The latest Warren Buffett shareholder letter is up!

In this letter for FY 2022, he discussed:

• Insurance float

• Share buybacks

• Choosing partners

• Coca-Cola & Amex

• Imaginative accounting

• His criteria for businesses

& more!

Here are my notes:

Nothing beats having a great partner

Charlie Munger played a huge role in the success of Berkshire Hathaway.

Here’s Buffett’s rule for finding a partner:

“Find a very smart high-grade partner – preferably slightly older than you – and then listen very carefully to what he says.”

And he included a list of his favorite Munger quotes:

• The world is full of foolish gamblers, and they will not do as well as the patient investor.

• If you don’t see the world the way it is, it’s like judging something through a distorted lens.

• All I want to know is where I’m going to die, so I’ll never go there. And a related thought:

Early on, write your desired obituary – and then behave accordingly.

• If you don’t care whether you are rational or not, you won’t work on it. Then you will stay

irrational and get lousy results.

• Patience can be learned. Having a long attention span and the ability to concentrate on one thing for a long time is a huge advantage.

• You can learn a lot from dead people. Read of the deceased you admire and detest.

• Don’t bail away in a sinking boat if you can swim to one that is seaworthy.

• A great company keeps working after you are not; a mediocre company won’t do that.

• Warren and I don’t focus on the froth of the market. We seek out good long-term

investments and stubbornly hold them for a long time.

• Ben Graham said, “Day to day, the stock market is a voting machine; in the long term it’s

a weighing machine.” If you keep making something more valuable, then some wise person is going to notice it and start buying.

• There is no such thing as a 100% sure thing when investing. Thus, the use of leverage is

dangerous. A string of wonderful numbers times zero will always equal zero. Don’t count

on getting rich twice.

• You don’t, however, need to own a lot of things in order to get rich.

• You have to keep learning if you want to become a great investor. When the world changes, you must change.

• Warren and I hated railroad stocks for decades, but the world changed and finally the country had four huge railroads of vital importance to the American economy. We were slow to recognize the change, but better late than never.

• Finally, I will add two short sentences by Charlie that have been his decision-clinchers for decades: “Warren, think more about it. You’re smart and I’m right.”

There’re 2 main forms of ownership for Berkshire:

1. Buy a 100% stake in businesses

2. Invest in public markets (i.e. stocks)

In the former, Buffett directs capital while the CEO handles day-to-day operations.

And for this to work on a large scale, trust and rules are essential.

“When large enterprises are being managed, both trust and rules are essential. Berkshire emphasizes the former to an unusual – some would say extreme – degree. Disappointments are inevitable. We are understanding about business mistakes; our tolerance for personal misconduct is zero.

The businesses Warren is looking for…

Goal for ownership is to own businesses with:

1. Long-lasting favorable economic characteristics

2. Trustworthy managers

Long-term business performance is always more important than short-term share price movements.

“Charlie & I are not stock-pickers; we are business-pickers.”

Efficient markets exists only in textbooks

When it comes to investing in the public markets…

The good news is that wonderful businesses occasionally come at wonderful prices.

Like Buffett says, the trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot.

“One advantage of our publicly-traded segment is that – episodically – it becomes easy to buy pieces of wonderful businesses at wonderful prices. It’s crucial to understand that stocks often trade at truly foolish prices, both high and low. “Efficient” markets exist only in textbooks. In truth, marketable stocks and bonds are baffling, their behavior usually understandable only in retrospect.”

Sit on your ass investing

Buffett’s emphasis on companies that can grow for a long time and has a wide moat is the secret sauce to Berkshire Hathaway’s success.

In 1994, Buffett purchased 400m of Coca-Cola shares at $1.3b.

In 2022 alone, it issued $704m in dividends.

Growth occurred annually.

Buffett just sits on his ass.

“The cash dividend we received from Coke in 1994 was $75 million. By 2022, the dividend had increased to $704 million. Growth occurred every year, just as certain as birthdays. All Charlie and I were required to do was cash Coke’s quarterly dividend checks. We expect that those checks are highly likely to grow.”

Likewise with his Amex investment.

Buffett purchased $1.3b of Amex in 1995.

And dividends received have grown from $41m to $302m.

The dividends growth brings with them important gains in stock prices.

Not all your investments will be winners

And that’s ok.

But you want to structure your portfolio in a way that doesn’t wipe you out when you are wrong (i.e. no leverage or overconcentration).

“These dividend gains, though pleasing, are far from spectacular. But they bring with them

important gains in stock prices. At year end, our Coke investment was valued at $25 billion while Amex was recorded at $22 billion. Each holding now accounts for roughly 5% of Berkshire’s net worth, akin to its weighting long ago.

Assume, for a moment, I had made a similarly-sized investment mistake in the 1990s, one

that flat-lined and simply retained its $1.3 billion value in 2022. (An example would be a

high-grade 30-year bond.) That disappointing investment would now represent an insignificant 0.3% of Berkshire’s net worth and would be delivering to us an unchanged $80 million or so of annual income.

The lesson for investors: The weeds wither away in significance as the flowers bloom.

Over time, it takes just a few winners to work wonders. And, yes, it helps to start early and live into your 90s as well.”

Focus on the underlying business

In investing, focus on the earnings that are most closely related to the performance of the business.

For Berkshire, it’s GAAP income exclusive of capital gains or losses from equity holdings.

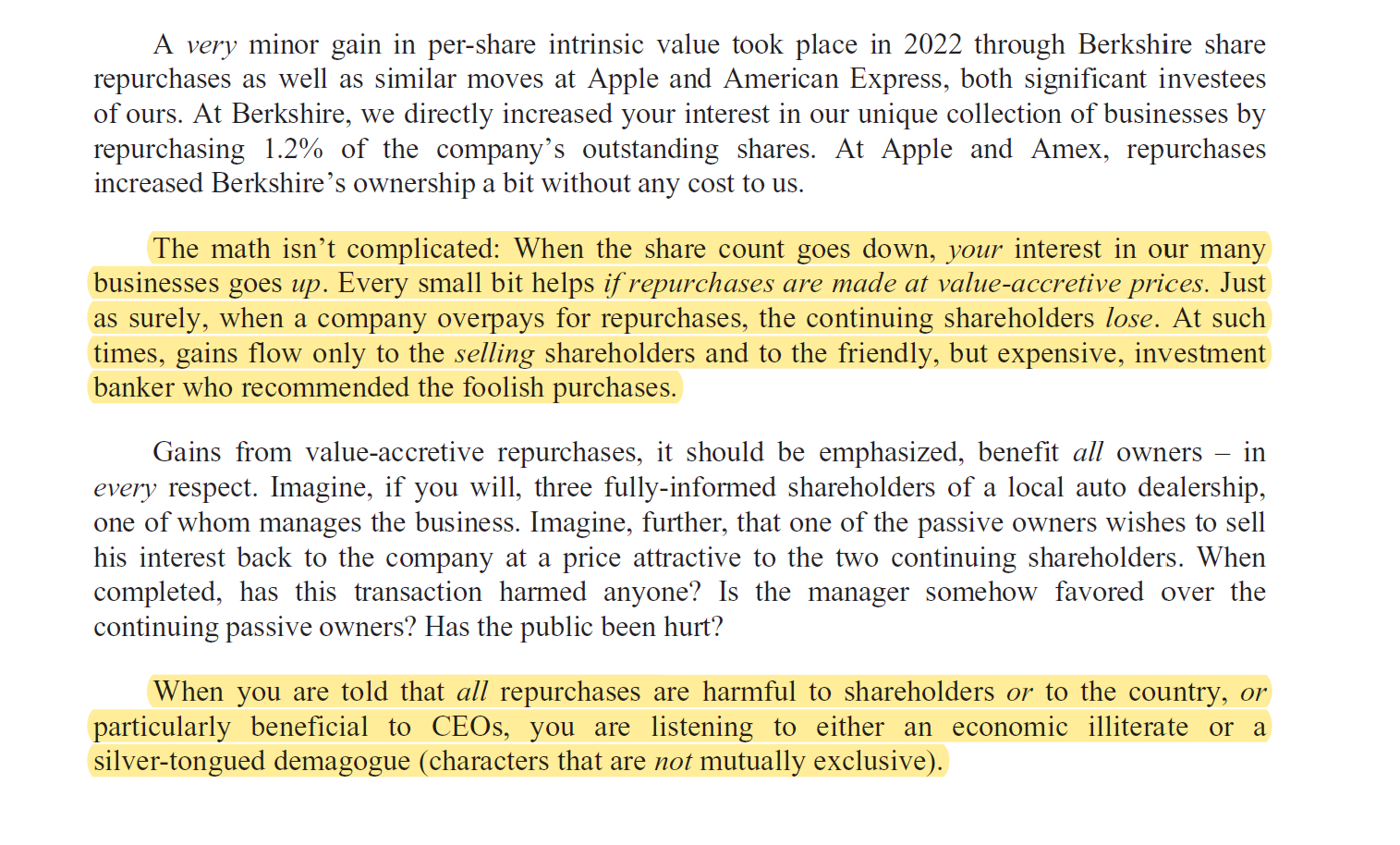

Share buybacks: good or evil?

Share buybacks when done at value-accretive prices, benefits everybody.

Especially continuing shareholders.

And here Warren took a dig at the other Warren.

Check out the last paragraph of this screengrab 👇

A warning from Buffett:

Even GAAP operating earnings can be manipulated.

These bold imaginative accounting are disgusting.

“Finally, an important warning: Even the operating earnings figure that we favor can easily be manipulated by managers who wish to do so. Such tampering is often thought of as sophisticated by CEOs, directors and their advisors. Reporters and analysts embrace its existence as well.

Beating “expectations” is heralded as a managerial triumph. That activity is disgusting. It requires no talent to manipulate numbers: Only a deep desire to deceive is required. “Bold imaginative accounting,” as a CEO once described his deception to me, has become one of the shames of capitalism.”

Never put yourself in a position of potential financial ruin

Take Buffett’s lead and run your personal finances like he does with Berkshire. Bullet-proof yourself financially by:

– Emergency funds

– Don’t borrow to invest

– Keep your expenses low

“As for the future, Berkshire will always hold a boatload of cash and U.S. Treasury bills

along with a wide array of businesses. We will also avoid behavior that could result in any uncomfortable cash needs at inconvenient times, including financial panics and unprecedented insurance losses. Our CEO will always be the Chief Risk Officer – a task it is irresponsible to delegate.”

Ignore forecasts

Instead, focus on what’s knowable and controllable.

“Though economists, politicians and many of the public have opinions about the

consequences of that huge imbalance, Charlie and I plead ignorance and firmly believe that near-term economic and market forecasts are worse than useless. Our job is to manage Berkshire’s operations and finances in a manner that will achieve an acceptable result over time and that will preserve the company’s unmatched staying power when financial panics or severe worldwide recessions occur. Berkshire also offers some modest protection from runaway inflation, but this attribute is far from perfect. Huge and entrenched fiscal deficits have consequences.”

Peanut brittle key to longevity?

Buffett ends off his letter with marketing for See’s peanut brittle and chocolates.

Claiming they’re nourishing and promising longevity.

I have my doubts but who am I to argue against a 92 and 99 years old?

I’ll be heading to the Berkshire AGM this year and I’m looking forward to it!

Very nice summation of Annual report. Would have liked more info on what changes are being made at Gieco. Was surprised that one page was missing that being a listing of BRK’s current holdings with purchase price and year end price. First time I believe it has not been posted. Tjhe teo oldsters are unbelivable. I doubt they will ever be replicated.