Sir Chris Hohn manages over $50 billion at TCI Fund Management with an approach that seems almost antiquated in today’s markets: he holds stocks for an average of 8 years. The market average? Less than one.

In a recent conversation with Simon Brewer at the Money Maze Allocator Summit, Hohn revealed the philosophy behind this patience – and why most investors are playing the wrong game entirely.

Risk Is Not Knowing What You’re Doing

“Investing is all about risk and return, and the vast majority of investors focus on return,” Hohn explains. “But I focused actually in my career on risk firstly.”

His definition of risk, borrowed from George Soros, is brilliantly simple: not knowing what you’re doing. This isn’t about volatility or beta – it’s about understanding what truly matters in a business.

For Hohn, what matters boils down to competitive dynamics and disruption potential. “The fact of the matter is that most investors underestimate the forces of competition and disruption because they underestimate complexity. They look short-term.”

The Persistence of Quality

Perhaps Hohn’s most powerful insight is the persistence of quality. “Good companies stay good and bad companies stay bad,” he states matter-of-factly.

This observation drives TCI’s extraordinary holding periods. “Our average holding period of a stock in our portfolio is 8 years. We’ve held stocks for 13 years, 12 years, and 10 years.”

The logic is compelling: “There aren’t that many great companies, the super companies of the world. If you find them, you should hold on to them.”

Multiple Barriers: The Fortress Principle

One competitive advantage isn’t enough for Hohn. He wants multiple, overlapping barriers to entry:

“Often you would like not just one barrier to entry but maybe five: intellectual property, brands, hard assets, contracts, network effects. Big jet engines and aircraft engines have many of those—IP, contracts, installed base, regulatory switching costs.”

His examples are instructive. Spanish airports: “No one’s ever going to rebuild those.” Toll roads with 100-year durations: “We don’t know whether people are going to drive electric cars or which brand, but it’s pretty clear they’re going to need these roads.”

The Obviousness Test

If a competitive advantage requires a complex explanation, Hohn isn’t interested.

“You really want something that’s obvious. Warren Buffett used to talk about this. If it’s not obvious, you probably just leave it alone because it’s probably not sustainable.”

This filters out most of what the market finds exciting. “Technologies that change quickly aren’t good for us—we can’t predict them.” Instead, he focuses on essential services with predictable demand over decades.

Pricing Power: The Holy Grail

While most companies avoid discussing pricing power, Hohn sees it as the ultimate proof of competitive strength:

“If you really do find one of these super companies that can dominate their industries, they have something special, which is pricing power—a rare thing. Most companies don’t like to talk about it.”

The mathematics are compelling: “If you have a 10% margin, every one point of real pricing is massive. It’s super leveraged and potent.”

The Danger of “New”

When asked what excites him about the investing landscape, Hohn’s response is characteristically contrarian:

“Sometimes people—your very question illustrates what most investors are looking for: the next hot thing, the new thing. Sometimes I’ll say, a little bit sarcastically, ‘Do you want to invest in what’s new? Do you need to change your wife every year?'”

His point is profound: “It’s not that easy to find the right investment. So why do you want to change them immediately?”

Peloton’s collapse from a $50 billion valuation to nearly zero exemplifies this principle. “I think the most important question is: what’s going to be around, rather than what’s new.”

The Weight of Time

Hohn’s philosophy ultimately rests on Benjamin Graham’s famous observation: “In the short term the market is a voting machine—what’s hot, what’s new—but in the long term it’s a weighing machine.”

By extending his time horizon to 20-30 years, Hohn plays a different game than most investors. He’s not trying to predict next quarter’s earnings or catch the next trend. He’s identifying businesses with such strong competitive positions that their dominance is obvious and enduring.

The approach seems simple: Find companies with multiple barriers to entry in essential industries, then hold them for decades. But simple doesn’t mean easy. It requires the discipline to ignore the market’s daily noise, the courage to appear wrong for extended periods, and the wisdom to distinguish between what changes and what endures.

In a market obsessed with the new and disruptive, Hohn’s success suggests that sometimes the best investment strategy is simply recognizing what won’t change.

What’s your favorite insight from Sir Chris Hohn? Let me know in the comments below.

Watch the interview here:

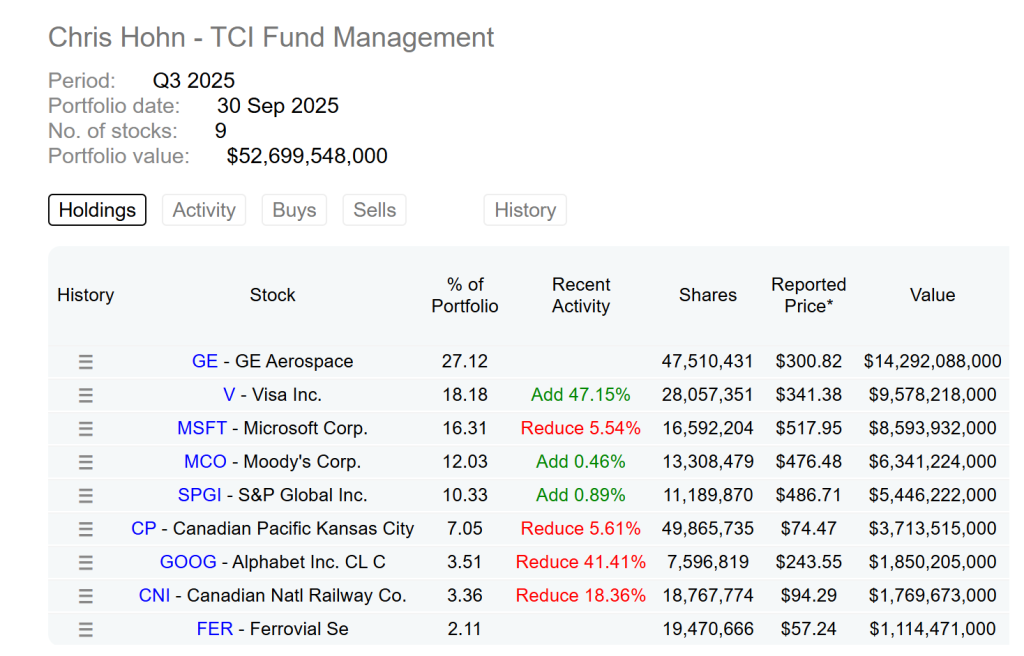

P.S. For the curious, this is Chris Hohn’s current portfolio: