I’ve been writing about Google’s AI transition for two years now.

In May 2024, when AI doom-mongering was building, I argued in “Alphabet in the AI Era” that Google’s moat was bigger than people gave it credit for. By March 2025, with sentiment at its lowest, I doubled down in “Why It’s Premature to Cancel Google Search.” Every quarter since has added evidence to the same thesis: AI isn’t zero-sum for Google.

Q1 2026 closes the loop. Five consecutive quarters of Search acceleration, Cloud at 63% growth with 32.9% margins, a $462 billion backlog that nearly doubled in a single quarter. The debate is over as a serious investment question.

Which means my job has changed. The interesting question is no longer whether Google adapts. It’s whether the current stock price has already priced in the next two years of that adaptation. By the end of this piece, I’ll tell you what I’m doing about it in my own portfolio. Let’s walk through the quarter.

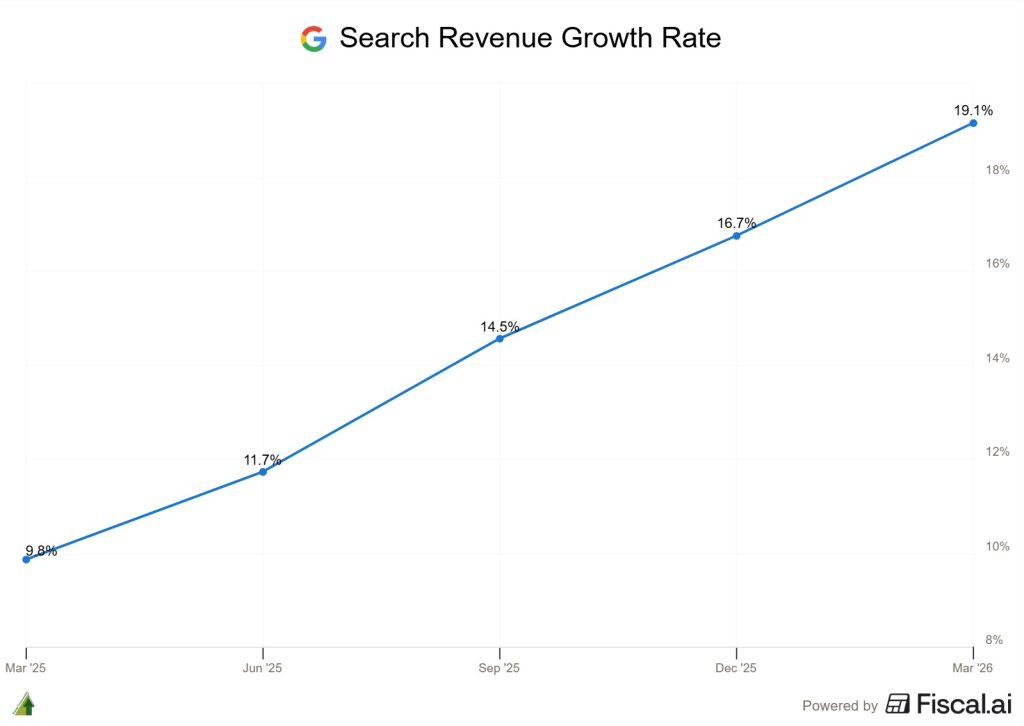

Search: Five Consecutive Quarters of Acceleration

Search & Other revenue grew 19% to $60.4 billion. Here’s the trajectory:

Source: Fiscal AI (get a 15% discount using this link)

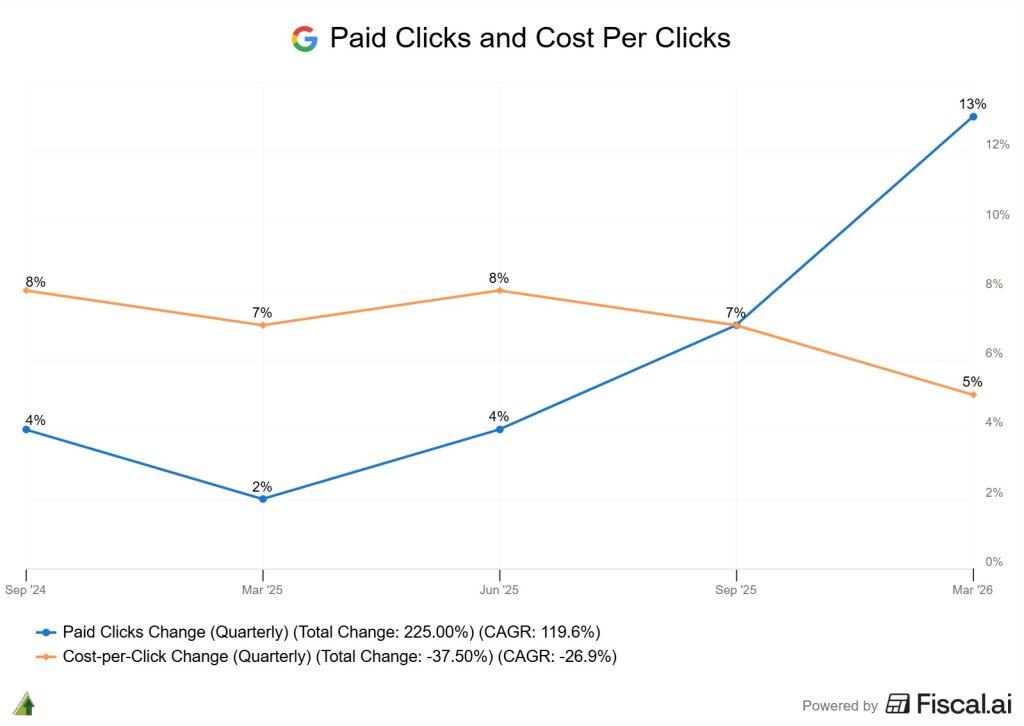

The bear thesis said AI would cannibalize Search through zero-click answers. The data says the opposite: paid clicks are accelerating, not collapsing.

Paid clicks grew 13% year-over-year and cost-per-click grew 5%. In other words, there’s more clicks and each click is bringing in more revenue. Rather than clicks cratering due to AI overviews answering questions in-line, click volume is accelerating.

Source: Fiscal AI (get a 15% discount using this link)

In the past quarters, growth between paid clicks and cost per clicks were pretty balance. But in Q1 2026, the mix tilted sharply toward volume (+13% clicks vs +5% CPC). Which suggests that AI Mode and AI Overviews are expanding query volume faster than they’re expanding pricing power, exactly what you’d expect from a “growing the pie” thesis where previously unmonetizable queries are now monetizable.

A little about the improving unit economics… Pichai shared on the call that Google has reduced the cost of core AI responses by more than 30% since upgrading AI Overviews and AI Mode to Gemini 3. That’s on top of a 35% reduction in Search latency over five years. Cost per query is falling while revenue per query is rising.

Google Services operating margin reached 45.3%, up from 42.3% a year ago. That’s 300 basis points of expansion on an $89.6 billion revenue base.

A few customer examples from the transcript that ground the abstraction:

- Hilton EMEA, using AI Max, captured one third more clicks for a fifth of the spend, while increasing average booking value by 55%

- Etsy saw a 10% Search volume uplift, with 15% of those queries net new to their business

- More than 30% of customers’ Search spend now runs through AI-enabled campaigns (AI Max or Performance Max)

Philipp Schindler, Google’s Chief Business Officer, said the company’s ability to deliver ads on longer, more complex searches that were “previously really difficult to monetize” has expanded. Queries that used to be unmonetizable now are. That’s the AI-as-pie-expansion thesis showing up directly in the numbers.

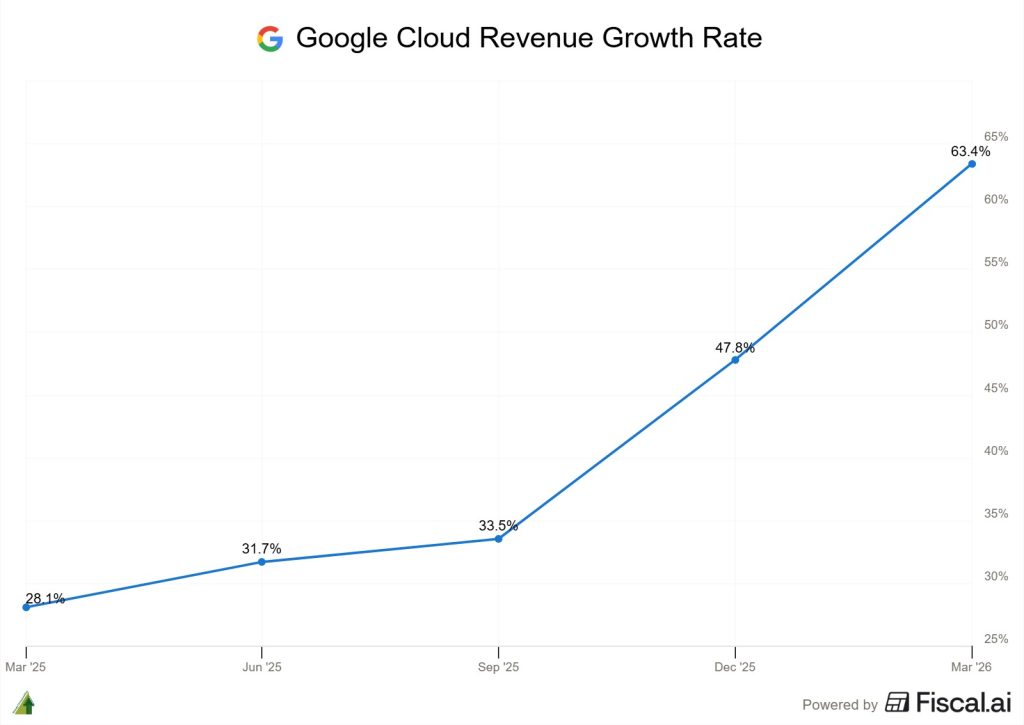

Google Cloud: Gaining Rapid Market Share

In Q1 2026, revenue grew 63% to $20.0 billion. The acceleration:

Source: Fiscal AI (get a 15% discount using this link)

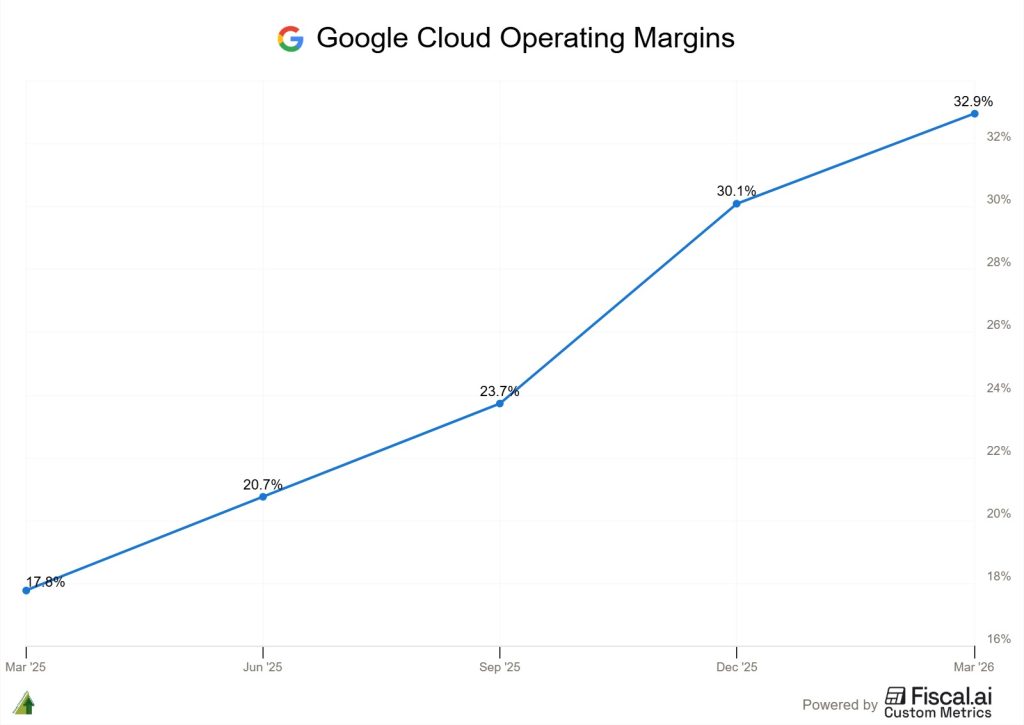

Operating income tripled to $6.6 billion. Operating margin hit 32.9%, up from 17.8% a year ago. That’s 1,510 basis points of margin expansion in twelve months. For context, AWS operates in the mid-30s.

Source: Fiscal AI (get a 15% discount using this link)

Backlog hit $462 billion, up from $240 billion in Q4 2025. Nearly doubled in one quarter. CFO Anat said just over half of that backlog converts to revenue in the next 24 months.

And for the first time, Google Cloud surpassed AWS in incremental quarter-over-quarter revenue growth in Q1 2026. In absolute dollar terms, Google added more new cloud revenue this quarter than number one player Amazon did.

Some insights about customer growth momentum from the earnings call:

- New customer acquisition doubled year-over-year

- $100M to $1B deals doubled year-over-year, plus multiple billion-dollar-plus deals

- Existing customers outpaced initial commitments by 45%, accelerating from 30% last quarter

- 330 customers processed over 1 trillion tokens in the past 12 months. 35 hit 10 trillion

- Revenue from products built on Google’s generative AI models grew nearly 800% year-over-year, up from 400% in Q4

Also, Google is now selling TPU hardware directly to customers for use in their own data centers. Until now, TPUs were exclusively available through Google Cloud rental. This will make revenue lumpy from quarter to quarter depending on shipment timing, with most of it landing in 2027.

If things go well, this could potentially unlock another market for Alphabet.

YouTube: Trading Ads for Subscription Revenue?

YouTube ads grew 11% to $9.9 billion. It didn’t see the acceleration like Google Search and GCP, but decent results nonetheless.

YouTube subscriptions revenue rolls up into Subscriptions, Platforms & Devices, which grew 19% to $12.4 billion. Pichai noted that YouTube Music and Premium had its largest quarterly increase in non-trial subscribers since the product launched in June 2018.

The subscription growth is good revenue, but it creates a challenge for YouTube’s ad business. When users opt into Premium, their impressions leave the ad supply pool entirely. And Premium users have heavier YouTube usage, including listening, Shorts, and live streams. These users are the ones most valuable to advertisers, and are exactly the segment opting out. As Premium grows, YouTube’s remaining ad supply skews toward more casual viewers.

With lesser supply, it affects targeting capabilities, which probably explains why YouTube ads are a lot more annoying intrusive than Instagram ads. And YouTube’s response to its shrinking ad supply has been to extract more from each remaining impression, in other words, flood more ads.

Which in turn pushes more viewers to Premium, shrinking the ad pool further. It’s not necessarily a bad outcome, but it is a business decision, one that perhaps will make YouTube’s revenue less cyclical than if it were to rely on ad revenue.

Financials: What the Headline Numbers Reveal

Total revenue $109.9 billion, up 22% reported and 19% constant currency. Eleventh consecutive quarter of double-digit growth. Operating income $39.7 billion, up 30%. Operating margin 36.1%, up 220 basis points and the highest in Alphabet’s history.

Net income up 81% to $62.6 billion. EPS $5.11, up 82%. Ignore these. $2.35 of the EPS came from a $36.9 billion equity gain that won’t repeat. Strip it out and operating EPS grew 26%. Operating income up 30% is the cleanest read.

Operating cash flow was $45.8 billion in Q1, free cash flow only $10.1 billion. CapEx of $35.7 billion ate the rest. Trailing twelve months OCF was $174.4 billion against projected 2026 CapEx of $180-190 billion. For the first time, Alphabet can’t fund its capital spending from internal cash. Hence the $31.1 billion in senior unsecured notes issued during Q1.

One other thing from the call: Pichai said “our Cloud revenue would have been higher if we were able to meet the demand.” That’s why they’re pouring heavily into CapEx.

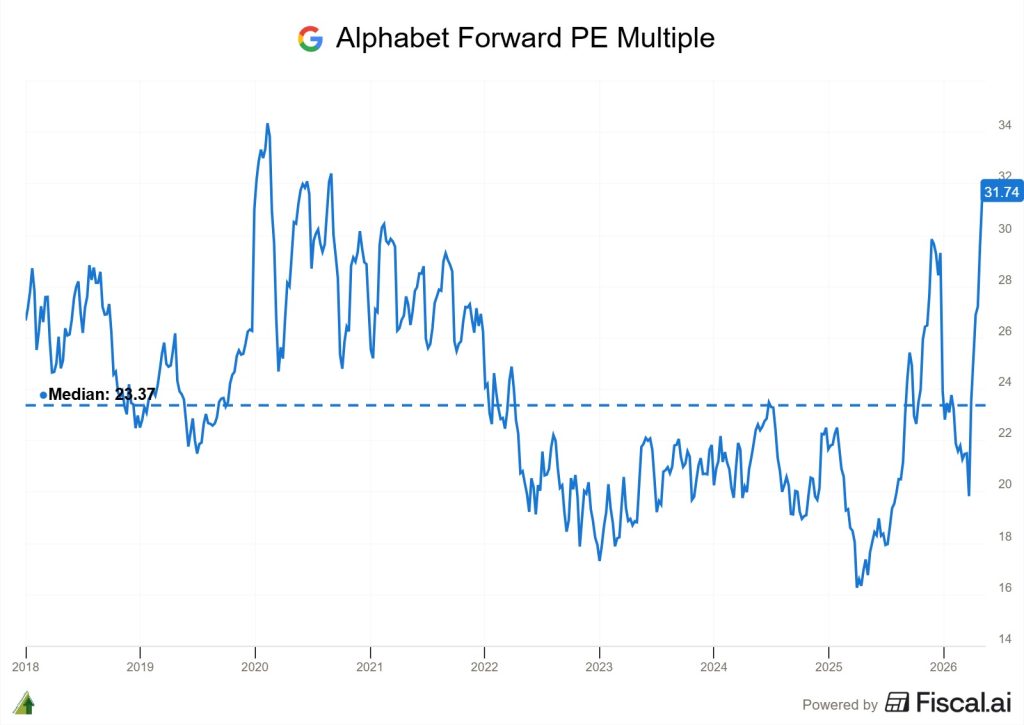

Valuation: No Longer Cheap

When I wrote “Why It’s Premature to Cancel Google Search” in March 2025, Alphabet traded at roughly 18-19x forward earnings. The stock was cheap.

Today, Alphabet trades at approximately 32x forward earnings, significantly higher than its median of 23x. At this multiple, the bull case requires continued great execution. The bear case is multiple compression as depreciation steps up in 2027-2028… or perhaps, the fickle Mr. Market decides that Search is once again under threat.

Source: Fiscal AI (get a 15% discount using this link)

What I’m Doing: Sitting on My Hands

I’m not going to add at today’s price, but I’m not going to sell either. I’m going to do the most difficult thing in investing… sitting and not doing anything… unless valuations become egregious.

Sentiment was my margin of safety in March 2025. There is no margin of safety in sentiment today, so I’m not adding. But selling our winners when they perform well is a sure way to end up with a bunch of mediocre companies in our portfolio.

I’d revisit the decision if it becomes too big a position in my portfolio (> 15%) or if valuations become too egregious.

Closing

Two years ago, this was the contrarian call. People thought AI would kill Google. I argued it would expand the business. Q1 2026 closes the debate.

The landscape is evolving fast, but so far, Google has proved adaptable. I’m still long. Sometimes the right move is no move.

Disclaimer: This research report constitutes the author’s personal views only and is for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure: I hold a position in Alphabet at the time of publishing this article. This is a disclosure and NOT A RECOMMENDATION.