Let me just start right off the bat—this was a bad quarter and it reflected badly on CEO Calvin McDonald, who for the past 15 months has talked about missteps in the women’s category and the lack of newness.

Turns out, he was right about the problem, but dramatically wrong about the solution.

Right Problem, Wrong Solution

Here’s what McDonald said in Q1 2024 earnings call:

“In our women’s business, we had some missed opportunities really, in our color palette, in particular in some of key categories such as our legging business, where we didn’t have enough color, newness.”

The word color appeared 20 times in that earnings call.

Today, after more than a year, McDonald shared that it’s not about the colors:

“While the guest is responding well to many of our new styles, they are not reacting as we had anticipated to the updated seasonal colors we brought into our core assortment.”

And to add fuel to the fire, he added that their offerings have become stale:

“We have recently conducted a deeper product diagnostic, the results of which I will share with you today. I now believe we have let our product life cycles run too long within many of our core categories particularly in lounge and social. We have become too predictable within our casual offerings and missed opportunities to create new trends.”

Which raises the question, why only run the “deeper product diagnostic” now?

Why not listen and conduct studies on consumers when the problem arose? And if the solution for more sizes and colors weren’t working, shouldn’t the data on conversion be picked up way earlier given their DTC model?

The High-Value Customers Aren’t Buying

Granted, there were some new innovations, such The Align No Line, Daydrift and BeCalm, but it wasn’t enough to keep its most loyal customers spending enough.

As McDonald shares:

“Our most recent guest cohort, those that are in our low to mid-spend range, all are spending more with us year-over-year. The opportunity is with the high-value guests. They’re over-indexing on new styles and retention remains strong, but the opportunity is they’re spending less with us like, as I mentioned, to these core franchises, predominantly in lounge and social.”

Your best customers are pulling back. These aren’t price-sensitive shoppers. They’re telling you something about your product.

And this was the first quarter management acknowledged that the competitive environment has become tougher, as opposed to brushing them off in the past few quarters:

“The competitive landscape is different today than it was even 2 or 3 years ago. And while no single competitor is having a meaningful impact on our business, there are now many players in the market.”

The De Minimis Bombshell

Then there’s also tariffs and the De Minimis Impact, which according to CFO Meghan Frank,“we now expect a 220 basis point or approximately $240 million mitigated impact on gross margin for the year.”

De Minimis allows duty-free shipments below $800—and Lululemon has been taking advantage of this through their Canadian distribution centers. And there have been reports that as much as two-thirds of its shipments to U.S. guests are from Canada.

Of the 220 basis point impact to gross margins, the De Minimis impact would have accounted for 170 basis points.

Now, President Trump signed the executive order “Suspending Duty-Free De Minimis Treatment for All Countries” on 30 July, 2025 (LINK).

But this isn’t a sudden change, on 2 April, 2025, on liberation day, there was the executive order “Regulating Imports with a Reciprocal Tariff to Rectify Trade Practices that Contribute to Large and Persistent Annual United States Goods Trade Deficits” (LINK) which spoke about how De Minimis clause would come to an end, once the government has developed the system in place to collect tariffs on them:

“After such notification, duty-free de minimis treatment under 19 U.S.C. 1321(a)(2)(C) shall not be available for the articles described in subsection (a) of this section.”

And subsection (a) referred to ALL imports in the U.S. will not have de minimis treatment, and will be subjected to at least an additional 10% tariffs :

“Except as otherwise provided in this order, all articles imported into the customs territory of the United States shall be, consistent with law, subject to an additional ad valorem rate of duty of 10 percent.”

Let me be clear about the timeline here: The April 2nd executive order signaled the end of De Minimis. Lululemon’s Q1 2025 earnings call happened on June 5th—giving management two full months to assess the impact and warn investors about the bulk of its ecommerce orders running through its Canada warehouse .

Instead? Silence.

We’re only hearing about this impact now, in Q2, after the July 30th order made it official. This isn’t transparent. Management knew a significant risk was materializing and chose to stay quiet.

I do not like this.

Bad things are going to happen, but what’s important is that management has to be candid and transparent with investors. As Buffett says, “When you find bad news, I say get it right, get it fast, get it out, get it over.”

China’s Warning Signs

The last piece of bad news comes from their fastest, and most promising market, China. From CEO Calvin McDonald:

“When looking at China, quarter 2 revenue came in at the low end of our expectations as we’re beginning to see some signs of macro-driven headwinds in Tier 1 cities.”

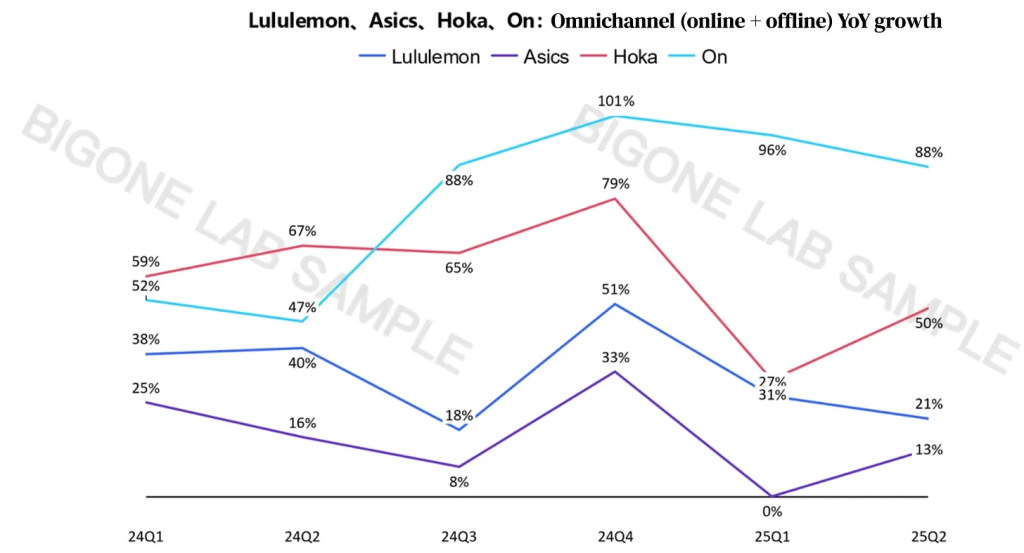

Separately, there has been reports from Bigone Lab (LINK), an independent research firm on China markets, that reported:

“In recent years, emerging brands that deliver both professional-grade functionality for a specific sport niche and a distinctive sense of taste—such as running shoes from Hoka or On Running—have consistently outperformed brands that focus on generalized sports merchandise and sell a trendy, middle-class lifestyle image. (One example is Lululemon, whose growth has slowed in recent quarters.)”

So we have product misdiagnosis in the core market, surprise tariff impacts eating margins, and now growth deceleration in their most promising market. Yet despite this cascade of problems, McDonald clings to one consolation prize.

Lululemon has “continued to gain market share within performance apparel even as the sector has declined according to the latest Circana market share data for the U.S. activewear space.”

I noted that he only pointed out performance apparel this time round, and did not mention another of its core category, lounge and social apparels.

It’s Always About The Management

A big part of the thesis is on the assessment of the management calibre who pulled Lululemon out of its mid-2010s slump, which began in 2013, following a major recall of its signature black “Wunder Under” yoga pants after customers complained that the material was too sheer and see-through. The recall affected 17% of the pants sold in its stores at the time.

Former Lululemon CEO Christine Day mismanaged the company and we saw growth rates plummet from above 30% to low-teens between 2014 to 2017.

When Calvin McDonald took over the CEO role in 2018, he successfully led Lululemon’s turnaround. Revenue exploded from $2.6 billion to $9.6 billion by 2023—a 24% annual clip. Operating cash flow surged even faster, from $489 million to $2.3 billion.

His “Power of Three x2” plan to double the business in five years? He did it in three.

That was remarkable execution, but given the execution missteps we see today, I may have to reassess my evaluation.

Notably, there was also an expert call published by Inpractise with a former Lululemon Creative Executive who discussed the challenges the creative team faced with CEO Calvin McDonald since Sun Choe left her role as Chief Product Officer:

“This has created a disaster because it’s unclear who makes the final decision. Is it design-led? Since Calvin now has the creative director reporting to him, Nikki is reportedly very hands-off and the team doesn’t feel valued. From a product line management perspective, culture and talent attraction are significant issues.

I’ve never been in a company where people are so unhappy. It’s quite sad. There’s also a lack of innovation. They’ve relied too much on the Align tight and missed trends like the decline of tight jeans, which affects tights as well. They attempted wider pants at $120, but who’s buying oversized pants at that price?

They face trend challenges and haven’t introduced anything new or innovative. Their attempt with Breeze Through was a disaster resulting in returns. They keep saying to wait for Jonathan who’s been in his role for over a year, but it takes 18 months to two years to bring something to market.”

The Numbers Don’t Lie

Revenue crawled 7% higher to $2.5 billion. But geography tells the real story:

Americas Region (The Core Rot)

- Total growth: 1%

- Comparable sales: -4%

- U.S. market: Flat

- Canada: 1% growth

International Markets

- China Mainland: 25% growth (24% constant currency)

- Rest of World: 19% growth (15% constant currency)

Notably, Canada which used to be the bright spot for growth in the Americas, has also seen a significant slowdown. And I suspect if they don’t fix the root of the problem—innovation—it will trickle over to its international markets.

But the most disturbing metric comes from the inventory bloat which surged 21% to $1.7 billion while revenue grew just 7%.

On a unit basis, inventory jumped 13%.

CFO Meghan explained that the discrepancy is due to “higher tariff rates relative to last year as well as foreign exchange.”

There are two implications from this:

- Cash is trapped in inventory, and

- Markdowns are coming as management admitted to having “more seasonal inventory than we need”

On markdowns, management expects them to be “80 basis points higher than 2024, driven by increased seasonal clearance.”

Why I Don’t Agree With Their Next Steps

Firstly, product and design overhaul. The company is increasing new styles as a percentage of their overall assortment from the current 23% to approximately 35% next spring.

Secondly, they plan to speed up their supply chain, as CEO Calvin McDonald shares:

“We are also enhancing our capabilities to go faster within our go-to-market process. By working with our vendors, we have and will continue to improve our ability to chase into strong performing styles outside of our mainline product development process. We have also improved our fast-track design capabilities, which reduces lead times by several months for select styles. These have been fully incorporated into the upcoming seasons to give us added flexibility to anticipate, meet and potentially exceed guest response and demand.”

I’m not that certain that adopting fast fashion strategies is the right approach to resolving this issue. In fact, I’m worried it may do the opposite.

At the heart of it, Lululemon is known for quality, and what I’m missing from this earnings call is any discussion about its technical fabrics. Not one word about technical innovation.

They’re trying to out-Zara Zara instead of out-Lululemon the competition.

They need to double down on quality, not speed.

And with that, management has shifted the timeline, from the remedies that were supposed to have fixed the problems early this year, to 2026 onwards.

The Verdict

To borrow Buffett’s recent comment on the Kraft Heinz split, I’m “disappointed” in Lululemon’s execution missteps.

While the missteps have been costly, I do not think that the company’s brand integrity has been compromised. Yet. That “yet” is doing heavy lifting.

McDonald had everything going for him—a powerful brand, loyal customers, and a proven playbook. Instead of doubling down on what made Lululemon special, he’s chasing symptoms while the disease spreads.

So what do I plan to do as a shareholder of Lululemon?

I will be publishing another post on what I plan to do exclusively to Steady Compounding Insider Stocks on my thoughts.

Disclaimer: These research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in Lululemon at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).