A simple trick to becoming an automatic millionaire

Take advantage of ‘out of sight, out of mind’!

Peter Lynch on the right time to buy bonds instead of stocks

When is a good time to buy bonds?

My 2 Cents on Retirement: Why Your Current Plan Might Fail You

I’ve been invited to speak at the Ready for Life event in Marina Bay Sands, Singapore, on 7 October, hosted by the Central Provident Fund Board (CPF). The topic? Retirement. The way I view retirement has changed over the years….

Fight record high inflation by saving on tax dollars and put them to work

Inflation in Singapore surged to 7.5% year over year in August 2022, and the tax season is approaching. Before the pandemic, I remember paying $4.80 for a regular Ya Kun toast set, but now 2 eggs, 2 slices of bread…

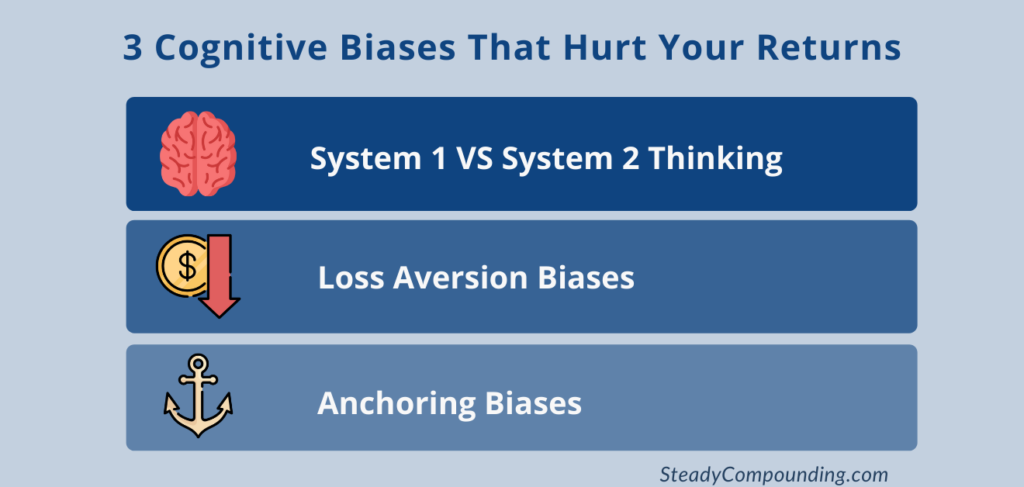

How Can You Overcome the 3 Cognitive Biases that Hurt Your Returns

“If you don’t know who you are, this [the stock market] is an expensive place to find out.”

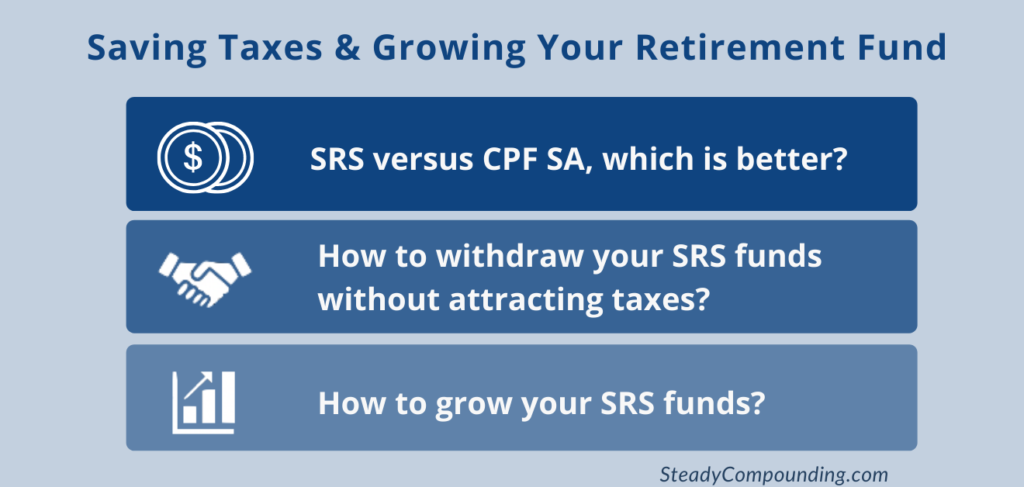

A Better Way to Save Taxes and Plan for Retirement in Singapore 2021

As the Singapore tax season approaches, we might wonder if there are ways to save on taxes while preparing for retirement.

What Is Your Rich Life?

I spent a huge part of my teens studying how to turn my financial situation around and it could be summarized into: get a decent paying job, underspend your income, and own equities.But I never actually thought about this—what is…

Lessons from The Psychology of Money

The Psychology of Money is one of the most highly anticipated books for finance enthusiasts in 2020. Morgan Housel has a knack for writing beautifully and a flair for capturing abstract concepts onto paper. This is not at all common…

How to Avoid Getting Hurt: Don’t Chase Yields Blindly

Some of the most popular asset classes Singaporeans love are REITS, bonds, and stocks that pay a high dividend yield. And understandably so, because we are so sold on the idea of generating consistent, sustainable passive income to cover our…

Setting up Your Financial Framework for Success in Your 20s

If you wish to become financially independent, being in your twenties is arguably the most important decade in your life as you have a long runway ahead of you. It is also at this stage where we are prone to…