Articles

About

Newsletter

Resources

Log In

No Result

View All Result

Updates

Research Reports

Become a member

Articles

About

Newsletter

Resources

Log In

Research Reports

Become a member

JOIN

Tag:

Wells Fargo

Options

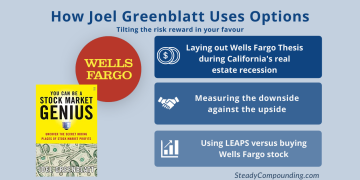

How Joel Greenblatt Uses Options

by

Thomas Chua

February 8, 2021

0

No Result

View All Result

Articles

About

Newsletter

Resources

Log In

© 2026

Steady Compounding

- By Thomas Chua