The Psychology of Money is one of the most highly anticipated books for finance enthusiasts in 2020. Morgan Housel has a knack for writing beautifully and a flair for capturing abstract concepts on paper. This is uncommon for writings in the realm of finance.

Reading this book made me reflect a lot and helped fine-tune my thinking. It also made me think a lot about the problems many of my friends shared with me—keeping up with the Joneses, staying in a job that’s costing their health for the high paycheck, and worrying about stock market volatility.

I had a tough time choosing the key lessons from this book because it’s filled with great insights. After much deliberation, the following are my key takeaways which would be helpful both for me and my friends.

The Price of Success

Investing is simple, but not easy.

By simply investing in the S&P 500 index over a 20-year period, we could generate a return of 8% to 11% with dividends reinvested.

The S&P 500 increased 119-fold in the 50 years ending 2018. All you had to do was sit back and let your money compound. But, of course, successful investing looks easy when you’re not the one doing it.

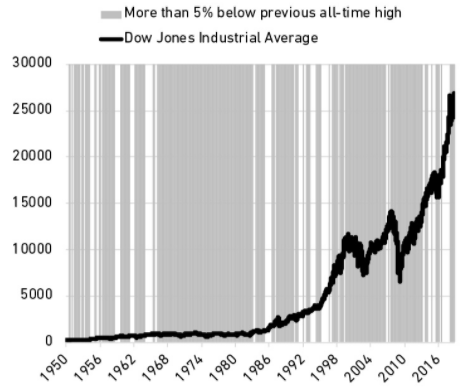

Sounds simple?

In his book, Housel presented the chart below where the shaded lines indicate at least a 5% decline below its previous all-time high.

Since 1928, the S&P 500 has declined by 10% or more 91 times. 20% declines have occurred 22 times. It has declined more than 30% once every decade with more than 40% decline once every few decades.

Amidst the long backdrop of growth are drawdowns of multiple magnitudes. To enjoy the growth, investors must be able to stomach the sharp drawdowns which come every now and then.

To enjoy the reward, you need to pay the price — volatility.

Sensible optimism is a belief that odds are in your favor, and over time things will balance out to a good outcome even if what happens in between is filled with misery.

Between the start and the end, know that it will be filled with misery. Be optimistic that the long-term growth trajectory is up but the route to the prize is a tough one.

Beyond Spreadsheets

Most people will agree that buying lottery tickets is a mathematically unsound decision. It perplexes me when people I know routinely purchase lottery tickets three times a week—especially when they are tight on cash!

Oftentimes the reasoning is “有买有希望,没买没希望。” Translated, this means, “There’s hope if I buy, but there’s no hope if I don’t buy.”

Few people make financial decisions purely with a spreadsheet. They make them at the dinner table, or in a company meeting. Places where personal history, your own unique view of the world, ego, pride, marketing, and odd incentives are scrambled together into a narrative that works for you.

Everyone has their own experience of how the world works. What I experienced is likely vastly different from what my parents experienced. All of us go through life anchored to our perception about how money works, and that perception varies widely from person to person.

Buying the lottery seems crazy to me but it makes sense for others.

I’m certain that you and I have some version of ‘craziness’ ourselves, anchored by perceptions formed from our experiences. Strive to continuously read books, especially from authors with differing opinions and consider their propositions in totality.

Beware of learning solely from social media sites, e.g., Youtube, Facebook, or Instagram. The algorithms work to reinforce your existing anchored views.

Tails Drive Everything

At a party given by a billionaire on Shelter Island, Kurt Vonnegut informs his pal, Joseph Heller, that their host, a hedge fund manager, had made more money in a single day than Heller had earned from his wildly popular novel Catch-22 over its whole history. Heller responds, “Yes, but I have something he will never have . . . enough.”

The case of Long Term Capital Management (LTCM) is an interesting one. They had 16 experienced professionals, including two Nobel prize winners. Collectively, the team probably had more than 350 years of experience in the investing business. They had an incredible amount of intellect and they invested most of their net worth into LTCM.

And then they went broke.

As Buffett says: “But to make money they didn’t have and didn’t need, they risked what they did have and did need. That is foolish. That is just plain foolish. It doesn’t make any difference what your IQ is. If you risk something that is important to you for something that is unimportant to you it just does not make any sense.“

There is no reason to risk what you have and need for what you don’t have and don’t need.

Many take on leverage to invest in stocks, given that interest rates are at historical lows. As tempting as it is, I have abstained from doing so out of a respect for tail-end risks.

Long tails—the farthest ends of a distribution of outcomes—have tremendous influence in finance, where a small number of events can account for the majority of outcomes.

What will wipe most leveraged investors out is when the market swings three standard deviations to the left (the yellow zone).

Is it likely to happen? No.

But if it does, leverage increases your probability of being wiped clean.

As Charlie Munger says, “The first rule of compounding is to never interrupt it unnecessarily.”

Even if the odds looks favorable, the key to success in building up wealth is in avoiding ruin. Even with a 95% success rate, the 5% odds of being wrong means that we will certainly experience downside at some point. And if the cost of the downside is ruin, no amount of reward is worth the risk.

As we look at what happened during the market bottom in March 2020, highly leveraged investors are more likely to cave in to volatility. When the market is soaring, risk appetite increases and leveraging up feels great.

During sharp drawdowns, your cash flows may be affected. Your emotions may spiral out of control as you look at your family and your bills.

Over-leveraging, not having at least six months’ worth of emergency cash, and inadequate insurance coverage all raise the probability of ruin—the risk of liquidating your positions at the worst possible time because you need the money.

On the flip side, Peter Lynch’s famous quote, “In this business, if you’re good, you’re right six times out of ten” reflects the other spectrum of long tails, where a handful of winners will propel bulk of your portfolio’s returns.

The Russell 3000 has increased more than 73-fold since 1980. That is a specular return. That is success. Forty percent of the companies in the index were effectively failures. But the 7% of components that performed extremely well were more than enough to offset the duds.”

Housel further explains that not only do a few companies account for most of the market’s return, but within these companies, a few tail events account for majority of the companies’ successes.

In 2018, Amazon alone drove 6% of the S&P 500’s returns, and Amazon’s advancement was largely due to Prime and Amazon Web Services (AWS)— both of which are tail events given that the company has experimented and failed with hundreds of products (e.g., Fire Phone) before striking gold.

“It’s not whether you’re right or wrong that’s important,” George Soros once said, “But how much money you make when you’re right and how much you lose when you’re wrong.” You can be wrong half the time and still make a fortune.

Tails drive everything—don’t over-leverage your positions, and also appreciate that a handful of companies you own will deliver an outsized return for your portfolio, so hold onto them.

The Ultimate Goal

Being able to wake up one morning and change what you’re doing, on your own terms, whenever you’re ready, seems like the grandmother of all financial goals. Independence, to me, doesn’t mean you’ll stop working. It means you only do the work you like with people you like at the times you want for as long as you want.

This is it.

Money’s greatest value is its ability to give you control of your time.

Plenty of studies have shown that splurging money provides only temporary relief. Life is miserable when we take up jobs we hate to sustain a lifestyle we do not need.

As Naval Ravikant puts it, “Looking forward to holidays takes the joy out of every day.”

What’s more important is having control over our lives. Independence means that your family is taken care of. It means that you are able to take controlled risks and pursue your dreams with a greater peace of mind.

Money in and of itself will not make you happy. But having the liberty to pursue your desired life might.

Independence, regardless of income bracket, is determined by how much you can save. Avoid lifestyle inflation upon landing your first job or from your promotion.

Most importantly, don’t fall into the trap of buying things we don’t need to impress people we don’t like.

The Hedonic Treadmill

The hardest financial skill is getting the goalpost to stop moving. Modern capitalism is a pro at two things: generating wealth and generating envy… Wanting to surpass your peers can be the fuel of hard work. But life isn’t any fun without a sense of enough. Happiness, as it’s said, is just results minus expectations.

As I reflect on the paragraph above, I’m reminded of a few of my close friends. They bring home a big paycheck but are never satisfied. Great earning power sometimes inflict a curse called the “hedonic treadmill.”

It continuously shifts the goalposts of your financial dreams, extinguishing the joy you thought you would get from having more wealth, once you achieve it.

From observations, this is extremely pervasive in the sales industry, where luxurious cars, condominiums, and branded bags are deemed a ‘necessity’ for success.

“Someone will always be getting richer faster than you. This is not a tragedy”, says Munger.

Social comparison is the problem. In our minds, wealth is always relative and not absolute. You could be within the top 20% income bracket but if plagued by envy for your peers’ wealth, you’ll never be happy.

As Benjamin Franklin puts it, “It is the eyes of others and not our own eyes that ruin us. If all the world were blind except myself I should not care for fine clothes or furniture.”

The Role of Luck

Investing, as with life, is like a game of poker, not chess. A novice chess player would stand no chance against Garry Kasparov.

In life, and investing, you can make all the right decisions and still end up losing.

Likewise, you can make all the wrong decisions and still come up a winner.

The cover of Forbes magazine does not celebrate poor investors who made good decisions but happened to experience the unfortunate side of risk. But it almost certainly celebrates rich investors who made OK or even reckless decisions and happened to get lucky.

The worrying part about this is that many of us try to study and emulate rich investors who made reckless decisions and got lucky.

Be careful who you praise and admire. Be careful who you look down upon and wish to avoid becoming.

Realize that not all success is due to good decisions or diligence, and not all poverty is due to poor decisions or laziness.

You’ll get closer to actionable takeaways by looking for broad patterns of success and failure. The more common the pattern, the more applicable it might be to your life.

Conclusion

Money is a relatively new tool and it is a subject that is very undertaught. Not understanding it caused many to bury themself in debt, sell at market bottoms, or become a tool for money. To better understand money, I strongly recommend The Psychology of Money, Dollars and Sense, and I Will Teach You to Be Rich.

For readers in Singapore, I would recommend you to check out the Seedly community.

Thank you for taking the time to read my blog.

In my next post, I will be back to writing on investment topics!

If you’re enjoying the content so far, I’m sure you’ll find 3-Bullet Sunday helpful. As an extension to the regular posts, I send out weekly newsletters sharing timeless ideas on life and finance.

I do not share this content elsewhere.

Join others and subscribe to our newsletter today to receive a free investment checklist!

highly resonated with the point on hedonistic treadmill!

Never get on it!

Love this :

At a party given by a billionaire on Shelter Island, Kurt Vonnegut informs his pal, Joseph Heller, that their host, a hedge fund manager, had made more money in a single day than Heller had earned from his wildly popular novel Catch-22 over its whole history. Heller responds, “Yes, but I have something he will never have . . . enough.”

Thanks for reading 🙂