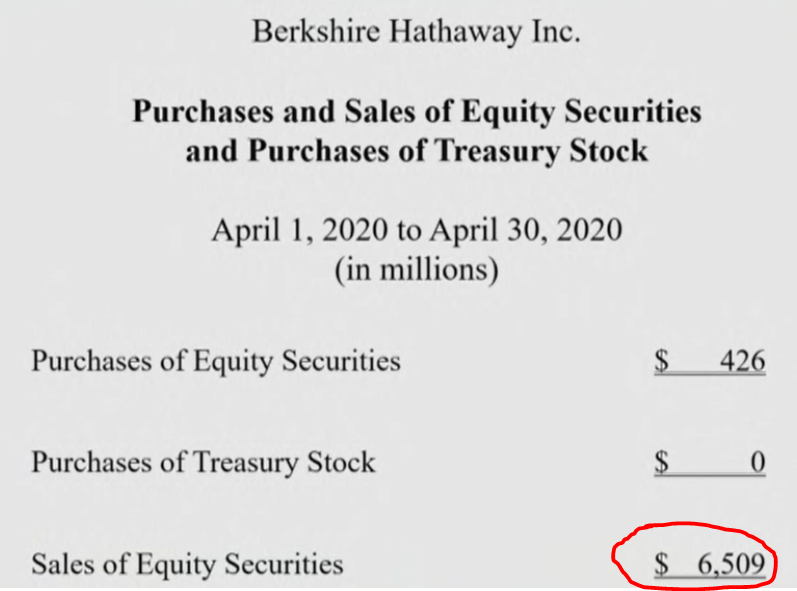

Warren Buffett started the Annual General Meeting (AGM) with a seemingly bullish stance, diving into America’s history and how it always emerged stronger. Despite painting a rosy image, it is important to observe his actions. Key decisions such as the sale of airline stocks, the lack of new investments and share repurchases indicated a much more bearish sentiment.

“But in any event, the range of probabilities on health narrowed down somewhat, I would say the range, the probabilities, or possibilities, and on the economic side are still extraordinarily wide. We do not know exactly what happens when you voluntarily shut down a substantial portion of your society.“

Warren E. Buffett

As the meeting unfolded, we were once again reminded of the Oracle’s ability to think in probabilities and the importance of taking action when circumstances change.

The Ability to Change Your Mind

When the facts change, I change my mind. What do you do, Sir?

John Maynard Keynes

Selling off the Entire Position in Airlines

In late 2016, Buffett revealed a surprise bet on the airline industry and took stakes in four major airlines – American Airlines, United Continental Holdings, Delta Airlines, and Southwest Airlines. In 2020, the stocks were down 63%, 70%, 59%, and 46% respectively.

His decision to sell highlights his ability to change his mind when new facts present themselves, rather than letting ego stand in the way. This was my biggest takeaway as it’s a tough pill to swallow when my investment thesis doesn’t pan out the way I expected it to.

In Buffett’s own words, “The airline business, and I may be wrong and I hope I’m wrong, but I think it changed in a very major way.” Similar to Singapore Airlines, these four airlines were each going to borrow an average of at least $10 to $12 billion each.

These debt obligations will severely impact shareholders’ returns over a prolonged period. And there was the possibility of the airlines having to issue shares at a cheap valuation to raise capital.

Furthermore, the demand for travelling two to three years from now remains uncertain. Passenger miles may not return to 2019 levels and airlines will not be profitable if passenger load falls below 70-80%. Buffett was concerned about the oversupply of airplanes as a result of COVID-19.

There could be many reasons he felt that there was potentially a structural shift happening. My guess is that business travel—which accounts for the highest margins (i.e. first class and business class passengers)—would significantly reduce as companies underwent rapid digitalization during this period. Meetings and deals could be executed online as opposed to having an executive fly several hours and spend a day or two away from home.

Lack of Share Repurchases

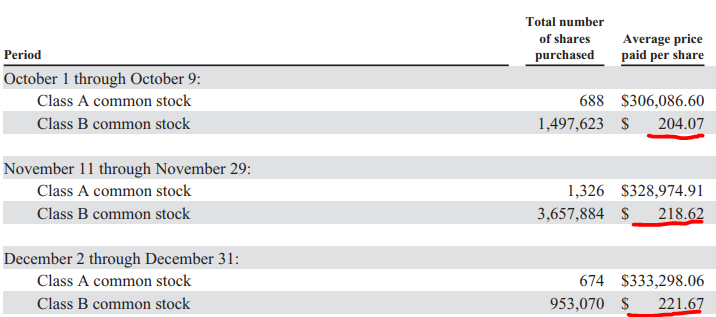

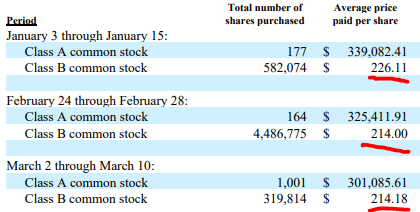

In 2019, Berkshire repurchased approximately $5 billion worth of shares during 2019. From their annual report, we could see that the company repurchase class B shares between $204.07 to $221.67 range.

When the class B shares plunged to $162 per share, many investors (including myself) expected Buffett to massively repurchase shares as the price was significantly below what he would consider to be undervalued back in 2019.

I was surprised when the total shares repurchased were only $1.7 billion in the first quarter of 2020, with Buffett ceasing share repurchases in entirety as the market went into free fall.

Once again, Buffett showed that when facts change, we have to adjust accordingly and not be anchored by our previous purchase price/ experience. He explained that Berkshire shares are not worth as much and it is not as compelling now to repurchase shares. Buffett was also honest in stating upfront that this was partly due to his mistake in purchasing the airlines.

Buffett emphasised that he much preferred to preserve the option value of money and that in order to benefit existing shareholders, share repurchases must only be done when current share prices are at a significant discount to intrinsic value.

You can also follow my Facebook page for updates here!