Articles

About

Newsletter

Resources

Log In

No Result

View All Result

Updates

Research Reports

Become a member

Articles

About

Newsletter

Resources

Log In

Research Reports

Become a member

JOIN

Tag:

Options

Options

Adjusting Your Options Position

by

Thomas Chua

March 5, 2021

0

Options

Using Options for Special Situations

by

Thomas Chua

February 28, 2021

2

Options

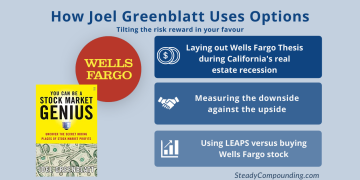

How Joel Greenblatt Uses Options

by

Thomas Chua

February 8, 2021

0

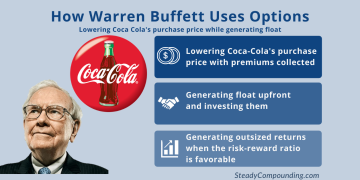

Options

How Warren Buffett Uses Options

by

Thomas Chua

February 1, 2021

2

Options

Why Gamestop went to the moon with Gamma Squeeze

by

Thomas Chua

January 28, 2021

0

Options

Why Did Nancy Pelosi Buy Tesla Calls

by

Thomas Chua

January 26, 2021

0

Options

Rules for dealing with options

by

Thomas Chua

January 25, 2021

0

Options

Determinants of options price (2)

by

Thomas Chua

January 22, 2021

0

Options

Determinants of Option Price (1)

by

Thomas Chua

January 19, 2021

0

No Result

View All Result

Articles

About

Newsletter

Resources

Log In

© 2026

Steady Compounding

- By Thomas Chua