Netflix sort of reminds me of Microsoft when they were still young. Back in 1998, speaking at the University of Washington, Bill Gates said: “Although 3 million computers get sold each year in China, people don’t pay for our software. Someday they will, though, and as long as they are going to steal it, we want them to steal ours. They’ll get sort of addicted, and then we’ll somehow figure out how to collect sometime in the next decade.”

Piracy, and password sharing was rampant for both Microsoft and Netflix. Technologically speaking, while it was more challenging for Microsoft to enforce back in the 1990s, it wouldn’t have been a problem for Netflix to clamp down on password sharing in the 2000s early on.

Business school textbooks don’t teach you this, but when you are a pioneer in your field, such as Microsoft, with its operating system, or Netflix, with its streaming services, turning a blind eye to piracy/password sharing and acquiring new customers for free and getting them acquainted with your product might make sense. Obtain mindshare and market share first, and revenue will follow.

For Netflix, there’s three levers it could pull to drive future growth:

1. Increase memberships

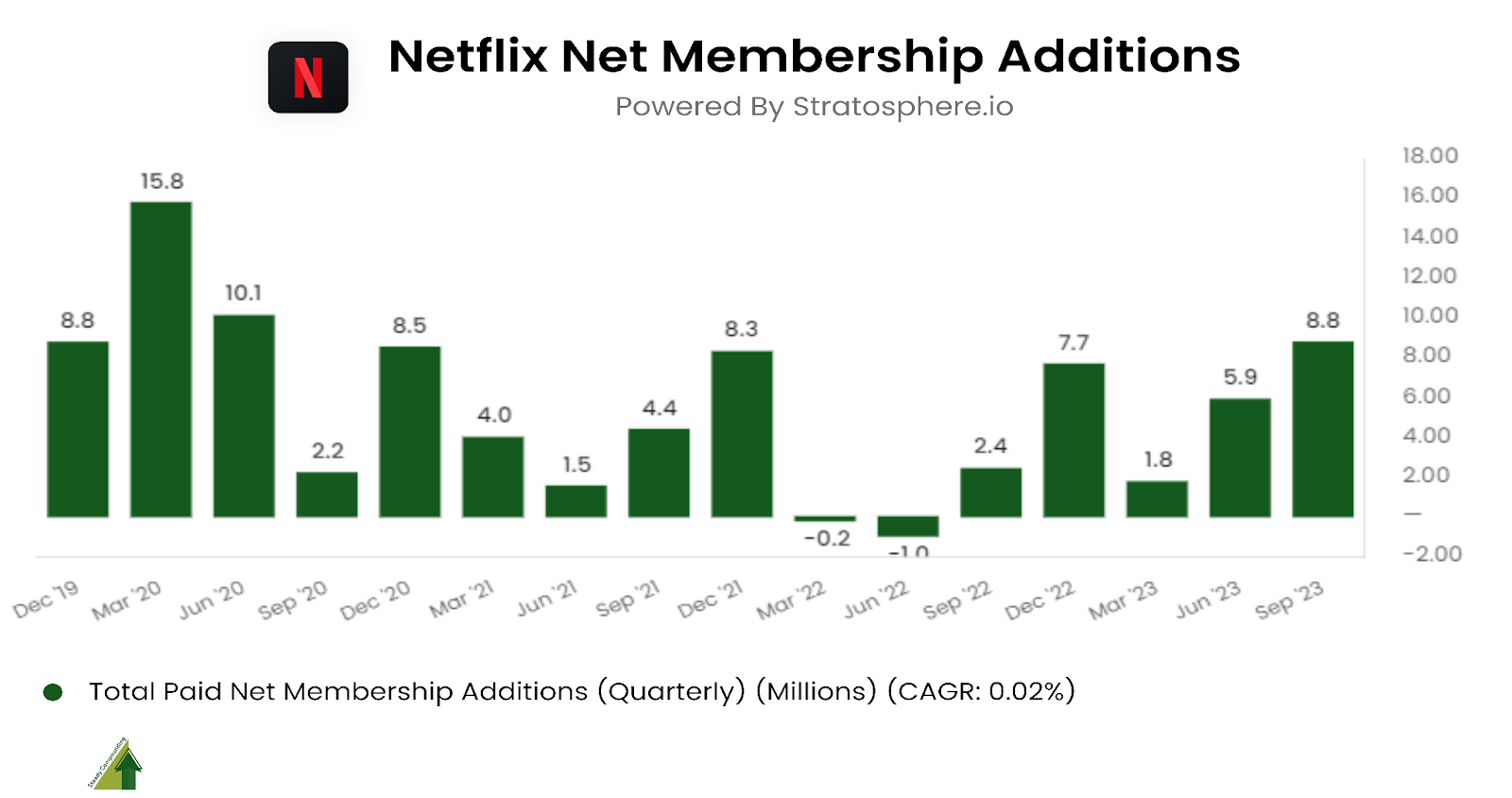

Netflix started password-sharing crackdown in May 2023 in phases and this quarter we were able to see their efforts bearing fruits. This quarter, they added a whopping 8.8m in net membership additions, bringing up their total paid memberships to 247.2m.

The membership additions from the password crackdown is likely to persist over the next few quarters. As Netflix didn’t implement this on its entire pool of membership in one shot, but rather, they’re doing it in a measured way:

“We’ve always thought this change should be done in a steady, considered way… As a result, there are a number of borrower cohorts, which as of today, have not received [the paid sharing crackdown notice]… We’re going to continue the roll out for the next couple of quarters… we anticipate that we will have incremental net adds for the next several quarters.”

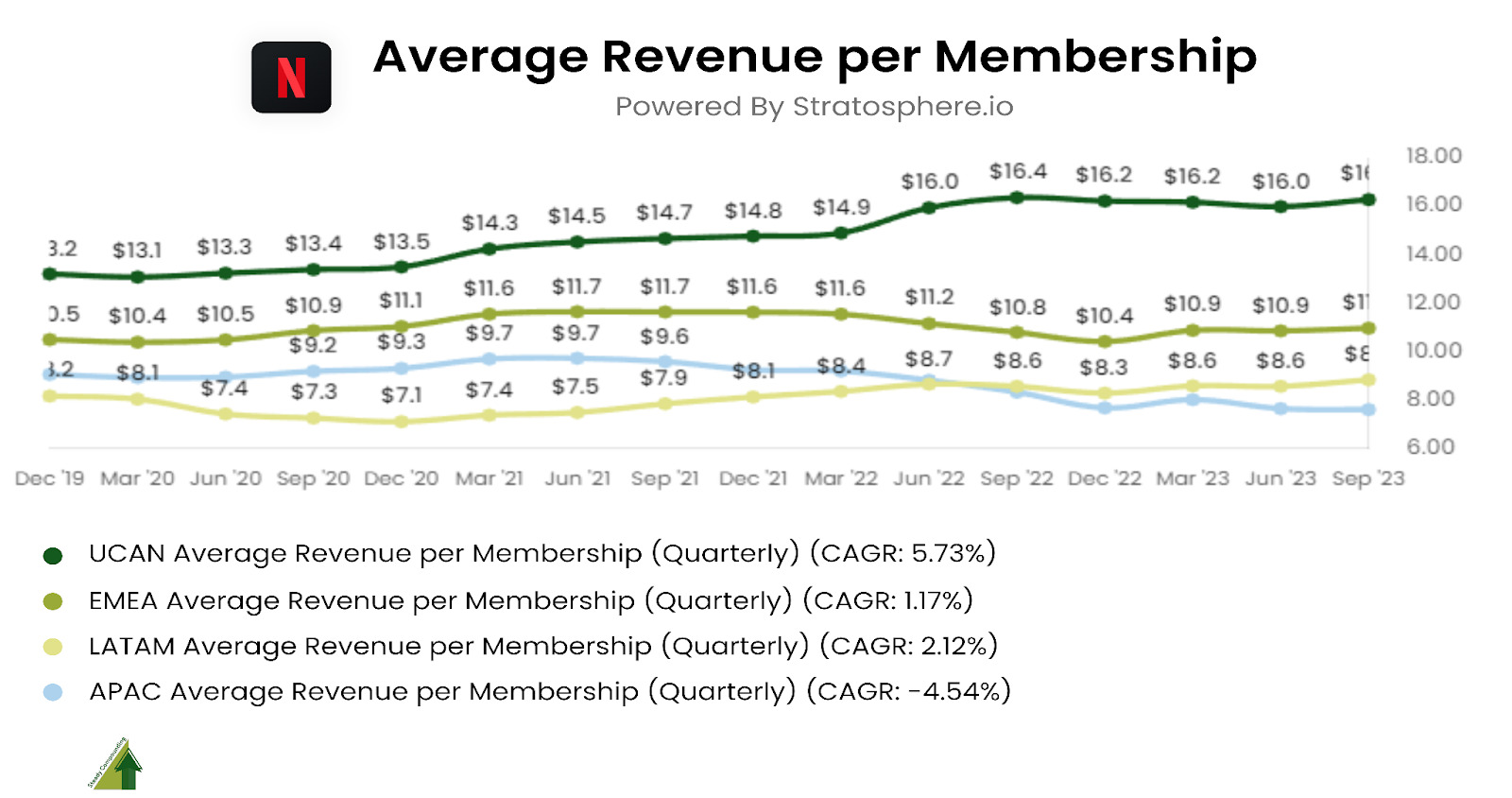

2. Increase average revenue per membership (ARM)

Over the past few quarters, Netflix has grown its UCAN ARM while maintaining its APAC and LATAM ARM at healthy levels, meaningfully higher than what Warner Brothers and Disney+ have been able to achieve.

I believe there’s still more room yet for Netflix to raise its prices as it still represents a small fraction of household monthly income and offers a deep pool of quality entertainment.

The company has just announced another round of price increases for both its basic and premium plan, while holding its ad-tier and standard plan steady.

For its premium ad-free plan:

- US: From $19.99 to $22.99

- UK: From 15.99 pounds to 17.99 pounds

- France: 17.99 euros to 19.99 euros

I would wager that now that the company has introduced an ad-free tier for $6.99 per month, it is more likely that they will raise prices more aggressively on the ad-free tiers since price sensitive customers will jump to the ad-tier rather than drop Netflix altogether.

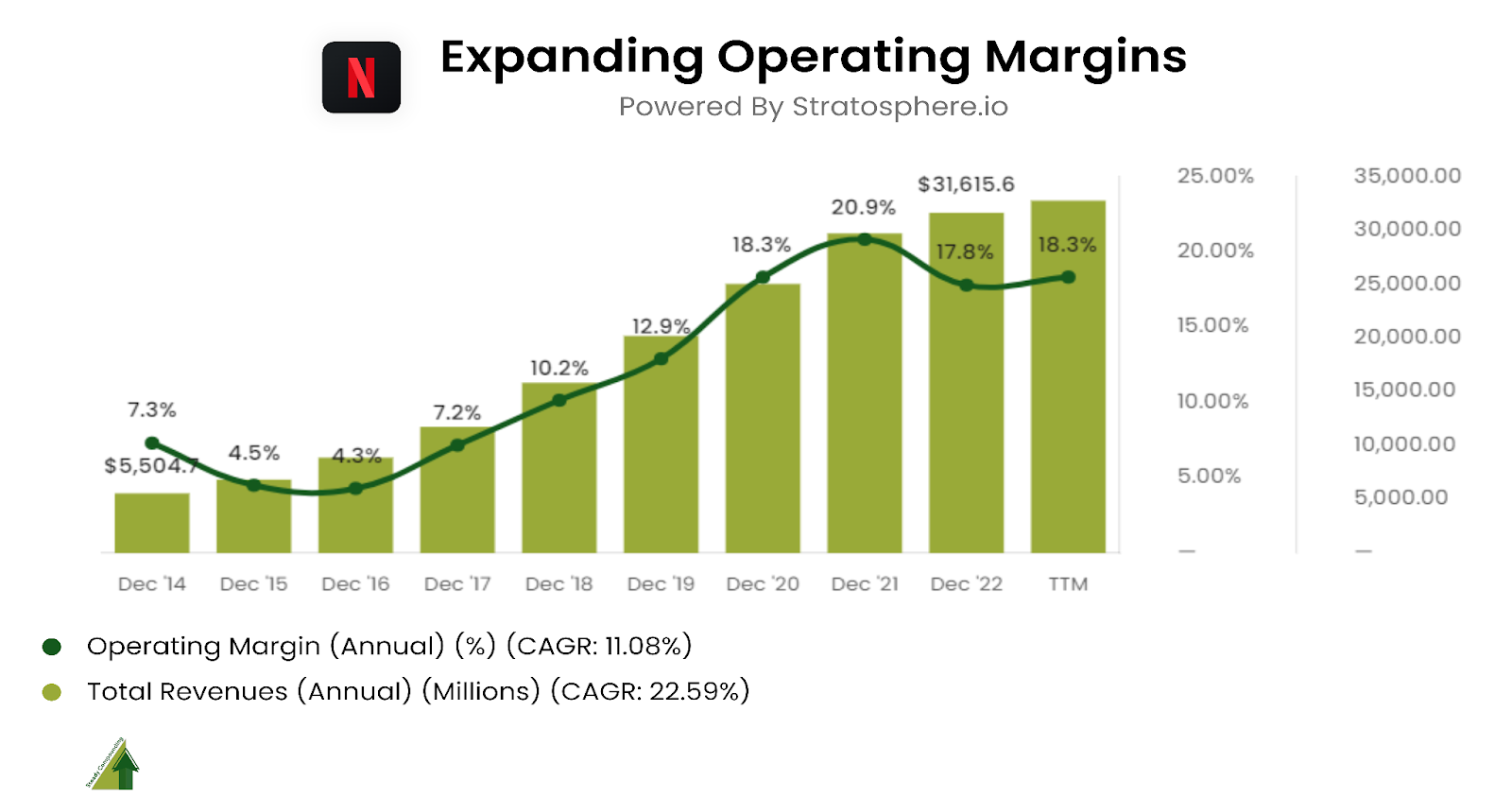

3. Expanding margins

As the number of subscribers and the fees increased faster than the amount they spent on content creation, we’re able to see expanding margins overtime.

Even though I’m happy to see margins expanding and I think there’s a lot more room to grow, I’m glad to hear that management is being cautious when it comes to extracting value from consumers and be prudent with raising prices:

“I don’t think it’s really prudent for us to keep growing [our operating margins] at three percentage points per year. That would probably constrain the business too much on the growth opportunity. So, we’ll grow margins more gradually.”

For FY 24, the company has guided for 200 – 300 basis points of margin expansion to 22% – 23%.

How does Netflix fare against competition

According to a Bloomberg article, streaming cancellations have hit a new high. About 6% of all streaming subscribers canceled their service in September.

There was increased churn across almost every streaming service, including Disney+, Apple TV+, Hulu, Max, and Starz. Netflix is one of the few exceptions, and certainly the only one who has a record spike in net additions post COVID, and is raising its prices while its competitors are suffering.

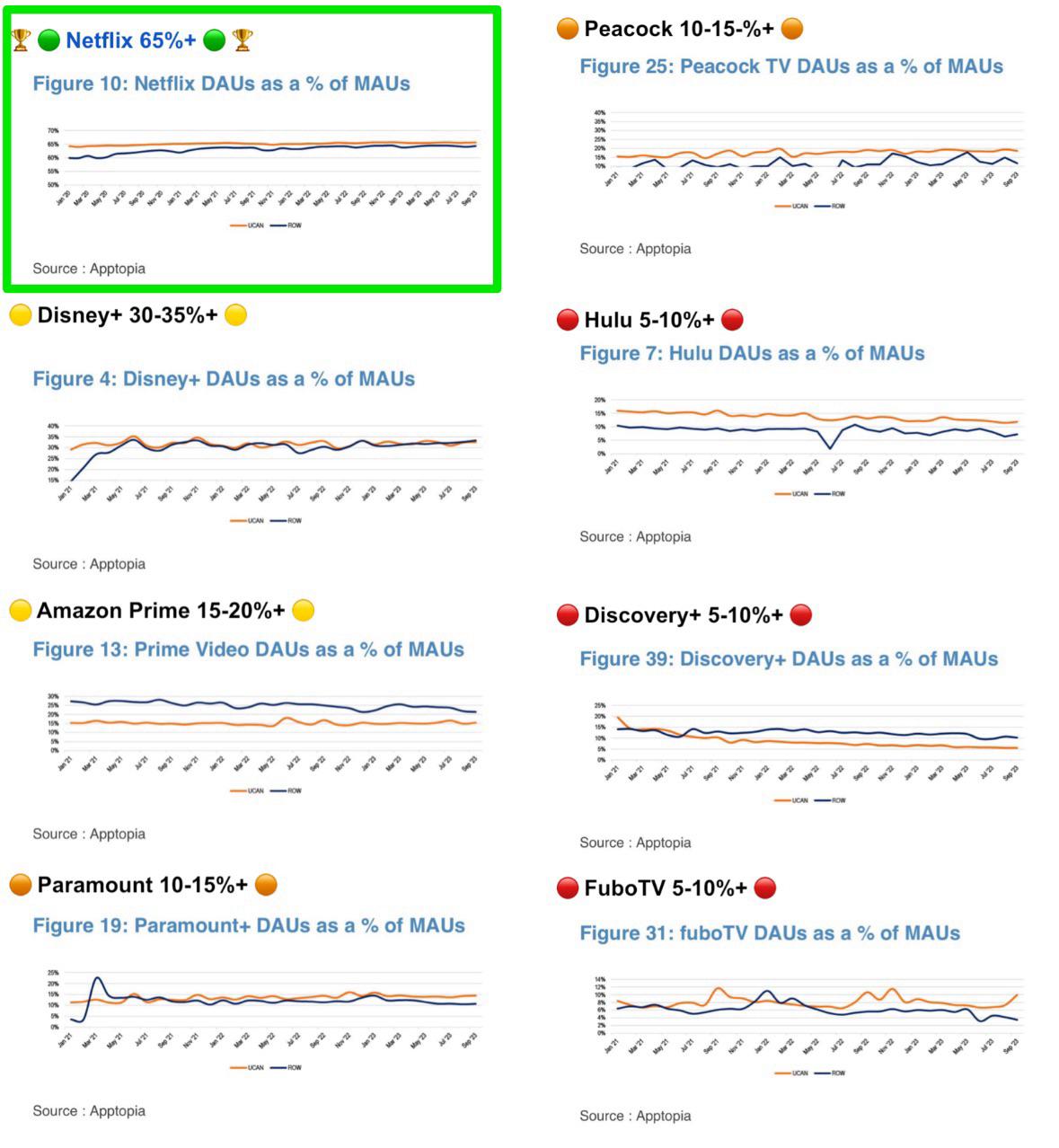

There’s a good reason for it, having a high subscribers count is one thing, but how active the subscribers are is a good indicator of how good the service is.

And Netflix has the highest daily active users (DAUs) as a percentage of monthly active users (MAUs), at 65%, crushing all its competition by a wide margin.

Credits to Eugene of Vision Capital for sharing these charts!

Oh, and one last thing. With the largest pool of members, Netflix has unparalleled distribution strength. Netflix broke viewing records in July with the debut of the licensed title Suits, which was already available on other streaming services.

“According to Nielsen, Suits was the most-watched title across film, original TV and acquired TV on streaming in the US for 12 weeks starting in late June (614M view hours – a new Nielsen record). Over that same time frame, Suits generated 1B view hours on Netflix globally.”

This distribution prowess puts Netflix in a great spot to secure great licensing terms. Apart from money, content creators want more people watching their work, building their brand equity.

In a fight between distributors and suppliers, such as Costco and Coca Cola, or Amazon and Visa, Coca Cola and Visa will have the upper hand initially, but as these distribution platforms grow, they gain more bargaining power over their suppliers as time goes on, negotiating for more competitive fees and prices. The same is likely to apply for Netflix, as it continues to grow.

Conclusion

Based on the latest numbers, Netflix remains the dominant leader in the streaming space, and it’s likely to continue to do so as it has the largest number of active users, showing that they’re delivering more value to consumers and have earned the right to raise prices. Having more subscribers, higher prices, and expanding profitability, they can continue to create more content for consumers and widen their moats.

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in Netflix at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).