobile game by average DAU and downloads, according to Sensor Tower.”

Financial Fortress

CEO Forrest Li’s opening statement says it all:

“We have delivered another great quarter of strong growth with improving profitability across all three businesses. Our businesses are now all self-sufficient and cash generating, positioning us well to capture future opportunities.”

The company now sits on $8.4 billion in cash with $1.8 billion in debt—a net cash position of $6.6 billion.

This resilient position makes them terrifying for regional competition because they can pursue growth, widen their moat and pursue profitability simultaneously.

What Keeps Me Up at Night

As competition mellows in Southeast Asia, I’m less concerned about competitive threats than during the pandemic when TikTok seemed unstoppable.

The biggest risk? Regulatory interference.

It wasn’t long ago that India’s government decided Sea Limited was a Chinese company (it’s Singaporean) and kicked them out despite heavy investments.

Indonesia is the crown jewel that worries me most. The country’s competition watchdog launched an investigation into Shopee over “monopolistic practices”—specifically because Shopee Xpress delivers faster and cheaper than domestic players.

Why is delivering better service monopolistic? I can’t explain it rationally. But this is the price of doing business in the region.

Beyond regulatory risks, Sea Limited today is in a significantly different position than during the pandemic. It no longer depends on external capital.

The Bottom Line

This marks the fourth consecutive quarter of excellence. Management is going on offense aggressively, but without sacrificing profitability this time.

As they say, age makes you wise. That near-death experience in 2022/2023 made Sea Limited a better company.

I’m happy to continue being a shareholder and let them keep executing.

Disclaimer: This research report constitutes the author’s personal views only and is for educational purposes only. It is not to be construed as financial advice in any shape or form. The author holds a position in Sea Limited at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).

Hi Thomas, other than the business aspect and growth prospects that you analysed in detail, what do you make of SEA’s current valuation , esp since SEA’s price has seen a run up recently? Thanks,

KC

Slight overvaluation range.