It’s wild to think that a year ago, Netflix’s share price dropped as low as $164.28. That was when Bill Ackman sold his 7% stake in Netflix, at a loss of about $400m. In his letter to investors, he explained:

“While we have a high regard for Netflix’s management and the remarkable company they have built, in light of the enormous operating leverage inherent in the company’s business model, changes in the company’s future subscriber growth can have an outsized impact on our estimate of intrinsic value,”

It was then that Netflix was coming off a huge COVID boost in subscribers and had a decline in subscribers as the economy reopened and more streaming players entered the fray.

The rapid growth of Disney+ attracted a lot of attention. They were throwing up huge numbers, but I explained how they didn’t compare to Netflix’s numbers because the Disney+ numbers were misleading. In summary, Disney+ charged peanuts (peanuts might have cost more) in India and a lot of subscribers churned as they raised prices and lost the rights to stream the India Premier League (Cricket).

You can read the article here: https://steadycompounding.com/investing/disney-overtook-netflix/

In another article, I explained why Netflix is likely to prevail over its competitors despite the share price tumbling. If Netflix, who has the largest content library and is already profitable and cash flow positive, would suffer in this environment, then the other smaller players would suffer and bleed.

You can read the article here: https://steadycompounding.com/investing/netflix-down-after-hours/

Recovering from the blip

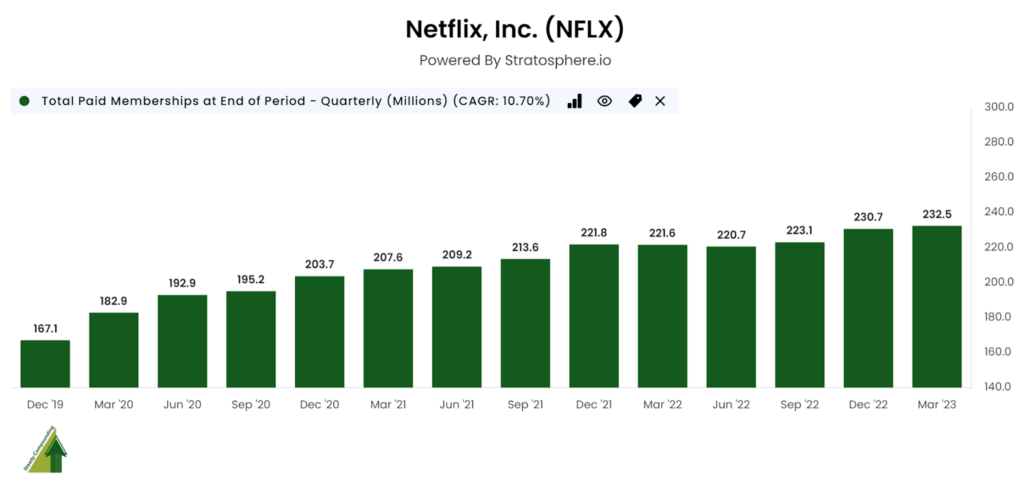

Fast forward to today, it turns out the drop in subscriber numbers was temporary, and the company has gone on to achieve an all time high in paid subscribers at 232.5m. Its share price has since more than doubled to $362 as of 21 May 2023.

Let’s dive into what the company has done right and what caused the narrative to change (once again).

Quality of content

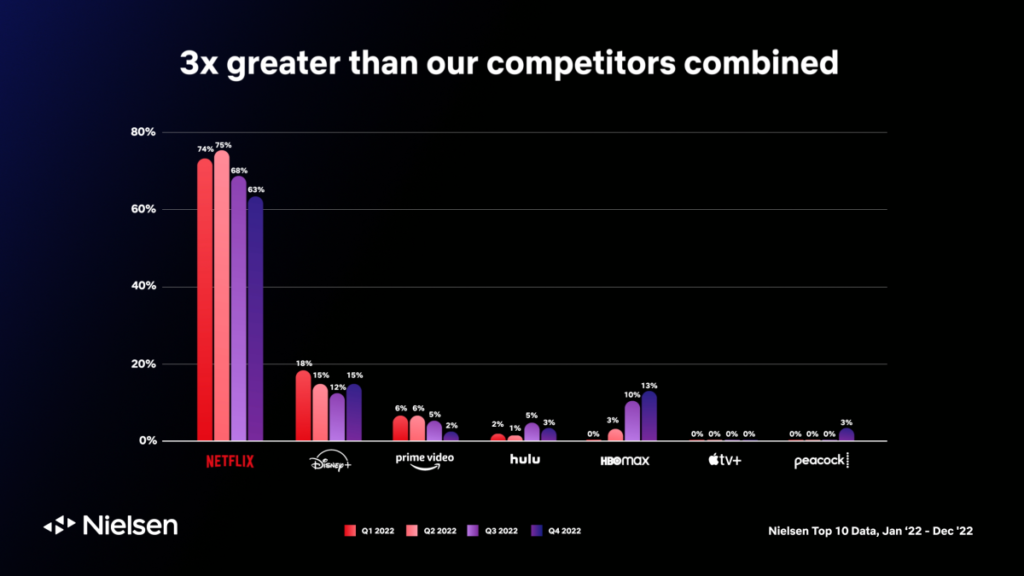

When we look at the quality of content being put out, Netflix viewing across Nielsen’s Top 10 most watched lists was three times greater than all its competitors combined — and five times greater than its nearest competitor.

Crackdown on password sharing

During this quarter, the company piloted cutting off password sharing in Latin America (LATAM) and Canada with positive results.

The average revenue per membership for UCAN has grown 9% from $14.91 to $16.17, and for LATAM it has increased 3% from $8.37 to $8.60. At first, management reported cancellation reactions, but that subsequently eased.

There was a drop of 0.45m paid members in LATAM, but revenue was up 7% YoY (13% in constant currency).

Similar patterns were observed for Canada as well. UCAN reported 0.1m net additions, but revenue was up 8%.

This quarter will see a broader rollout, which will lift revenue and cause temporary increases in churn (member cancellations).

Advertising tier

The ability of Netflix to adapt to changing consumer behavior is one of their strongest traits. Reed Hastings has publicly stated that Netflix will never introduce an advertisement tier.

After seeing that Hulu proved the ad-tier model scaled and offered customers lower prices, he acknowledged that he was wrong, that they should have done it sooner, but they will catch up eventually.

Netflix’s ad-supported plan has nearly 5M monthly active users after just six months. On average, more than a quarter of Netflix sign ups now choose the ads plan in countries where it’s available.

There are two observations from their ad-tier roll out, management stated:

1. Members from the more expensive ad-free tier didn’t really jump over to the cheaper ad-tier. This means that most of the ad-tier growth are new customers, which were previously priced out.

“Engagement on our ads tier is above our initial expectations and, as expected, we’ve seen very little switching from our standard and premium plans.”

2. The ad-tier actually turned out great, bringing in an even higher average revenue per member than the ad-free tier. This goes to show that advertisers were hungry for inventory in connected TV.

“We are pleased with the current performance and trajectory of our per-member advertising economics. In the US for instance, our ads plan already has a total ARM (subscription + ads) greater than our standard plan.”

Conclusion

I believe Netflix will continue to outperform its competitors. Increasing churn due to password sharing is likely, but it will be temporary and spur revenue growth.

>> Click here to read the Netflix Research Report that was published in April 2022.

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in Netflix at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).