Back in March, I wrote a piece titled “Why It’s Premature to Cancel Google Search.”

The thesis was straightforward:

“Writing off Google in search would be premature. Its younger competitors have their own set of problems—they need viable business models that allow them to offer their best AI models to everyone quickly and accurately. When I look at the evidence—increasing search volumes, successful monetization of AI features, infrastructure advantages, and competitors’ monetization challenges—I see a company that’s still adapting to a changing landscape rather than one being disrupted into oblivion.”

The market sentiment at the time was decidedly bearish. AI chatbots were the future. Traditional search was becoming obsolete. Google’s core business model faced an existential threat.

Q2 2025 results are now in. Let’s see what the data tells us.

The Numbers Tell A Different Story

Alphabet reported consolidated revenues of $96.4 billion, up 14% year-over-year. In constant currency, that’s 13% growth.

A company approaching $100 billion in quarterly revenue maintaining double-digit growth deserves attention.

The segment breakdown reveals broad-based strength:

Google Search & Other revenue reached $54.2 billion, up 12% year-over-year. That’s $5.7 billion in incremental revenue from the segment many consider under threat.

YouTube ads grew 13% to $9.8 billion, maintaining its momentum in a competitive video landscape.

Google Network declined 1% to $7.4 billion—the only segment showing weakness.

Total Google Advertising revenue hit $71.3 billion, up 10%.

Google subscriptions, platforms, and devices jumped 20% to $11.2 billion. This includes Pixel phones, YouTube Premium, Google One, and other consumer offerings.

Combined, Google Services reached $82.5 billion, growing 12%.

The standout performer was Google Cloud: $13.6 billion in revenue, up 32% year-over-year.

Source: Fiscal AI (get a 15% discount using this link)

The Profitability Picture

Operating income increased 14% to $31.3 billion. Operating margin held steady at 32.4%.

The flat margin despite strong revenue growth requires explanation. Management disclosed a $1.4 billion charge related to “a settlement in principle of certain legal matters,” which drove General & Administrative expenses up 65% to $5.2 billion (versus $3.2 billion in the prior year).

Without this one-time settlement, operating income would have been $32.7 billion, resulting in an operating margin of 33.9%—an expansion of 150 basis points year-over-year.

The underlying business is generating meaningful operating leverage. It’s just hidden beneath legal costs this quarter.

Segment operating margins tell two different stories:

- Google Services: 40.1% (stable)

- Google Cloud: 20.7% (up from 11.3% a year ago)

That Cloud margin number is remarkable. In just twelve months, profitability nearly doubled.

Google Cloud: The Transformation Story

Source: Fiscal AI (get a 15% discount using this link)

The magnitude of Google Cloud’s transformation cannot be overstated. Operating margins expanded from 11.3% to 20.7% in a single year—an increase of 940 basis points.

The segment has reached a new stage of maturity, now exceeding a $50 billion annual run-rate while demonstrating significant operating leverage. As the business continues to scale, there’s substantial room for margin expansion—AWS operates at 39% operating margins, providing a clear benchmark for what’s possible.

Management highlighted three growth drivers during the call:

Core GCP products continue to see strong enterprise adoption. Companies are migrating workloads to the cloud, and Google’s infrastructure capabilities are winning deals.

AI infrastructure demand is surging. Organizations need compute for training models and running inference. Google’s TPUs and GPU availability are key differentiators.

Generative AI solutions are gaining traction. Vertex AI, Gemini APIs, and enterprise search solutions are moving from pilots to production deployments.

The OpenAI partnership on Google Cloud, announced weeks prior, adds another dimension to this story. Even direct competitors in AI require Google’s computing infrastructure to operate effectively.

As Sundar noted: “We are very excited to be partnering with them (OpenAI) on Google Cloud. Google Cloud is an open platform, and we have a strong history of supporting great companies, startups, and AI labs.”

This illustrates Google’s infrastructure advantage—their computing capabilities are so advanced that competitors have little choice but to become customers.

The rapid margin expansion demonstrates the operating leverage inherent in the cloud business model. Fixed costs—data centers, chip design, software development—are now spread across a substantially larger revenue base.

While Cloud margins still trail Google Services’ 40.1%, the 940 basis point improvement in a single year shows the trajectory. At a 32% growth rate, the segment is rapidly becoming a more meaningful contributor to overall profitability.

Search: Not Dead, Just Evolving

The $54.2 billion question: Is Google Search actually being disrupted by AI, or is it adapting?

The revenue growth of 12% suggests adaptation rather than disruption. But revenue is a lagging indicator. What matters more is how users are engaging with Search and whether Google can monetize new AI features effectively.

Adaptation in Action

Google hasn’t been sitting still. The company has rolled out AI Overviews and AI Mode, fundamentally changing how users interact with search results.

AI Overviews provide synthesized answers directly in search results, similar to what ChatGPT or Perplexity offer. The key difference? These are integrated into the existing search experience rather than requiring users to visit a separate site or app.

Sundar Pichai reaffirmed a crucial data point during the call: these AI features are monetizing at rates “comparable or better to traditional Search results.” This echoes similar comments from previous quarters, showing consistent performance.

The bear thesis assumed AI would destroy search economics—that synthesized answers would eliminate the need for clicks and thus advertising opportunities. Instead, Google has found ways to monetize AI features as effectively as traditional blue links.

But what’s really driving the 12% search revenue growth?

Management seemed evasive when analysts pressed for specifics on search metrics. Philipp Schindler emphasized they “don’t manage to paid clicks and CPC targets” and cautioned against “drawing overly broad conclusions” from these metrics.

The numbers told an interesting story: paid clicks increased 4% year-over-year. With search revenue up 12%, Google’s growth is coming primarily from higher prices and, to a lesser extent, increased volume.

My take? AI Overviews are improving search result quality, which leads to better-qualified clicks for advertisers. Users get more relevant results, click on ads that actually match their intent, and advertisers pay premium prices for these higher-converting clicks.

AI Overviews are also expanding search use cases—people are now searching for queries they previously wouldn’t have bothered with. This backs up the thesis that both volume increases and quality of conversion improves. The enhanced capabilities are growing the overall search pie while making each slice more valuable.

The Accidental Cloudflare Advantage

Here’s where things get really interesting—and where most investors are missing a crucial piece of the puzzle.

Cloudflare recently made a dramatic change to their service, which handles approximately 20% of internet traffic. They now block AI crawlers by default across tens of millions of websites. The only major exception? Googlebot.

This creates a fascinating dynamic. Publishers face an impossible choice: they can’t afford to block Googlebot because it would mean losing Google Search traffic—economic suicide for most websites. But here’s the catch: court testimony confirmed that Googlebot doesn’t just crawl for traditional search. It also captures data for Google’s AI products, including AI Overviews and AI Mode.

The result? Google maintains uninterrupted access to fresh web content while competitors like OpenAI, Anthropic, and Perplexity are blocked by default. They must now negotiate individual deals or find workarounds to access the same data Google gets automatically.

This structural advantage can’t be replicated by competitors, at least for now. It’s not about better algorithms or more compute—it’s about access to data. And that access is now partially gated by infrastructure players like Cloudflare, whether intentionally or not.

YouTube: The Powerhouse Continues

YouTube ads grew 13% to $9.8 billion, maintaining steady momentum in an increasingly competitive landscape.

The real story here is YouTube Shorts. Management revealed several stunning data points:

YouTube Shorts monetization has reached a milestone: in the USA, it now generates the same revenue per watch hour as traditional YouTube. In some countries, Shorts actually generates more revenue per watch hour.

This challenges the narrative that short-form content can’t be monetized effectively.

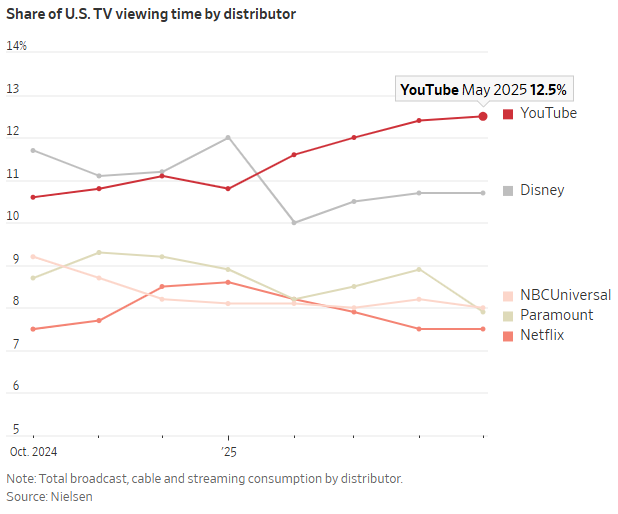

The platform now has 200 million daily views on Shorts. For context, YouTube has led US streaming watch time for 2 years running, hitting a record high 12.8% of total TV views.

Management is leveraging AI to improve content recommendation and dubbing capabilities, which helps widen the audience reach for creators. They’re also rolling out new AI tools specifically for Shorts creators.

The implications are profound. YouTube has cracked the code on short-form monetization while maintaining its dominance in long-form content and connected TV (CTV). It’s competing effectively across all video formats and screen sizes.

The subscription business—YouTube TV, YouTube Music, and YouTube Premium—continues its strong trajectory, contributing to the 20% growth in Google’s subscriptions, platforms, and devices segment.

Other Bets: Waymo’s Steady Progress

While most of Alphabet’s “Other Bets” remain in investment mode, Waymo continues to make tangible progress.

The autonomous vehicle service is expanding to Atlanta and Austin, adding to its existing operations in Phoenix, San Francisco, and Los Angeles. The commercialization path is becoming clearer as Waymo moves beyond pilot programs to actual revenue-generating rides.

While the segment still loses money (Other Bets posted a $1.2 billion operating loss), Waymo is the closest to achieving meaningful scale among Alphabet’s various bets.

The Investment Phase: Understanding the FCF Decline

Let’s address the elephant in the room: Free cash flow declined 61% year-over-year, from $13.5 billion to $5.3 billion.

The primary driver is capital expenditures.

CapEx surged 70% to $22.4 billion in Q2 alone. Management has guided to approximately $85 billion for the full year 2025.

The numbers paint a clear picture: Alphabet is trading today’s cash generation to ensure they can meet the surging demand for AI infrastructure and services.

Is this concerning? Perhaps. But there is a case for Google to lock in market share and remain at the forefront rather than miss the opportunity.

It’s worth noting that even with higher depreciation from these investments, margins remain robust. We’re seeing Google Cloud hit all-time high operating margins through operating leverage, and overall company margins would have expanded 150 basis points without the legal settlement.

The company is investing at this scale because demand is strong. As Philipp Schindler noted: “With this strong and growing demand for our Cloud products and services, we are increasing our investment in capital expenditures in 2025.”

The key question: Will these investments generate adequate returns?

Only time will tell, but historical precedent is encouraging. Google’s previous infrastructure investments—from building their own data centers to designing custom chips—have generated healthy returns over time. The company has a track record of turning CapEx into competitive advantages.

Management’s Forward Vision

Sundar Pichai stated during the call: “We are leading at the frontier of AI and shipping at an incredible pace.”

The evidence supports this view so far:

Search is evolving, not dying. AI Overviews and AI Mode are expanding use cases while maintaining monetization rates. The Cloudflare situation gives Google preferential access to fresh web data.

Cloud has reached an inflection point. The 940 basis point margin expansion in one year shows the business model is working. The $50 billion run-rate is remarkable.

AI is driving demand everywhere. From Cloud infrastructure to Search queries to YouTube recommendations, AI is enhancing every part of the business.

Management sees AI as a transformative platform shift requiring substantial investment.

Philipp Schindler emphasized the breadth of demand: “AI is positively impacting every part of the business, driving strong momentum.”

This isn’t just about defending against ChatGPT or competing with AWS. It’s about building the infrastructure for an AI-native future where every query, every video recommendation, every cloud workload is enhanced by artificial intelligence.

If I were Google, I would invest aggressively to capture demand while competition is still figuring out their business models and can’t live indefinitely on VC money. Build a moat through infrastructure that competitors can’t easily replicate.

Will it work? The Q2 results suggest they’re on the right track. Search revenue continues growing. Cloud margins are expanding rapidly. YouTube is monetizing new formats successfully.

But it’s still a massive bet. If AI adoption slows, if competitors find ways around Google’s advantages, if regulators intervene—any of these could derail the strategy.

For now, management is betting that AI represents a fundamental platform shift comparable to mobile or the internet itself.

Conclusion: The Fog Is Lifting With Each Quarter

The jury is still out on Alphabet’s AI transition, but each quarter provides more clarity. What seemed murky when ChatGPT grabbed the world by storm is becoming clearer with each earnings report.

The company is successfully navigating multiple challenges simultaneously:

Monetizing AI without cannibalizing search. AI Overviews are monetizing at comparable or better rates while expanding use cases. Search revenue grew 12%, demonstrating resilience in the face of new competition.

Expanding Cloud margins dramatically. A 940 basis point margin expansion in one year shows significant operating leverage taking hold. The path to AWS-level profitability (39% operating margins) is becoming visible.

Maintaining competitive advantages through infrastructure. The $85 billion CapEx commitment ensures Google can meet demand while competitors scramble for compute. The OpenAI partnership on Google Cloud proves even rivals need their infrastructure.

Benefiting from structural advantages. The Cloudflare situation grants Google preferential access to fresh web data—an advantage competitors can’t easily replicate in the near term.

Q2 results show a company that’s adapting its core products, monetizing new features, and investing to maintain its position in AI development.

The landscape continues to evolve. Regulatory intervention could change competitive dynamics. Well-funded competitors are working to find sustainable business models. The massive CapEx investments need to generate adequate returns.

But based on the evidence so far—14% revenue growth, expanding margins (excluding one-time charges), successful AI monetization—Alphabet appears to be executing well on a coherent strategy.

The search giant refused to die. Instead, it’s evolving into something potentially more powerful—an AI-native company with the infrastructure, data, and business model to monetize the transformation.

Time will tell if the $85 billion bet pays off. But the Q2 results suggest Google is successfully navigating the AI transition while maintaining the profitability of its core business.

The fog is lifting. The view, at least for now, is encouraging.

[For Steady Compounding Insider Stocks Members]

The analysis continues with my portfolio positioning based on these Q2 results. Members can access:

- Portfolio Update: One Sell, Two Potential Buys – My specific trades based on this quarter’s learnings, including which positions I’m exiting and where I’m redeploying capital

- Detailed rationale behind each portfolio decision

- Links to my in-depth research on the companies involved

This portfolio update section, along with all my past research reports is available exclusively to Steady Compounding Insider Stocks members.

If you’re interested in following my investment journey and accessing the complete analysis, you can learn more about membership here.

Disclaimer: This research reports constitute the author’s personal views only and are for educational purposes only. It is not to be construed as financial advice in any shape or form. From time to time, the author may hold positions in the below-mentioned stocks consistent with the views and opinions expressed in this article. Disclosure – I hold a position in Alphabet at the time of publishing this article (this is a disclosure and NOT A RECOMMENDATION).