MercadoLibre’s shares dropped 8% the day after reporting Q4 2025. Net income fell 13%. The clean EBIT margin (stripping out a one-off $99 million Brazilian tax credit) landed at 9.0%, down 450 basis points year-over-year.

The market saw margin compression and sold. I see a business I’ve watched before, doing exactly what it’s done before, and I’m buying.

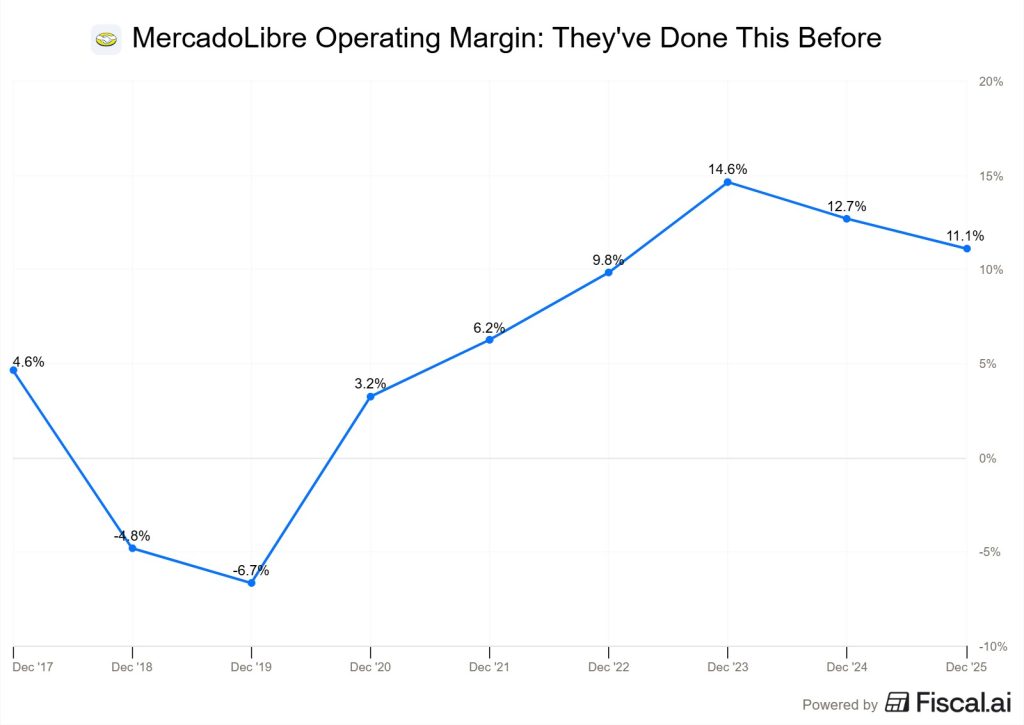

They’ve Done This Before

In 2017, MercadoLibre launched free shipping across its marketplace. Operating margins went from 4.6% to negative 4.8% to negative 6.7% by 2019. The stock suffered. The investment community questioned whether management was destroying value.

Then COVID arrived. MELI was the only platform in Latin America with the logistics infrastructure to meet the moment. Revenue went from $2.3 billion in 2019 to $7.1 billion in 2021. Margins recovered from negative territory to 6.2%, then 9.8%, then 14.6%. What looked like reckless spending was actually the foundation of the dominant e-commerce and fintech ecosystem in Latin America.

Source: Fiscal AI (get a 15% discount using this link)

That pattern is exactly what’s happening now. Invest aggressively, absorb the margin pain, build infrastructure that competitors can’t replicate, and emerge stronger.

The Quarter Underneath the Margins

Revenue of $8.8 billion grew 45% year-over-year, accelerating from 37% in Q1, 34% in Q2, and 39% in Q3. The 28th consecutive quarter above 30%. This is the strongest growth rate of the year.

Commerce is reaccelerating. GMV hit $19.9 billion, up 37% FX-neutral and accelerating from Q3. Items sold grew 43%. Brazil and Mexico both posted 45% items sold growth, the best quarter of 2025 for each market. Unique buyers rose 24% to 83 million, and purchase frequency (items per buyer) climbed to 9.0 from 7.8 a year ago.

Fintech is compounding. The credit portfolio reached $12.5 billion (+90% YoY). AUM hit $19 billion (+78% YoY). Fintech MAUs grew to 78 million, roughly 30% growth for 10 consecutive quarters.

Advertising grew 70%,and management noted penetration as a percentage of GMV is “still small compared to its potential.” Within the 3P take rate, advertising and loyalty revenue are partially offsetting the revenue forgone from free shipping, limiting the take rate decline to just 30 basis points year-over-year.

Where the Margins Went

Management quantified the investment drag at 5-6 percentage points of operating margin. That means the underlying business would be running at roughly 14-15% EBIT margins absent these deliberate investments.

Two buckets account for most of it.

Logistics and free shipping. In June 2025, MercadoLibre cut the free shipping threshold in Brazil from R$79 to R$19. On the Q4 call, SVP Commerce Ariel Szarfsztejn was direct: “This is the third time we’ve lowered the threshold, and the results we’re seeing now are no different from the past. Growth has accelerated, frequency has accelerated, we’re at record conversion rates and retention rates.”

The logistics network absorbed a 41% increase in shipment volume in 2025, nearly 500 million additional packages, while unit shipping costs in Brazil fell 11% in local currency. Fulfillment costs declined year-over-year in Brazil, Mexico, Chile, and Colombia. The efficiency gains are real. They just haven’t translated to margin expansion yet because management keeps reinvesting them into even lower thresholds and faster delivery. The same playbook as 2017.

Credit card expansion. Bad debt provisions consumed 250 basis points of operating margin because they’re making credit available to a wider pool of consumers. Osvaldo Giménez, President of Mercado Pago, was blunt: “We increased the number and riskier profile of people we gave credit to, but we priced that risk accordingly, and ended up having a larger spread than the prior quarter.”

Underwriting models keep improving. The credit card’s 15-90 day NPL (non-performing loan ratio, measuring loans that are 15 to 90 days past due) fell to a historic low of 4.4%, down over 300 basis points in three years, even as MELI expanded into riskier profiles. They’re pricing that risk accordingly, which is why NIMAL (net interest margin after losses, which captures the full equation of credit revenue minus provisions minus funding costs) expanded to 23.3% from 21.0% in Q3.

The Q4 shareholder letter confirmed that credit card cohorts consistently reach NIMAL breakeven within 12-18 months, and 75% of the credit card portfolio in Brazil has reached this milestone. In Q4, they issued nearly 3 million new cards. The front-loaded cost of new cohorts is enormous. But every prior cohort has matured to profitability on schedule. As CFO Martín de los Santos said on the Q3 call: “Last year, you saw when we invested on credit card, it required some margin compression. But now the credit card is starting to mature, and that turns around.”

The Capacity to Suffer

MercadoLibre generated $1.5 billion in adjusted free cash flow in 2025. After $1.3 billion in capex. After investing more than $6.5 billion in credit portfolio growth.

Revenue is reaccelerating. Purchase frequency is at record levels. NPS is the highest in both commerce and fintech across Brazil, Mexico, Argentina, and Chile. In fintech, it’s the first time Mercado Pago has led NPS in all four markets.

The shareholder letter said it plainly: “We do not solve for short-term margin optimization.” They said the same thing in 2017. Margins went negative. And then they built the dominant e-commerce and fintech ecosystem in Latin America.

This is a company with the capacity to suffer, sacrificing today’s margins for a stronger position in the future.

What You’re Paying

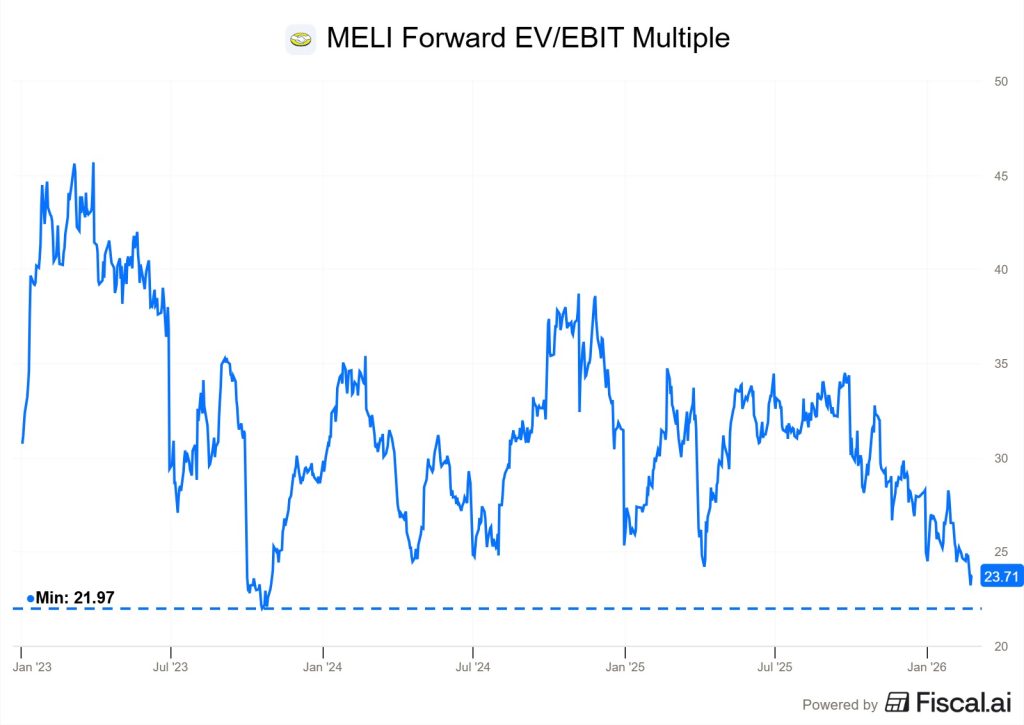

At current prices, MELI trades at 23.7x forward EV/EBIT, within striking distance of its 3-year low. The market is pricing in prolonged margin compression.

Source: Fiscal AI (get a 15% discount using this link)

It takes time, but every investment line is likely to mature toward profitability. Credit card cohorts break even in 12-18 months. Logistics unit costs are declining while volume surges. Advertising is growing 70% and partially offsetting the free shipping cost. If even half of the 5-6 percentage points of investment drag normalizes, today’s multiple on normalized earnings is substantially cheaper than it appears.

This isn’t without risks. Latin American macro, a credit cycle turn, or competitive pressures could all change the calculus. But near the lowest valuation in years, on temporarily compressed earnings, while the underlying business posts its strongest operating quarter of the year, I like the risk-reward setup.

Buy MELI, I am.

Thomas

P.S. For SCIS members, a portfolio update is coming before Friday’s market open. There are periods where nothing happens, and there are periods where a lot happens at once. The AI sell-off has served up some interesting opportunities, and I’ll be making changes soon. If you’re not a member yet, join here: steadycompounding.com/membership

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in MELI at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).

Hi, Thomas, what was the share price you had used to arrive at this 23.7 forward EV/EBIT? What would be a fair value for this stock? Thanks!

Hey Esther, it’s based on last night’s closing price. 1787. It’s roughly fair value now.