Admission Open: We have opened admission to our investing course for beginners. If you like to learn how to analyze and value a stock from start to finish, this course is for you! We are offering a $50 discount from now till 10 Jun, 9am. Once past that time, we will be raising the prices to at least $500.

We have all read Peter Lynch’s One Up Wall Street.

But few people know that he wrote for Worth Magazine from 1992 to 1999.

It’s a 181 page bonus scene to his best seller.

Link to his articles provided at the end of this post.

Here are my biggest takeaway:

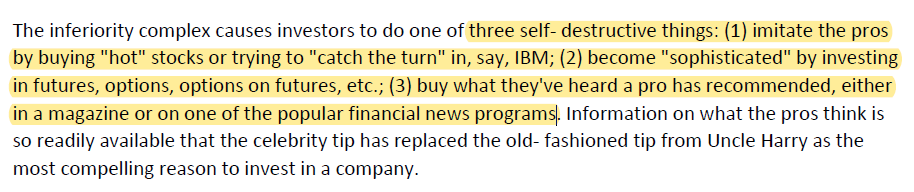

1. Retail investor feels inferior to institutions and often commit these three deadly sins

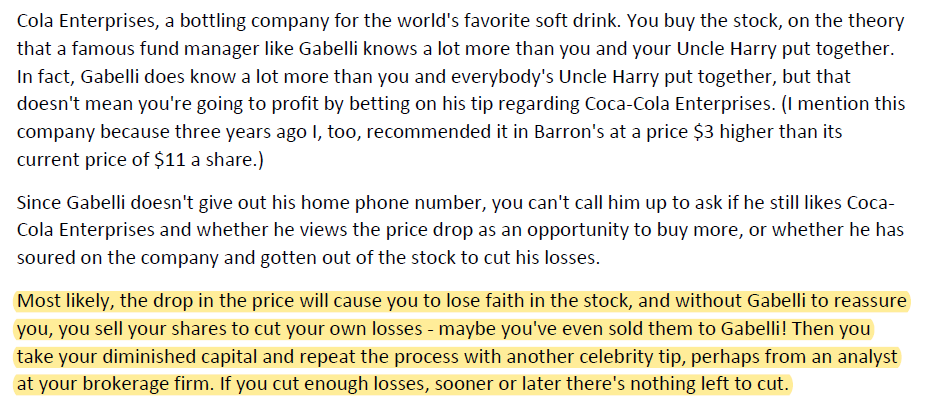

2. Why you shouldn’t buy based on an expert tip without doing your due diligence

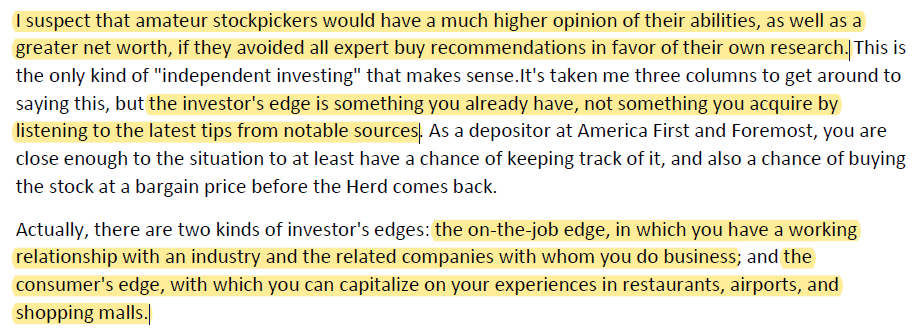

3. Ignore expert tips and favor your own research.

The retail investors’ edge:

– on-the-job edge

-consumer’s edge

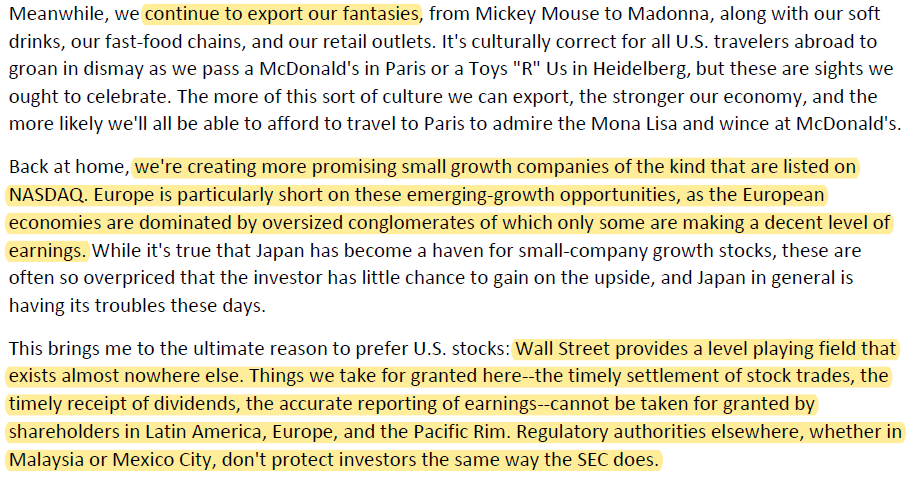

4. Why Lynch thinks that investors in the US should focus on US companies: It’s in the backyard that investors find their edge

5. Why it’s best to avoid your broker’s “hot IPO” tip.

For best deals, it’s often oversubscribed.

Even the big funds are assigned a piddling amount.

If there are left overs in a hot IPO, think about why the big investors are avoiding it.

6. IPOs often happen in waves, It usually correspond with periods when investors are euphoric.

But it might be costly, but the best companies usually get listed during times like these.

7. How to review IPO prospectuses

Compare the red herring with the final prospectus.

To gauge the enthusiasm for the IPO.

Check what are the proceeds from the IPO being used for?

a. [Ideally] Invested into the company for working capital needs, pay down debt or for expansion?

b. Go into the pockets of the founders and directors who are selling their shares?

Other stuff Lynch look for in an restaurant company’s IPO:

-Is the growth plan well-articulated? -Sales and earning increasing?

-Annual sales should exceed the cost of construction

-Is revenue heavily reliant on alcohol sales? Liquor tastes the same everywhere, there’s no moat if it’s reliant on alcohol.

8. There’ll always be something to worry about.

That nagging doubt that the company may not have staying power.

As a result, we miss many of the best home runs.

“The trick is to put your fears to rest by doing the research and checking the facts.”

9. Three lessons on biotech investments

10. You don’t have to invest in companies that are in its early stage.

Even during the late innings, you can make great returns.

11. When the entire biotech industry is down, look for:

-Companies with share values close to their cash holdings

-Limit the search to companies that already have drugs on the market

-Have revenue

12. The pan-and-shovel technique

Whenever there’s a mania, look for supplier who provides them with all the tools they need.

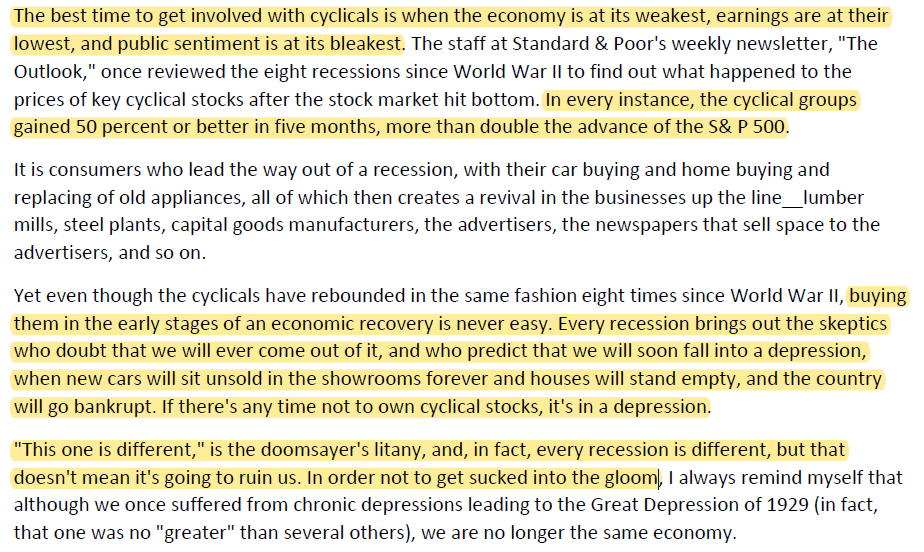

13. The best time to invest in cyclicals is when the economy is at its weakest.

Even though investing in cyclicals has provided predictable results, it is never easy.

Because the sirens of pessimism would be the loudest during times like this.

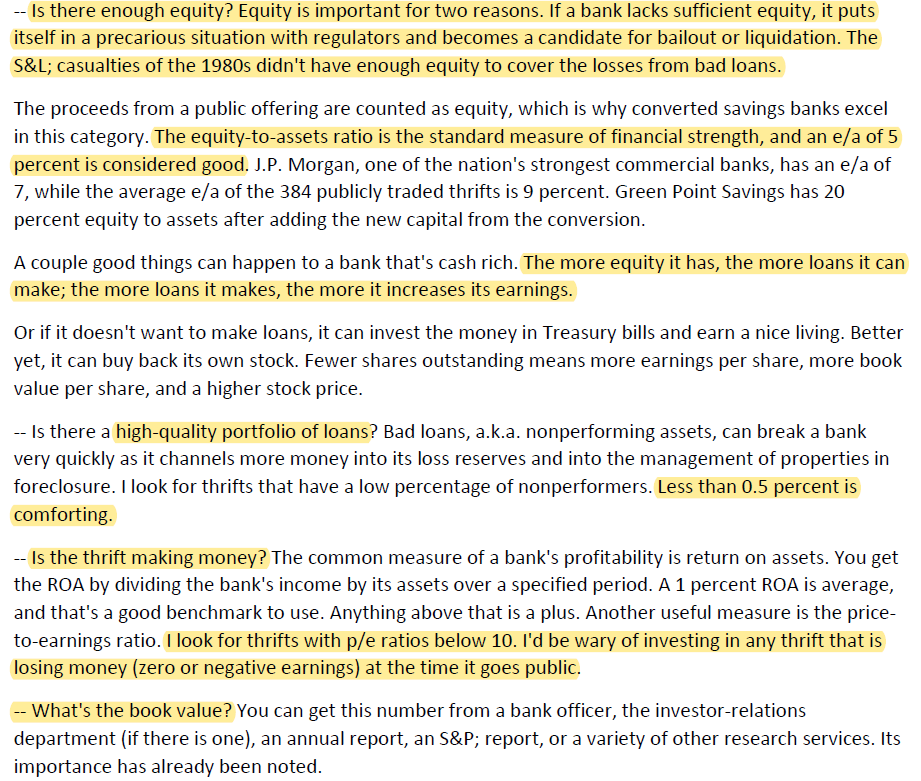

14. When investing in distressed banks, check:

-Enough equity? Equity-to-assets > 5% is good.

-High-quality portfolio of loans? Less than 0.5% is good.

-Is it profitable? ROA > 1% and P/E < 10 -Book value?

-Does it have real estate?

-Cheap deposits? Low number of clients but with large deposits have lower maintenance costs.

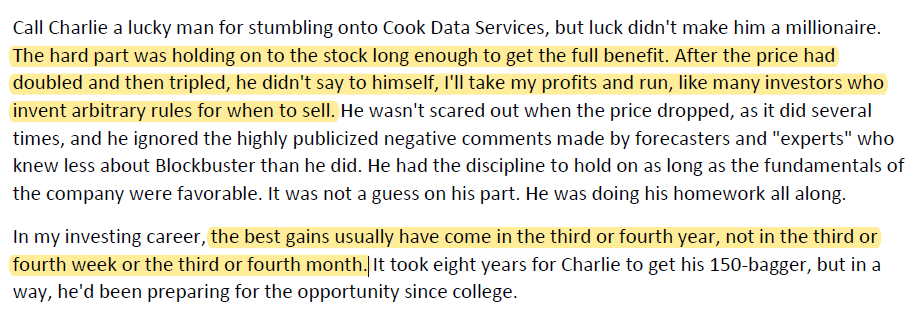

15. The hardest thing about getting a multi-bagger isn’t hunting for one, it’s the holding.

Not taking quick profits.

Not selling on drawdowns.

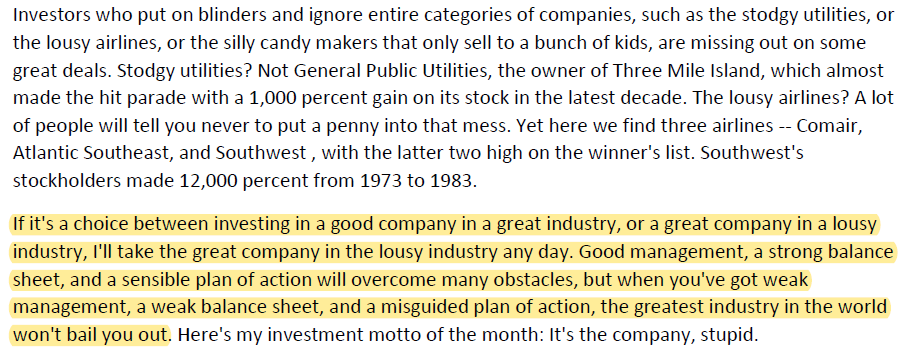

16. It’s the company, stupid.

17. When investing in turnarounds:

-Figure out if it’s going to survive long enough to turn

-Is it a temporary misfortune or secular decline?

-Be patient

You can download the complete set of PDF articles here: Peter Lynch’s Articles for Worth Magazine

Enjoyed Peter Lynch’s investing insights?