Meta delivered another quarter of strong performance. Revenue grew 24% to $59.9 billion. Net income came in at $22.8 billion, up 9% year-over-year. Operating margin held steady at 41%. The Family of Apps now reaches 3.58 billion daily active people, up 7% from a year ago.

These are phenomenal numbers for a company this huge. And this quarter’s earnings provided growing evidence that Meta’s AI investments are generating real, measurable returns.

The Core Business Is Accelerating

Let’s start with the fundamental drivers: impressions and pricing.

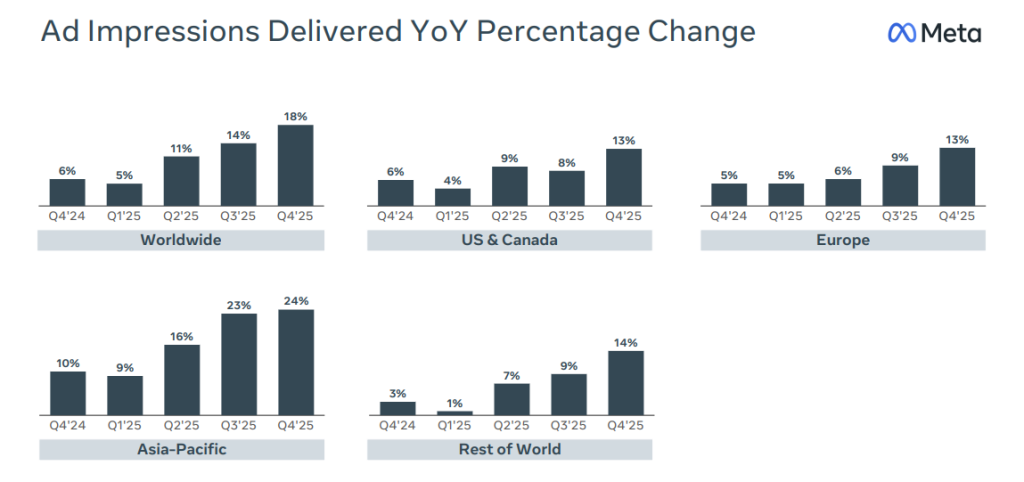

Ad impressions grew 18% worldwide, with healthy growth across all regions. Asia-Pacific led at 24%, followed by Rest of World at 14%, and both US & Canada and Europe at 13%.

What’s driving this? Engagement is up across the board. On the earnings call, Susan Li noted that Instagram Reels watch time increased more than 30% year-over-year in the US. Facebook video time grew double digits. Threads time spent jumped 20% after Q4 optimizations. These engagement gains translate directly into ad inventory.

The improvements stem from better recommendations. Meta simplified their ranking architecture to enable more efficient model scaling, which allows their systems to consider longer interaction histories to better identify user interests. On Facebook, these optimizations drove a 7% lift in views of organic feed and video posts, resulting in what Susan Li called “the largest quarterly revenue impact from Facebook product launches in the past two years.”

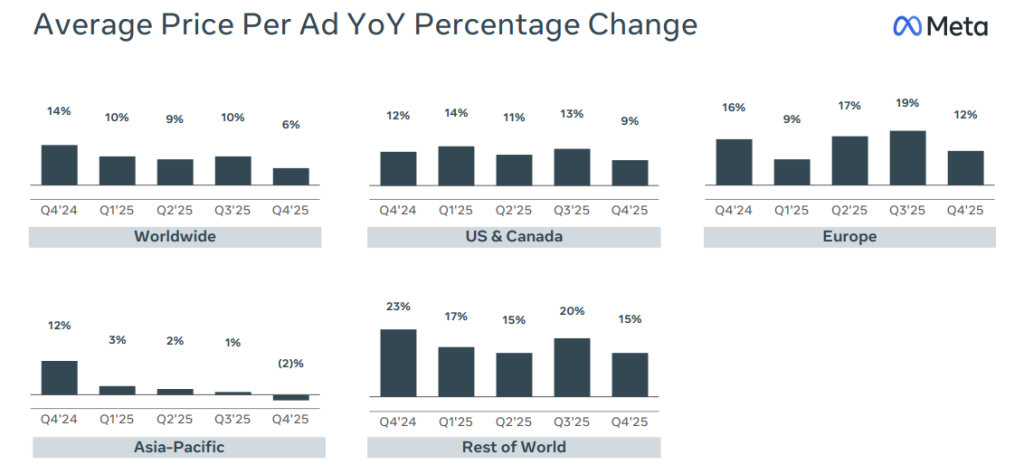

On pricing, average price per ad increased 6% worldwide. US & Canada saw 9% growth, Europe 12%, and Rest of World 15%. Susan Li attributed this to increased advertiser demand driven by improved ad performance. Online commerce was the largest contributor to year-over-year growth, followed by professional services and technology.

One regional anomaly worth noting: Asia-Pacific was the only region with declining ad prices, down 2%, despite having the highest impression growth. Management didn’t address this on the call. It suggests APAC is currently a volume story rather than a pricing story, worth noting.

The AI Investments Are Working

Meta provided concrete evidence that their AI spending is generating returns.

On ad ranking, they doubled the GPUs used to train GEM (Generative Ads Recommendation Model), a foundational AI model that powers the ranking and delivery of ads across Meta’s platforms. They also adopted a new sequence learning architecture.

The result? A 3.5% lift in ad clicks on Facebook and more than 1% gain in conversions on Instagram. They also launched a new runtime model across Instagram Feed, Stories, and Reels that drove a 3% increase in conversion rates.

Their incremental attribution feature, which optimizes for incremental conversions in real time, is now driving a 24% increase in incremental conversions versus their standard attribution model. This product launched just seven months ago and has already achieved a multibillion-dollar annual run rate.

Their AI-powered video generation tools, which help advertisers create video ad creative, are now at a $10 billion ad revenue run rate, with quarter-over-quarter growth outpacing overall ads revenue growth by nearly 3x.

Their initiatives to redistribute ads across users and sessions delivered a 4x larger revenue impact than simply increasing ad load. They’re getting smarter about when and where to show ads, not just showing more of them.

Internally, engineering productivity increased 30% since the beginning of 2025, with the majority of gains coming from agentic coding tools. Power users saw output increase 80% year-over-year.

These improvements are showing up in the revenue line.

The Elephant in the Room

Now let’s address what everyone’s worried about: the CapEx and the balance sheet.

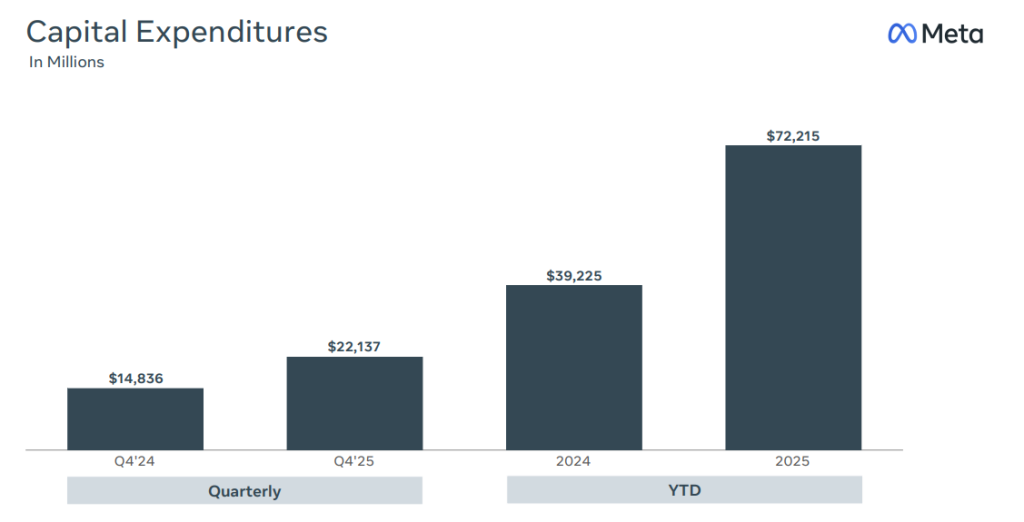

CapEx was $72 billion in 2025, up from $39 billion in 2024. Management is guiding $115-135 billion for 2026.

Net cash declined from $49 billion to $23 billion as debt doubled from $29 billion to $59 billion. Share buybacks, which totaled $30 billion in 2024, dropped to zero in Q4 2025.

I view the pause in buybacks positively. Buybacks should be the residual use of capital after all attractive reinvestment opportunities have been funded. When management sees opportunities to deploy capital at reasonable returns or strengthen the moat, that should take precedence.

Susan Li was direct about priorities: “Right now, we think the highest order priority for the company is investing our resources to position ourselves as a leader in AI.” She acknowledged they may eventually move to a net debt position:

“We will continue to look for opportunities to periodically supplement our strong operating cash flow with prudent amounts of cost-efficient external financing, which may lead us to eventually maintain a positive net debt balance.”

These are legitimate concerns. I’m not going to dismiss them.

But here’s what I find ironic about the current narrative.

Long-term intrinsic value growth is determined not just by high returns on invested capital, but also by whether a company has the opportunity to reinvest those returns at attractive rates. For years, the criticism of big tech was that they were hoarding cash with no reinvestment opportunities, just buying back stock because they had nothing better to do with the money.

Now Meta has a massive reinvestment opportunity in AI infrastructure that is demonstrably improving their core business. And they’re being criticized for taking it.

The right question isn’t “are they spending a lot?” The right question is “are they getting returns?”

So far, the evidence suggests they are. Revenue growth accelerated to 24%. Ad performance metrics are improving across the board. New products are scaling to multibillion-dollar run rates within months. Engineering output is up 30%. Infrastructure efficiency nearly tripled.

Susan Li explained their process: they use projected ROI to stack rank investments, maintain robust measurement systems, fund only positive-ROI initiatives, and track performance throughout the year. The 2025 investments “generally paid off,” and they’ve applied the same framework to the 2026 budget.

While I’m not a fan of Meta going into net debt territory, if they did, their $116 billion in annual operating cash flow can comfortably handle it.

Management also committed to a key guardrail: “Despite the meaningful step-up in infrastructure investment, in 2026 we expect to deliver operating income that is above 2025 operating income.” They’re not sacrificing profitability for growth. They’re doing both.

Reality Labs: The Bottomless Pit Bottoming?

One development that addresses a long-standing bear concern: Zuckerberg indicated Reality Labs losses are expected to peak.

“I expect Reality Labs losses this year to be similar to last year, and this will likely be the peak as we start to gradually reduce our losses going forward,” he said on the call.

Reality Labs lost $19.2 billion in 2025. The “bottomless pit” narrative has been a persistent criticism. Now management is guiding for peak losses and gradual reduction, while pivoting focus toward glasses and wearables where they’re seeing real traction. Sales of their glasses more than tripled last year.

This shows capital discipline. They’re not blindly funding moonshots indefinitely.

This Rhymes With 2022

In Q3 2022, Meta was investing heavily in AI to counter Apple’s iOS changes. CapEx was $9.52 billion against operating cash flow of $9.7 billion, leaving just $0.18 billion as free cash flow. Similarly, the market didn’t like it back then.

What I wrote then (link):

“Their heavy CAPEX spend relative to its operating cash flow does seem worrying but when viewed in another light, it might be more worrying if Zuck isn’t investing heavily into the business. And contrary to what most people are saying, most of the spending isn’t on the Metaverse, it is on its AI recommendation engine, which is imperative to running a world class social media platform at Meta’s scale.”

The AI investments paid off. The recommendation improvements management promised have materialized in measurable engagement and monetization gains.

The same framework applies now. Meta has a clear opportunity to invest in AI infrastructure that improves their core business. The early returns are visible, and I’m inclined to give management the leeway to invest away.

What I’m Watching

A few things to monitor going forward.

First, revenue growth versus the CapEx trajectory. If growth decelerates meaningfully while spending continues ramping, the thesis weakens.

Second, the 2026 operating income commitment. Management said operating income will exceed 2025 levels despite the CapEx step-up.

Third, Asia-Pacific pricing. It’s the only region with declining ad prices despite strong impression growth. Management didn’t explain why.

Fourth, Meta Superintelligence Labs progress. Zuckerberg was notably vague here, calling it “somewhat of an unfulfilling time to be answering some of these questions.” The near-term AI investments in ads and recommendations are clearly paying off. The frontier AI bets are longer-dated and less certain.

Bottom Line

Meta delivered strong Q4 results with accelerating revenue growth and clear evidence that AI investments are generating returns. Reality Labs losses are expected to peak. The balance sheet is being leveraged to fund infrastructure, but cash generation remains exceptional at $116 billion in operating cash flow.

The market is focused on the absolute dollar amount of spending. The right focus is whether that spending is generating returns. The evidence suggests it is.

As I wrote in 2022: it might be more worrying if Zuck isn’t investing heavily into the business. That view was validated over the following three years. And I’m inclined to give management the benefit of the doubt.

Disclaimer: These research reports constitute the author’s personal views and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the stocks mentioned below that are consistent with the views and opinions expressed in this article. Disclosure – I have a position at Meta at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).