Inflation in Singapore surged to 7.5% year over year in August 2022, and the tax season is approaching.

Before the pandemic, I remember paying $4.80 for a regular Ya Kun toast set, but now 2 eggs, 2 slices of bread and a Kopi O at Yakun will cost you $5.60.

What caused inflation to spiral out of control?

There are three main causes: (1) The Fed, (2) China’s zero-covid policy, and (3) Ukraine-Russia war.

The Fed was slow in acknowledging inflation

One key reason is that the US Federal Reserve took too long to recognize that inflation is not transitory. Jerome Powell, chair of the Fed, said in April 2021, “Readings on inflation have increased and are likely to rise somewhat further before moderating. However, these one-time increases in prices are likely to have only transitory effects on inflation.”

The Fed refused to believe that inflation was not temporary, and did not reverse their earlier policy of flooding the economy with cheap money to help people and businesses battle the adverse impact COVID-19 had on the economy.

The inflation rate jumped from 1.4% in the 12-month period from January 2020 to January 2021 to 9.1% in the 12-month period from June 2021 to June 2022.

Taking a page from 2008, the Fed has reduced interest rates and injected money into the economy to encourage consumer and business spending in response to COVID-19. This was to lower borrowing costs and support economic growth. However, when done in excess, it contributed to a sharp rise in global inflation.

China’s zero-Covid policy

The global economy suffers whenever China, the world’s largest manufacturing hub, is put on lockdown.

Shanghai’s lockdown, for example, shocked the global supply chain. Shanghai port accounts for a fifth of China’s port volume, and China contributes 15% of the world’s merchandise exports. Any time it goes into lockdown, it will further exacerbate inflationary pressures globally.

Russia-Ukraine War

Russia and Ukraine are major commodities producers. Ukraine is the world’s largest producer of sunflower oil. When we take Russia into account, both countries are responsible for more than 50% of global exports of vegetable oils. The region also exports 36% of the world’s wheat.

This caused food prices around the world to skyrocket as countries scrambled to look for alternative sources. The disruption in food supply can’t be remedied overnight, and it will take some time before the world adjusts to this new reality.

Since Russia is one of the world’s largest producers of crude oil and natural gas, energy prices have also spiked. Due to the reopening of the economy and the cold winter, disruptions in supply levels combined with Europe’s commitment to reduce natural gas production led to a spike in energy prices.

We’re gonna have inflation for a while

The Monetary Authority of Singapore (MAS) gave its outlook on inflation in October 2022, “Inflation is projected to ease more discernibly in the later half of 2023, although there is considerable uncertainty around the outlook for inflation and growth.”

In other words, we can expect to see inflation rage on up till the second half of 2023 at least. Our hard earned savings and purchasing power will continue to erode under the claws of inflation.

So what can we do to preserve our hard-earned income’s purchasing power?

Think about how you can beat inflation while saving on taxes.

Topping up your CPF Special Account

The most common and straightforward method is to top up your CPF Special Account (SA) to qualify for up to $8,000 in tax relief.

But there are three limitations with the CPF Cash Top-up Relief:

Firstly, you can only enjoy up to $8,000 in tax relief. If you are a high-income earner, you may want to consider other alternatives.

Secondly, top-ups to CPF SA are restrictive. It can’t be used for CPF schemes for investment, insurance, etc.

Thirdly, the SA limit is $192,000 and the MediSave Account limit is $66,000 (these limits are only for 2022).

Given the limits and restrictive nature of CPF top-ups, not everyone will top-up their CPF to save on taxes.

The alternative method would be to contribute to your Supplementary Retirement Scheme (SRS) account.

Supplementary Retirement Scheme

The SRS is a voluntary saving scheme to encourage Singaporeans to save more for retirement.

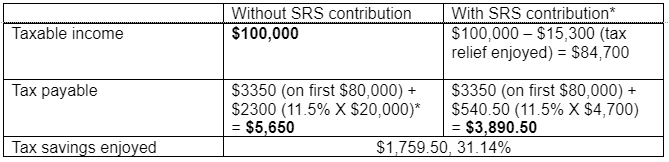

Similar to CPF Cash Top-up relief, contributing to your SRS account offers attractive tax benefits. For Singaporeans, you may contribute and enjoy up to $15,300 yearly in tax reliefs. The sum for foreigners goes up to $35,700.

Assuming you have a taxable income of $100,000 before tax-relief from SRS:

*CPF top-ups / SRS contributions by the end of 2022 will be considered for Year of Assessment 2022, and taxes will be payable in 2023.

This means that if you are a high-income earner, contributing $15,300 would provide you up to 31.14% in tax savings!

Withdrawing your SRS

Unlike the CPF which is more restrictive in terms of withdrawals, there is more flexibility for SRS savings. Upon reaching your statutory retirement age, you are allowed to make a lump sum withdrawal or spread it over 10 years. There will be no penalties, and only 50% of the amount withdrawn is taxable.

If you need to withdraw your SRS before the retirement age, you can do so, but will need to pay a 5% penalty and the full withdrawal amount is taxable. The penalty for early withdrawal will not apply if it is on medical grounds, or other circumstances such as bankruptcy, etc.

Here is the catch — it’s possible to avoid paying taxes altogether!

Or at least reduce the amount of tax payable.

Nope, it’s not illegal. It’s just a matter of spreading out your withdrawals.

Assuming you only withdraw your SRS post-retirement, in other words, you no longer draw an income. You may withdraw $40,000 from your SRS annually, for 10 years, tax-free!

There’re 2 factors here:

(1) The first $20,000 of chargeable income is taxed at 0%.

(2) Only 50% of your SRS funds are subject to tax.

Hence, if you can withdraw up to $40,000 annually, with only 50% of it subject to tax at 0%, it is essentially tax-free.

You may read more about the different withdrawal scenarios here.

Growing your SRS funds

Here is the thing—unlike your CPF SA and MA which earns 4% per year, the interest rate on monies in your SRS account is fixed at 0.05% per year.

Considering the opportunity costs, it would be a terrible idea to not invest your SRS funds and let inflation erode your SRS savings, especially if you have a long runway.

The good news is that SRS allows us to invest in a wide range of products, including bonds, Singapore Government Securities (SGS)/Singapore Savings Bonds (SSB), fixed deposits, foreign currency fixed deposits, shares, single premium insurance and unit trusts.

An affordable and convenient way is to invest your SRS funds with MoneyOwl to grow your retirement fund while beating the rate of inflation.

Before we begin, it is important to note that investing is not for everyone. It is important to take factors, such as your investment horizon, liquidity needs and risk tolerance, into consideration.

If volatility keeps you up at night and you will need retirement savings in the near term, topping up your CPF would be the better alternative. To reiterate, CPF SA offers a decent 4% p.a. risk-free returns with up to $8,000 in tax savings.

Investing your SRS with MoneyOwl

As an NTUC social enterprise, MoneyOwl’s mission is to enable people to make wise financial decisions to live their best possible life. One of the ways they do this is through their fundamentally sound portfolios.

For a limited time, MoneyOwl is giving away FairPrice E-vouchers worth up to $500 for clients who invest their SRS funds on its platform before 31 Dec 2022!

MoneyOwl offers 3 main portfolios for SRS funds, depending on your investment goals:

- Dimensional: Funds will be invested in a globally diversified portfolio to grow your wealth.

- WiseIncome: Grow and invest for your retirement

- WiseSaver: Park spare cash

Dimensional

MoneyOwl Dimensional provides five portfolios, depending on your risk tolerance and investment period:

- Conservative: 20% equities, 80% bond

- Moderate: 40% equities, 60% bond

- Balanced: 60% equities, 40% bond

- Growth: 80% equities, 20% bond

- Equity: 100% equities, 0% bond

You can do a quiz here to find out which portfolio suits you.

WiseIncome

MoneyOwl WiseIncome provides three payout options to cater to your needs at various life stages. You can use your SRS monies to invest in the WiseIncome Grow & Invest Payout option:

- Reinvest your payouts and watch your money grow.

- For those who want to build up assets to reap a higher payout later.

You may read here to find out more.

WiseSaver

MoneyOwl WiseSaver is a fund that invests in Singapore Dollar bank deposits. This is a low-risk investment, and the current rate is 3.26% p.a. (as of 21 October 2022).

Getting Started with MoneyOwl

To start investing your SRS funds with MoneyOwl, it is as easy as completing the following steps:

- Open a SRS account with DBS, OCBC or UOB online and deposit funds in it

- Create a MoneyOwl account and head to their investment platform

- Start investing in any portfolios with your SRS funds

- Enjoy tax relief while earning up to $500 worth of FairPrice E-vouchers

My 2-cents

When it comes to investing, I prefer to invest overseas in high-quality companies such as Amazon, Apple, etc. As Buffett says, “the first rule of fishing is fish where the fish are.” With funds such as MoneyOwl Dimensional, I’m able to circumvent the limitation of investing in Singapore stocks with my CPF OA and SRS monies, and gain access to a low cost globally diversified portfolio and not let inflation erode my SRS savings.

Besides, my personal rule-of-thumb would be to invest for capital growth instead of income if you are younger, with 10 years or more till retirement.

Readers of my article on income investing would know that I echo Terry Smith’s thinking that we should focus on total returns—returns from share price increases and dividends—and not just dividend returns alone.

And generally, investing in a globally diversified portfolio (i.e. dimensional portfolio) would bring higher total returns compared to a portfolio of predominantly income-generating assets.

That said, I have a long duration (more than 30 years) and a stomach for volatility. If you need help deciding which portfolio, you can try the “Build Your Portfolio” feature for Dimensional or WiseIncome. Alternatively, you may arrange for a phone call here.

Conclusion

There are predominantly two ways to reduce taxes, beat inflation, and invest for your retirement: (1) Topping up CPF SA and (2) Topping up your SRS account & investing them. With services such as MoneyOwl, we are able to invest our SRS funds into a diversified portfolio with low fees.