Sea Limited delivered an absolutely ridiculous set of results this quarter—the kind that makes you double-check the numbers. But while the headline figures are spectacular, there are a couple of things that raised my eyebrows. In this report, I’ll cover what went (ridiculously) well and what are some concerning points worth monitoring.

Digital Entertainment: Monetization Miracle, But Where’s the User Growth?

Garena delivered its best quarter since 2021 with bookings surging 51.1% year-on-year to $840.7 million. Revenue grew 31.2% to $653.0 million.

Here’s why bookings grew faster than revenue: bookings represent cash spent by users in the period, while revenue gets recognized over time as virtual items are consumed. Think of it as cash collected versus accounting revenue—the 51% bookings growth signals strong momentum ahead.

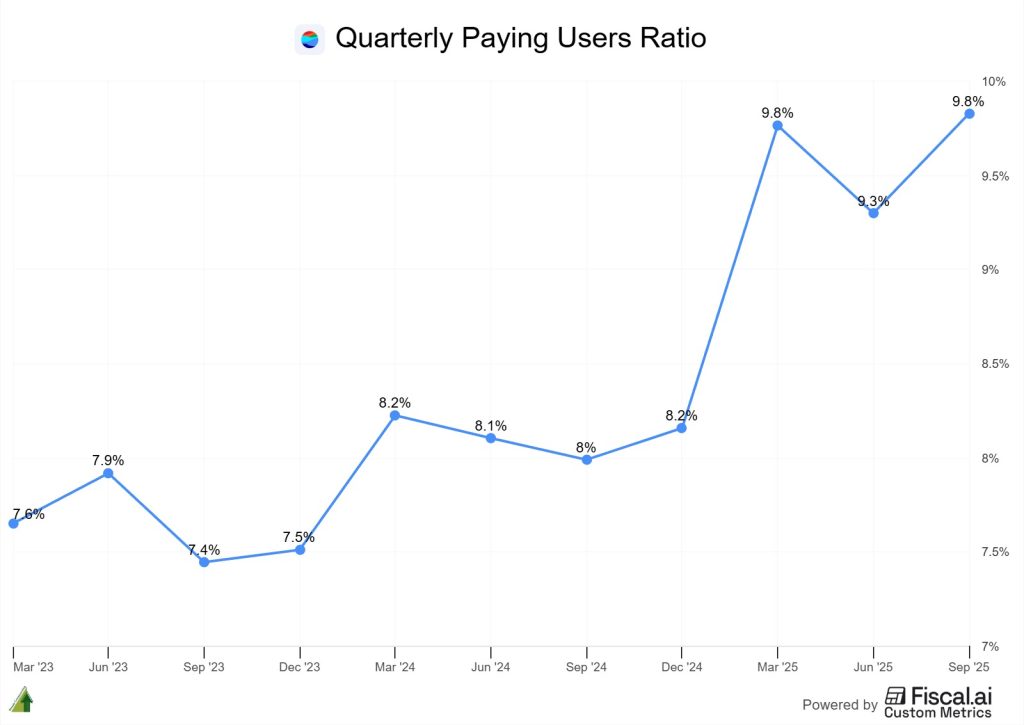

But here’s what caught my attention: this explosive growth was driven almost entirely by monetization rather than user expansion. Quarterly active users (QAU) increased just 6.7% to 670.8 million, while quarterly paying users (QPU) jumped 31.2% to 65.9 million, lifting the paying user ratio from 8.0% to 9.8%.

The uptick in paying users against total active players is clear:

Source: Fiscal AI (get a 15% discount using this link)

Management attributed the performance to two high-impact campaigns. As Forrest Li explained:

“Performance driven by two high-impact campaigns: Squid Game and NARUTO SHIPPUDEN Chapter 2… The Squid Game collaboration incorporated iconic challenges from the blockbuster Netflix TV series such as Red Light, Green Light and the Glass Bridge. The event drove strong participation with the Red Light, Green Light Challenge being played more than 300 million times in the quarter.”

The Naruto campaign was even more impressive, with Chapter 2 surpassing Chapter 1 in both engagement and revenue, achieving “the highest satisfaction scores of any campaign launched over the past two years.”

But here’s what bothers me: In my August report (LINK$), I highlighted Garena’s earlier announcement about Free Fire relaunching in India in September 2025. We’re not seeing any bump in QAU here, and management didn’t mention India once during the earnings call. Frankly, I’m surprised no analyst asked about it.

I assume the India relaunch ran into roadblocks, but I made a mental note that management wasn’t transparent enough to discuss this proactively. When guidance doesn’t materialize, good management addresses it head-on.

Despite sales and marketing expanding 253 basis points to 7.9% of revenue, adjusted EBITDA margin still increased 82 basis points to 71.4%—revenue simply grew faster than costs.

All in all, I’m genuinely surprised by how much bookings grew. It’s incredible. But for this to be sustainable, we need to see QAU growth. Monetization has limits; user growth is the seed for future expansion.

Shopee: Hyper-Growth with Puzzling Margin Compression

Shopee delivered spectacular top-line results with GMV growing 28.4% to $32.2 billion and revenue surging 34.9% to $4.3 billion. Core marketplace revenue (transaction fees and ads) grew even faster at 52.8% to $3.1 billion.

Take rates have expanded over the past two years:

From quarterly filings, author’s calculation

But this is where I start to raise my eyebrows.

Management has routinely laid out a clear path to 2-3% e-commerce EBITDA margins as a percentage of GMV. Yet this quarter, we saw profitability shrink to 0.6% from 0.8% in Q2, despite all the monetization gains.

I’d understand if profitability compressed because they’re cementing their moat with the Shopee VIP program and logistics investments. But here’s the puzzling part: value-added services revenue (mainly logistics) dropped 5.7% year-on-year against the backdrop of GMV increasing 28.4%.

That’s some aggressive subsidizing for growth. What makes this more concerning is management’s own characterization of the competitive environment. CFO Tony Hou stated:

“On the competitive landscapes, what we see is relatively stable competitive landscapes. I think as you can probably observe as well from your own sources. We didn’t see any particular market different from another.”

If competition is stable across markets, why the heavy subsidies?

The Brazil and Taiwan Stories

Brazil continues to be a bright spot. Management highlighted:

“Brazil: GMV growth outpaced the market, driven by sustained increases in monthly active buyers, purchase frequency, and average basket sizes while maintaining positive adjusted EBITDA… In the third quarter, GMV for Shopee Mall, our premium shopping section more than doubled year-on-year in Brazil.”

Taiwan showed interesting dynamics with their locker strategy:

“We expanded our automated locker store network to over 2,500 locations in less than 3 years, making us the only e-commerce player in Taiwan with a locker network at such scale… The lockers run at over 30% lower cost per order than traditional pickup locations.”

VIP Membership Gaining Traction

The Shopee VIP program is showing promise:

“By the end of September, VIP members across Indonesia, Thailand, Vietnam surpassed 3.5 million, up more than 75% from the previous quarter… In Indonesia, these members spend around 40% more after subscribing to the program.”

I’m all for cementing the moat and would give management the benefit of the doubt, but the disconnect between take-rate expansion and margin compression is worth monitoring closely.

Monee: The Incredible Beast

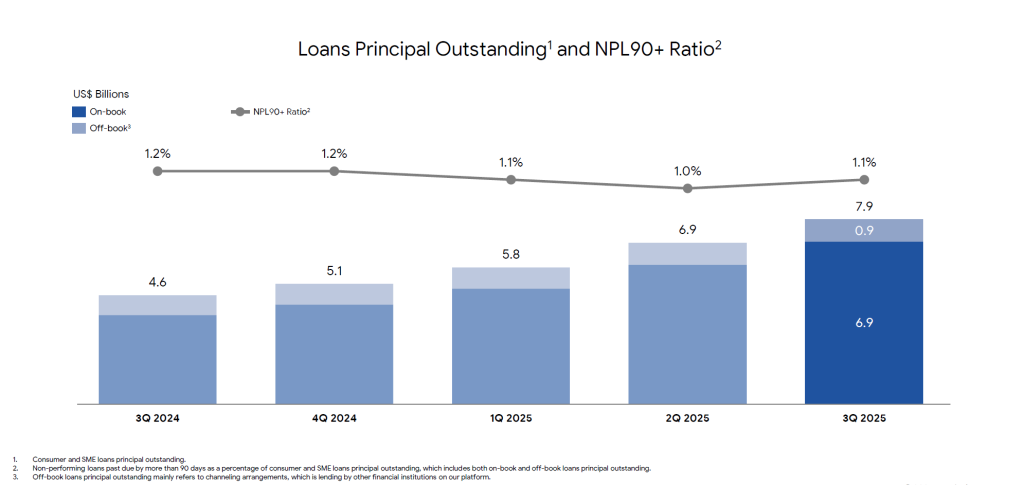

Monee (formerly SeaMoney) is just an incredible beast. Revenue grew 60.8% to $989.9 million with adjusted EBITDA up 37.5% to $258.3 million. The loan book expanded 69.8% to $7.9 billion while NPLs remained rock-solid stable at 1.1%.

Monee’s ability to scale while maintaining credit quality is impressive:

Q3 2025 Investor’s Presentation

Management provided color on the expansion strategy:

“We used to take a waitlist approach to onboarding new users. Now any Shopee user in most of our markets can apply for a pay later credit and we can make credit approval decisions very quickly, in many cases, almost instantly.”

This resulted in adding “more than 5 million first-time borrowers in the third quarter” with “new user cohorts scaled well with generally positive unit economics.”

Geographic diversification is working beautifully:

“Thailand has reached another major milestone, surpassing $2 billion in loans outstanding at the end of September. In Brazil, our loan book more than tripled year-on-year in the third quarter with improving portfolio quality.”

The off-Shopee expansion is particularly exciting:

“Off-Shopee SPayLater showed strong traction this quarter, growing over 300% year-on-year and over 40% quarter-on-quarter. It still only accounts for less than 10% of our total loan book.”

This segment continues to demonstrate that Sea’s real genius lies in leveraging its ecosystem—using Shopee’s data and customer base to build a highly profitable lending business with superior underwriting.

The Bottom Line

This was undeniably a great quarter, but this quarter has some data points which leave me raising my eyebrow:

- Garena needs to show QAU growth in a significant way. Monetization-driven growth has limits, and the silence on India is concerning.

- Shopee’s margin trajectory needs clarity. Are the VIP and logistics investments temporary drags, or is competition fiercer than acknowledged? The value-added services revenue decline suggests they’re subsidizing aggressively even in stronghold markets.

- Execution on strategic initiatives—particularly whether Shopee VIP can drive the loyalty and frequency gains needed to justify current investment levels.

Sea has proven it can deliver growth and profitability simultaneously. But I’m watching Q4 closely for answers to these questions.

Disclaimer: This research report constitutes the author’s personal views only and is for educational purposes only. It is not to be construed as financial advice in any shape or form. The author holds a position in Sea Limited at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).

Hi Thomas,

Saw your latest article on TTD and you will hold position and not add further.

What about on SEA especially after another trading session of almost -10% decline! ;(

Thanks.

Sea is actually pretty decent value now.