Some of the most popular asset classes Singaporeans love are REITS, bonds, and stocks that pay a high dividend yield. And understandably so, because we are so sold on the idea of generating consistent, sustainable passive income to cover our expenses. It is almost like a Singaporean dream to invest for passive income.

There is nothing wrong with that and it is great that people are taking charge of their financial welfare. But that eagerness has caused many to be blindsided to the risks involved, and many more have been taken advantage of by financial institutions.

In this article, I will discuss bonds and leave the discussion of REITs and high-dividend-yield stocks for subsequent articles.

Bonds, Must Be Safe Right?

In today’s low-interest rate environment, I find it difficult to comprehend why anyone would subscribe to corporate bonds or perpetual securities when they only offer marginally higher interest rates than CPF. There are many risks associated with any investment which are often underestimated by retail investors. And these are definitely not what most relationship managers pitch as “buy-and-forget instruments”.

High profile defaults such as DBS Lehman Minibonds, Swiber bonds, and Hyflux bonds have caused investors much agony, especially those who poured their retirement savings into these instruments.

A self-employed man, who wanted to be known only as Mr Jin, said he had invested $500,000 in two Swiber bond issues through DBS. “I was simply following the advice of my relationship manager, who never told me much about the company. I just thought, a bank in Singapore, with this much regulation, would not recommend risky investments,” the 44-year-old said.

“Around 34,000 retail investors sank a total of $900 million into Hyflux perpetual securities and preference shares.”

“In all, nearly 10,000 people in Singapore stand to lose over S$500 million ($338 million) due to the collapse of Lehman Brothers Holdings Inc (i.e. DBS Lehman Minibonds), the central bank says.”

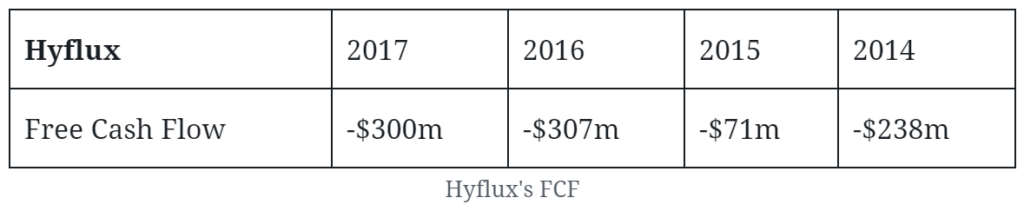

Taking a closer look at their financials, we realise that both Hyflux and Swiber had a negative free cash flow (FCF).

The same goes for Swiber. The company was bleeding cash in most years prior to issuing their bonds. The company made up for its shortfall by borrowing US$736 million from banks, with DBS being its largest creditor.

The point is, the interest for these products was anywhere between 5-7% only. Furthermore, bond investors do not participate in any upside, yet have to deal with the risk of total capital loss just like equity investors. The interest payments are fixed, meaning that if the company does well it is still going to pay you the agreed-upon interest payment. But if it runs into problems, you will suffer losses just like its shareholders.

When investing in bonds, it would serve investors well to think of it as lending money to their friends. A question you would naturally ask is, would they be able to repay me?

If this friend has been super reliant on credit cards for his day to day living (as in the case of Swiber and Hyflux by borrowing from banks), then we’d better think twice about lending them our money.

There is no easy way out when it comes to investing. If we do not have time to dig deeper, investors are better off putting money into CPF for a guaranteed 4-6% (depending on your current account balance and age) and not reach for an additional 1-2% worth of yield without understanding the risk-reward ratio.

You can also follow my Facebook page for updates here!